We have a very busy week ahead of us with three central banks deciding on policy: the BoJ, the FOMC and the BoE. On the data front, the US employment report, due out on Friday, is likely to take center stage. The US core PCE index, the Fed’s favorite inflation metric, as well as Eurozone’s inflation and GDP data, are likely to attract attention as well.

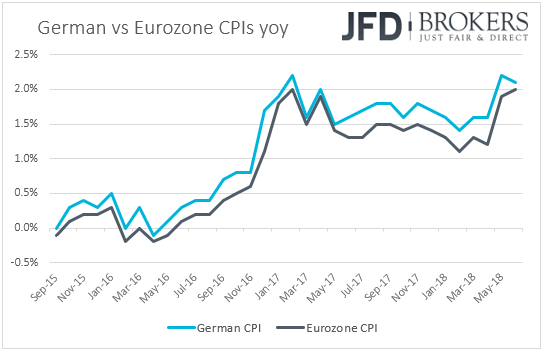

Monday appears to be a relatively quiet day in terms of economic events and releases. The only indicator worth noting is Germany’s preliminary CPI for July. The German inflation rate is expected to have remained unchanged at +2.1% yoy, something that would support the case for Eurozone’s headline print, due out on Tuesday, to have held steady as well.

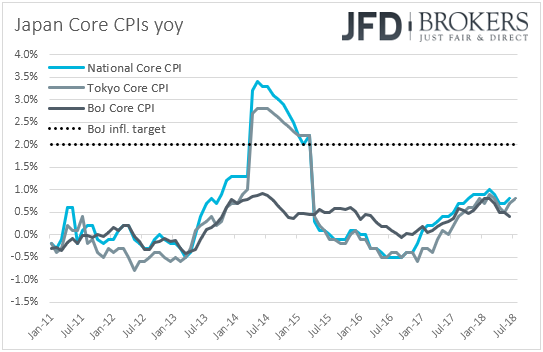

On Tuesday, Asian time, the BoJ concludes its two-day policy gathering. Following the recent reports that policymakers have been discussing possible changes to monetary policy, some investors may have raised bets that the Bank may start scaling back its stimulus program soon. However, with all Japanese inflation metrics, even the Bank’s own core CPI, well below its 2% objective, it’s hard for us to imagine the Bank taking a step towards normalization at this meeting. As for Japan’s economic indicators, we get the nation’s unemployment rate and the preliminary industrial production data, both for June.

From China, we have the official manufacturing and non-manufacturing PMIs for July. Expectations are for the manufacturing index to have ticked down to 51.4 from 51.5, while the non-manufacturing one is expected to have remained unchanged at 55.0.

During the European session, we get Eurozone’s preliminary inflation data for July and the bloc’s first estimate of the Q2 GDP. The forecast is for the headline CPI rate to have remained unchanged at +2.0% yoy, while the core rate is anticipated to have ticked up to +1.0% yoy from +0.9% yoy. As for first estimate of Q2 GDP, it is expected to show that the euro area economy grew 0.4% qoq, the same pace as in Q1. At the press conference following last week’s ECB meeting, President Draghi maintained the view that the risks surrounding the Eurozone’s economic outlook remain broadly balanced and noted that market expectations on interest rates are well aligned with the anticipation of the Governing Council. Thus, if the forecasts of the aforementioned data are met, we see it unlikely for investors to change their expectations around the Bank’s future plans.

