The yen was the main gainer among the G10s, while major equity indices ended Monday's session in the red. Once again, the catalysts may have been rising US Treasury yields as well as worries over Italy’s budget plans. The fact that PBOC’s easing over the weekend failed to support Chinese stocks may have also contributed to risk aversion.

Sentiment Remains Fragile Amid a Blend of Italy, China, and Fed Hike Speculation

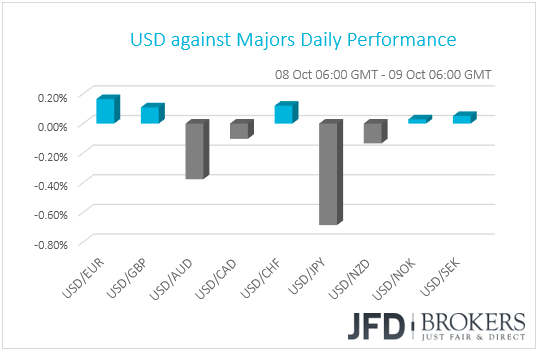

The dollar traded lower or unchanged against most of the other G10 currencies on Monday. It gained slightly only against EUR, GBP and CHF. The greenback underperformed versus JPY, AUD, NZD and CAD, while it traded virtually unchanged against NOK and SEK.

Market sentiment remained fragile yesterday, even if this is not clearly visible by the performance of currencies. Yes, the safe-haven yen was the main winner against its US counterpart, but the risk currencies AUD and NZD, instead of sliding as it is usually the case, they gained. In any case, investors’ mood was better reflected in the equity markets. Major EU and US indices ended in the red, with the exception being Dow Jones, which closed slightly in the green.

Once again, the driving force may have been a blend of rising US Treasury yields and concerns surrounding the Italian political landscape. The fact that China’s policy easing over the weekend failed to boost the Chinese equity market may have also contributed to risk aversion, with investors perhaps reluctant to believe that these measures can bolster the Chinese economy.

Starting with US Treasuries, they continued to surge on concerns of faster-than-previously-anticipated rate increases by the Fed, with 10-year yields hitting 3.252, their highest since April 2011. Higher interest rates mean higher borrowing costs for companies, something that could erode their profitability, and that’s why some investors may have abandoned the equity market.

Now moving to Italy, the nation’s 10-year government bond yields surged 6.25%, while the FTSE MIB index slid 2.43% on renewed concerns over Italy’s budget pans. Yesterday, Deputy PM Matteo Salvini called EU Commission President Juncker and Commissioner Pierre Moscovici as enemies of Europe. His comments come after Juncker called on Italy to increase its fiscal efforts in order to avoid breaching EU rules.

Italy is set to submit a draft proposal to the European Commission next week and thus, we expect markets to stay sensitive on headlines and comments ahead of the submission. Anything adding to concerns that EU officials could reject the plan may keep pressure on Italian assets, the euro, as well as the broader risk sentiment.

Last but not least, we have China. Over the weekend, the People’s Bank of China (PBOC) decided to ease monetary policy, cutting the amount cash lenders must hold as reserves by 1 percentage point, a move aimed at supporting the economy amid escalating trade tensions with the US. However, instead of trading north, Shanghai’s Composite Index slid on Monday, closing 3.72% down. Perhaps investors were not convinced that this measure could have the desired effect. It could also be that, with China on holiday last week, the tumble in Chinese equities was just an accumulation of the negative sentiment we saw being reflected in other global markets.

That said, on Tuesday, Shanghai’s index closed 0.17% up, perhaps due to PBOC’s second consecutive upside fixing in the USD/CNY central rate overnight. The central bank fixed the onshore yuan at 6.9019 per dollar, prompting investors to drive the offshore rate (USD/CNH) up to 6.9348, slightly below yesterday’s peak of 6.9371.

