The calendar includes only one central bank decision this week, and that’s the Fed’s decision on Wednesday. Although no action is expected this time around, investors may look for hints as to how ready officials are to act again if the virus situation continues to worsen. They are also likely to keep an eye on the Congress’s decision over a new coronavirus-aid bill. As for the data, we have the US and Euro-area preliminary GDPs for Q2, as well as the Australian CPIs for Q2, and the preliminary Eurozone inflation numbers for July.

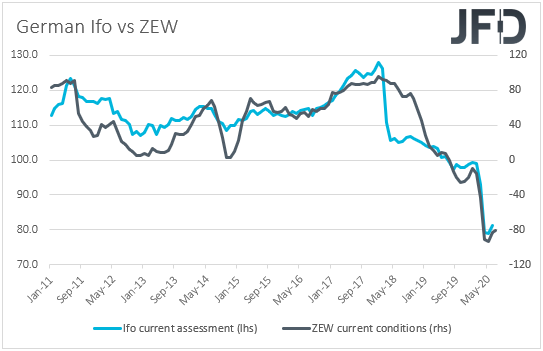

On Monday, the agenda includes the German Ifo survey for July and the US durable goods orders for June. With regards to the Ifo survey, both the current assessment and expectations indices are expected to have risen to 85.0 and 93.7 from 81.3 and 91.4 respectively, something that could drive the business climate one up to 89.3 from 86.2. However, both the ZEW indices for the month improved less than anticipated, and thus, we would consider the risks surrounding the Ifo forecasts as tilted slightly to the downside.

With regards to the durable goods, expectations are for headline orders to have slowed to +7.2% mom from +15.7%, while the core rate is anticipated to have slid to +3.5% mom from +3.7%.

On Tuesday, the only release worth mentioning is the US Conference Board consumer confidence index for July, which is expected to have declined to 94.5 from 98.1.

On Wednesday, the FOMC ends its two-day monetary policy gathering. When they last met, Fed officials kept interest rates unchanged and noted that they will continue to increase purchases of bonds and mortgage-backed securities “at least at the current pace”, something suggesting that purchases can accelerate if deemed necessary. With regards to the new dot plot, the median dots suggested that interest rates are likely to stay at the current level at least until 2022. “We're not thinking about raising rates, we're not even thinking about thinking about raising rates”, Fed Chair Powell characteristically said at the press conference following the decision.

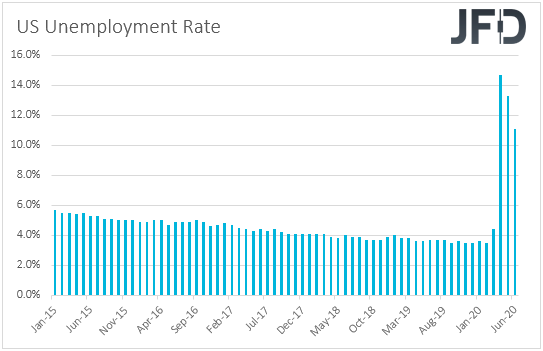

Since then, data were somewhat encouraging, with the unemployment rate declining for the second straight month in June, the NFP’s revealing record gains, and the ISM PMIs returning into expansionary territory. However, with the virus still spreading fast in the US, several states have halted or reversed their reopening, which could dampen the economic recovery and raise speculation over more stimulus. Thus, although policymakers are not expected to act this time around, investors may look for hints as to how ready officials are to act again if the situation continues to worsen. In other words, it would be interesting to see whether they will maintain the “at least at the current pace” wording, and whether they will strengthen it.

Investors will also be eager to find out whether the US Congress will agree on a new fiscal-stimulus package before the extended unemployment aid for millions of Americans expires at the end of the week. Democrats want the enhanced benefits of USD 600 per week to be extended and support a much bigger stimulus than the USD 1trln proposed by Republicans. Thus, for equities and risk-linked assets to rebound, a bigger number than that may need to be agreed.

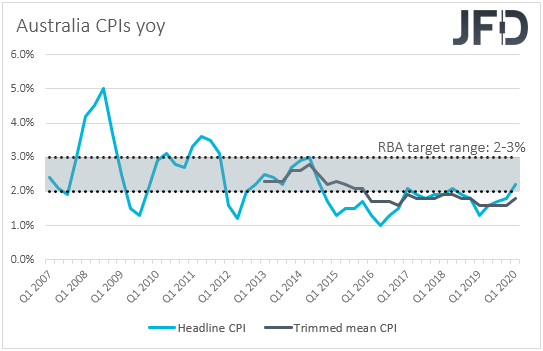

As for Wednesday’s data, during the Asian morning, we get Australia’s CPIs for Q2. The headline CPI rate is forecast to have fallen into negative waters, to -0.4% yoy from +2.2%, while the trimmed mean rate is anticipated to have declined to +1.4% yoy from 1.8%. At its latest meeting, the RBA kept the targets for its cash rate and the yield on 3-year government bonds unchanged at 0.25%, adding that they remain prepared to scale-up bond purchases again if deemed necessary. Officials noted that the worst of the global economic contraction may have now passed, but still, the outlook remains uncertain and the recovery is expected to be bumpy and dependent upon containment of the coronavirus. With all that in mind, and also considering the newly adopted lockdown measures in the state of Victoria, a deflationary CPI print may raise speculation that the RBA may indeed consider scaling up again its QE purchases at some point soon.

Later in the day, ahead of the FOMC decision, the US pending home sales for June are due to be released, and the consensus is for a slowdown to +15.3% mom from 44.3%, which is still a strong reading compared to the ones we were getting in the pre-coronavirus era.

