A few big central banks will take the spotlight this week, delivering their interest rate announcements. Also, the focus remains on Brexit negotiations and Italy’s budget plan, both of which would add their touch on the markets.

Monday will be a quiet day in regards to economic data releases. No major market moving data are expected to come out. The only thing that everyone should be on a look out is any news coming out of Italy, as it is expected to reply to Brussels notes made last week. Just a reminder of the issue, the European Commission came out on Thursday saying that the submitted draft of the Italian budget plan is a clear violation of the EU rules. Mario Draghi was also one of those who showed dissatisfaction. Even though he spoke without finger pointing at certain countries, still his message was clear that he also has concerns over the Italian proposed budget plan draft.

Tuesday won’t be a more exciting day than Monday in terms of economic data. The Bank of Japan is set to release the its YoY core CPI figure, which currently has no expectations on what it could be, but we know that the previous one was released at +0.5%. The BoJ states that the banks main aim would be price stability, which is important for their economic activity, as businesses make their decisions mainly based on the prices of goods and services. Quote: “On this basis, the Bank set the "price stability target" at 2 percent in terms of the year-on-year rate of change in the consumer price index (CPI) in January 2013 and has made a commitment to achieving this target at the earliest possible time”, as stated by the BoJ.

Starting from Wednesday, the economic data releases will carry more weight. Wednesday will be the PMI day, as the EU, together with Japan and the US will be releasing their preliminary manufacturing purchasing manager’s index numbers. But before Europe and the US kick off with that, Japan will show how their manufacturing sector has performed. The previous number came out 52.5, which is still ok, more or less stable and almost in line with the previous 2-year figures. Now the forecast sits at 52.6. The German preliminary PMI is expected to come out at 53.4, slightly below the previous number of 53.7. Eurozone’s as a whole, preliminary manufacturing PMI is forecasted to come down from the previous 53.2 to 53.1. The bloc's preliminary services index is also set to be released, expected to have declined slightly from 54.7 to 54.5.

We get the preliminary PMI data from the US as well. The manufacturing number is expected to have declined a tick, from 55.6 to 55.5, whereas the services figure is forecasted to have risen from 53.5 previous to 54.1.

But there is one central bank that will attract attention in between the European PMI releases and that’s the Riksbank. The Swedish central bank is set to announce that their Repo rate is expected to have remained at the previous negative 0.5%. According to the Riksbank’s monetary policy report, quote: “Economic activity in Sweden is strong and inflation is close to the target of 2 per cent. Rapidly rising energy prices have helped to push up inflation. If energy prices are disregarded, inflationary pressures are still moderate. As it is important for economic activity to continue to be strong and have an impact on price growth, monetary policy needs to remain expansionary.” The Swedish CPIF on a YoY basis jumped to +2.5% in September, from the previous +2.2%. For now, the Repo rate will remain unchanged, but because inflation started picking up, the Swedish bank said that it could be raising its rate by 25 bps either in December or February.

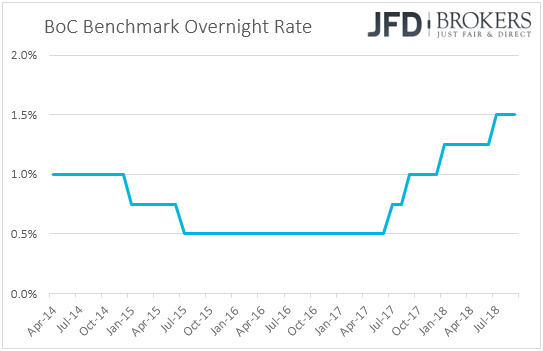

The Bank of Canada will have its say on their interest rate as well. Everyone will be expecting the Bank to raise its interest rate by 25bps, which is expected go from +1.50% to +1.75%. Even though the recent economic data releases from Canada showed that the retail sales and inflation came out weaker than expected, still, the bank is planning to go ahead with the rise. Just to remind that last Friday, the headline CPI on YoY basis came out at +2.2%, which half of a percent lower from the expected +2.7% for the month of September. Retail sales (MoM) were disappointing as well, as they slid 0.1% for the month of August, where it was anticipated that they could come out at +0.3%.

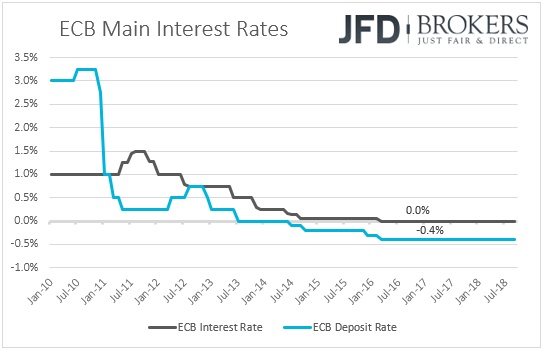

On Thursday, ECB will take the centre stage, as it will announce their interest rate decision. No surprise here as the European Central Bank is expected to keep the rate at the same level as previous 0.00%. The ECB is planning to keep borrowing costs unchanged at least through the summer of next year. According to the ECB minutes from the September meeting, the risks of the Euro Area are somewhat balanced, and the economy seems to be showing good health. But the recent negative developments around rising protectionism and the vulnerability of the emerging markets worries the central bank. Also, the ECB is concerned about the Italian issue, Brexit, and the US trade wars, all of which could have their effect on the future policy decisions of the European Central Bank. 45 minutes after we get the ECB rate announcement, Mario Draghi will hold a press conference, where he will answer economics and political questions surrounding the Eurozone.

Other important economic data releases that we will get on Thursday, will be the Norwegian unemployment rate, which is set to come out during the early European morning. The figure is expected to come out the same as previous at 4.0%. Two hours after that, the Norges bank will announce their interest rate decision. There should be no surprises there, as the bank is expected to keep the rate unchanged at +0.75%. The Bank is planning to keep the rate running at the current level at least until Q1 of 2019. The Bank also states that it cannot continue keeping the rate low for too long, as it could force wage and price inflation to rise, creating financial imbalances.

Also, we will get the Swedish PPIs, the German business climate index and the US pending home sales. The last one is expected to have improved, going from the previous -1.8% to -0.1%.

On Friday all eyes will be on the US QoQ GDP number for Q3. The markets will be expecting growth to come out at +3.3%, compared to the previous +4.2%. The previous number was the highest since Q3 of 2014. Even though analysts are expecting a slowdown of the economy, still, it remains on the right path. Certainly, the Fed will be watching the data very carefully as well. According to the FOMC minutes delivered last week, it seems that the Fed is sticking to its plan of raising rates in the future, unless there will be significant indications of a slowing economy.

From the European data news, we will be getting the Swedish retail sales figures for the MoM and YoY basis. The first is believed to have dropped from the previous +0.8% to +0.5% for the month of September. The YoY number is forecasted to have declines sharply from the previous +2.0% to +0.5%. That’s a potential one and a half percent drop, which could not go unnoticed by the Riksbank.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2018 JFD Brokers Ltd.