The recent slide in the yuan triggered comments by a senior US Treasury official, who said that the US remains concerned over the yuan’s devaluation. The official also said that these concerns would be laid out in their semi-annual currency report, which is scheduled to be released next week. US President Trump has accused China for manipulating its currency several times in the past, and thus, it would be interesting to see whether the Treasury Department will name the nation as currency manipulator, something that could give President Trump more reasons to proceed with tariffs on the remaining USD 267bn worth of Chinese goods imported to the US.

USD/JPY – Technical Outlook

USD/JPY broke and closed below its short-term upwards moving support line, drawn from the low of the 7th of September. Also, the pair has broken the neckline of the head-and-shoulders pattern, which is visible on the 4-hour chart. All this suggests that USD/JPY could continue its sail south, as some more potential sellers who have missed the yesterday’s slide, may want to get a piece of that cake. For now, we remain bearish, at least for the short-run.

With the rate now returning towards the neckline of the head and shoulders, at around 113.50, the bears may be tempted to take advantage of the higher rate and perhaps push it down for another test near yesterday’s low of 112.80. A break below that zone could interest more bears to join in the action and push USD/JPY further down towards the 112.40 support zone, near the lows of the 21st and 24th of September. That level was also a good resistance on the 19th of the month.

The RSI and the MACD both rebounded within their bearish territories, supporting the case for some further recovery, at least towards the neckline of the head and shoulders.

Because the sentiment is still more to the downside, we will take a more conservative approach in terms of the upside for USD/JPY. To consider the pair moving higher in the longer-term, we would need to see it breaking back above the short-term upside support line and closing above the 114.07 zone, marked by the highs of the 1st and 5th of October. Only then we could get comfortable and start examining higher resistance areas like the 114.55 barrier, which held the rate down on the 3rd of October. Just 20 pips higher, lies another potential strong resistance at 114.75, marked by the peak of November last year.

![]()

USD/CNH – Technical Outlook

Since the summer of this year, the Chinese yuan had depreciated heavily against its US counterpart. Obviously, not without the help of the Chinese authorities. From the technical side, we can see that since the end of August, USD/CNH has slowed down its uprise. From the short-term perspective, the pair is balancing above its short-term upside support line, taken from the low of the 26th of July, but it looks like it could be aiming for a bit of retracement to the downside, before going back higher again in the near-term.

In order to consider a small corrective move to the downside, we would need to see USD/CNH dropping below the 6.9125 support zone, slightly above the overnight low. This could open the path for the 6.8890 key area, marked by the lows of the 5th and the 4th of October, as well as the highs of the 28th and the 12th of September. This is where the bulls could jump back into the action and aim for another test near yesterday’s peak of around 6.9370.

That said, even if the 6.8890 area does not prove attractive for the bulls and breaks, we would still consider the near-term outlook to be cautiously positive, as the rate could rebound again from near the crossroads of the aforementioned upside support line and the 6.8560 level. Let’s also not exclude a possibility to see the pair reversing to the upside straight away, where it could break the yesterday’s high at 6.9370 and make its way towards the peak of August near the 6.9590 barrier.

The alternative scenario could be a close below the upside support line and the 6.8560 level. This way we could start looking south, but in order to get comfortable with further declines, we would need USD/CNH closing below the 6.8230 hurdle, which proved a solid support throughout the whole month of September. Only then, a test of the 6.7850 support zone could become a reality. That zone held the rate from dropping lower on the 28th of August. Slightly below lies another good potential support, in case the 6.7850 level doesn’t hold, and that’s the 6.7736 obstacle, which withheld USD/CNH from moving lower on the 26th of July.

![]()

As for Today’s Events

The calendar appears relatively light in terms of economic data. The only releases worth mentioning are the US NFIB Small Business Optimism Index for September and Canada’s housing starts for the same month. The NFIB index is anticipated to have ticked up to 108.9 from 108.8, while Canada’s housing starts are expected to have increased to 210.0k from 201.0k.

We also have 4 speakers on the agenda: Chicago Fed President Charles Evans, BoE MPC member Ben Broadbent, and BoC Deputy Governor Carolyn Wilkins will speak during the US session. During the Asian morning, New York Fed President John Williams will step up to the rostrum.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.