On Thursday, during the Asian session, New Zealand’s ANZ business confidence index for July and Japan’s retail sales for June are coming out. No forecast is available for the ANZ index, while Japanese retail sales are forecast to have declined at a slower pace than in May. Specifically, they are expected to have fallen 6.5% yoy, after tumbling 12.5% in May.

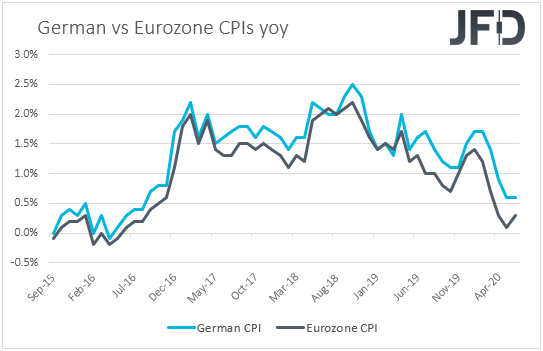

Later, from the EU, we have Germany’s 1st estimate of GDP for Q2 and the nation’s preliminary CPIs for July. The German GDP is forecast to have contracted 9.0% qoq, after shrinking 2.2% in Q1, while the CPI rate is anticipated to have fallen to +0.1% yoy from +0.9%. The German unemployment rate, as well as that for the bloc as a whole are also coming out. The German rate is expected to have ticked up to 6.5% from 6.4%, while the Euro-area one is forecast to have risen to 7.7% from 7.4%.

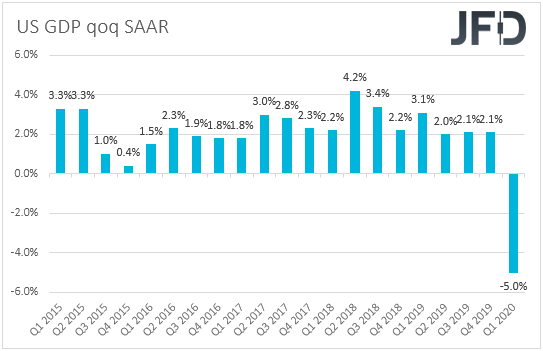

From the US, we get the 1st estimate of GDP for Q2. The forecast suggests that the coronavirus-related lockdown caused the economy to collapse by a historic 34% qoq after contracting 5% in the first three months of the year. The Atlanta Fed GDPNow model points to a -34.7% rate, very close to the consensus, but the New York Nowcast suggests that the economy contracted only 14.3%. If indeed, the actual print is closer to the New York estimate, risk-linked assets are likely to gain and safe havens could slide, as this will mean that the economic wounds from the coronavirus were not as severe as initially afraid. On the other hand, a worse than expected number would raise fears and concerns that the already adopted stimulative measures are not having the desired effect and that more may be needed.

Finally, on Friday, we have Japan’s employment and industrial production data for June. The unemployment rate is expected to have increased to 3.1% from 2.9%, while the jobs-to-applications ratio is anticipated to have declined to 1.16 from 1.20. Industrial production is anticipated to have rebounded 1.2% mom after falling 8.9%.

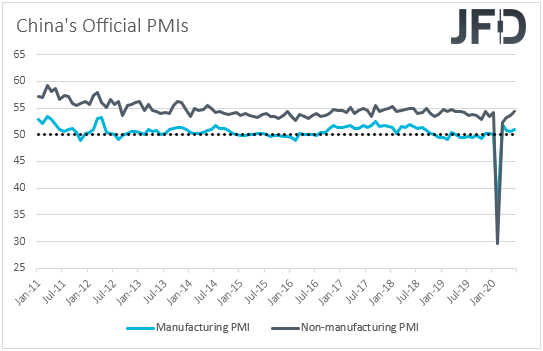

In China, the official PMIs for July are coming out. The manufacturing index is anticipated to have ticked up to 51.0, but no forecast is available for the non-manufacturing and composite prints. Following the second outbreak of the coronavirus in China, it would be interesting to see whether there were any economic damages due to that, and if so, how severe they were.

Eurozone’s 1st estimate of Q2 GDP and the bloc’s preliminary CPIs for July are also coming out. GDP is expected to have shrunk 11.2% qoq following a 3.6% contraction in Q1, while the headline CPI is expected to have ticked down to +0.2% yoy from +0.3%. No forecast is currently available for the core rate, which stood at +0.8% yoy in June.

At its last meeting, the ECB did not alter its monetary policy, but stayed ready to adjust all its instruments, as appropriate, to ensure that inflation moves towards its aim in a sustained manner. At the press conference following the decision, President Lagarde urged EU governments to take action in battling the coronavirus pandemic as soon as possible, with EU leaders eventually reaching consensus last Tuesday morning. The euro has been on a rally mode last week, on hopes that with a fiscal aid, the Eurozone is now likely to recover faster, and the return of the July PMIs into expansionary territory increased those hopes. Thus, it may need worse-than-expected GDP and CPI numbers to revive fears with regards to a halt in the economic recovery, and thereby more stimulus by the ECB. If the actual prints come close to their forecasts, despite weaker than the previous ones, we believe that the euro could continue to gain.

Later in the day, from the US, we have personal income and spending, alongside the core PCE index, all for June. Personal income is forecast to have declined 0.5% mom after falling 4.2% in May, while personal spending is expected to have slowed to +5.5% mom from +8.2%. With regards to the core PCE index, it is forecast to have held steady at +1.0% yoy. We also have the final UoM consumer sentiment index for July, which is expected to be revised down to 72.9 from 73.2.

Canada GDP for May is coming out as well, with the forecast pointing to a 3.5% mom rebound after a 11.6% contraction in April.

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 83% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2020 JFD Group Ltd.