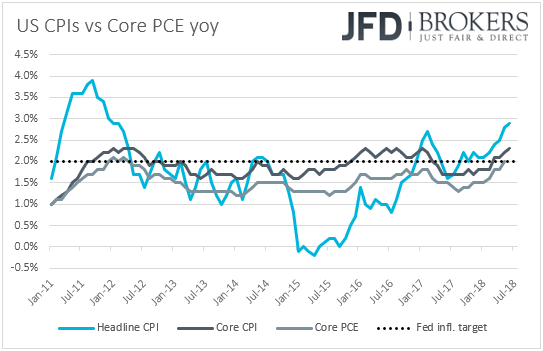

Later in the US, we have personal income and spending data for June, as well as the core PCE index for the month. Personal income is anticipated to have risen 0.4% mom, the same pace as in May. Spending is also expected to rise 0.4%, but this would be an acceleration from the previous monthly rate of +0.2%. That said, the slowdowns in the monthly earnings and retail sales prints for the month suggest that the risks surrounding both the income and spending forecasts are tilted to the downside.

As for the yoy core PCE rate, the Fed’s favorite inflation measure, it is expected to have remained unchanged at +2.0% yoy. However, bearing in mind that the core CPI accelerated during the month, we see the case for the core PCE index to have moved in a similar fashion. Just a day ahead of the FOMC decision, an acceleration of this inflation metric above the Fed’s 2% objective could increase bets that Fed officials will maintain an upbeat tone in the statement accompanying the decision, keeping the door open for two more rate increases until the end of the year.

From Canada, we get the monthly GDP print for May. The forecast is for the monthly rate to have risen to +0.3% mom from +0.1%, but this would drive the yoy rate down to +2.3% from +2.5%.

On Wednesday, the FOMC decides on monetary policy and expectations are for the Committee to keep interest rates unchanged. This is one of the “smaller” gatherings that is not accompanied by updated economic projections, neither a press conference by Fed Chair Powell. Thus, all the attention is likely to fall on the statement accompanying the decision.

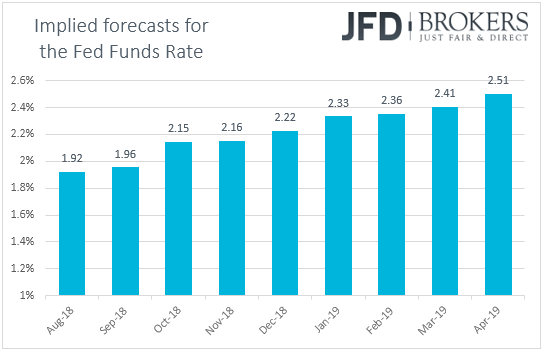

When they last met, Fed policymakers decided to raise interest rates by 25bps, while the new “dot plot” pointed at two more rate increases by year end, instead of just one as the previous plot suggested. The case for further gradual rate increases was also supported by the minutes of that meeting, as well as Powell’s semi-annual testimony before Congress.

Thus, despite the latest criticism of Trump over higher interest rates, we believe that officials will maintain their upbeat stance, sealing the deal for a hike at the September gathering and keeping the door open for another one in December. According to the Fed funds futures, the market assigns a 91% chance for a hike in September, while there is a 67% probability for another one to follow in December.

As for Wednesday’s economic data, during the Asian morning, we get New Zealand’s employment data for Q2. Expectations are for the unemployment rate to have remained unchanged at 4.4%, while the net change in employment is expected to have slowed to +0.4% qoq from +0.6% in Q1. In China, the Caixin manufacturing PMI for July is forecast to have ticked down to 50.9 from 51.0. The official manufacturing PMI is also expected to have declined fractionally, which supports the Caixin forecast.

During the European day, we get the final manufacturing PMIs for July from several European nations and the Eurozone as well. As usual, the final prints are expected to confirm the preliminary estimates.

We get manufacturing PMI data for July from the UK as well, just a day ahead of the BoE policy decision. The forecast suggests that the index slid somewhat, to 54.2 from 54.4, but such a small slide is unlikely to alter market expectations with regards to a BoE rate increase the following day.

In the US, we get the ADP employment report for July. Expectations are for the private sector to have gained 186k jobs, slightly more than June’s 177k. We expect this release to attract less attention than usual as investors may keep their gaze locked on the FOMC decision later in the day. The ISM manufacturing PMI for July is also due to be released and expectations are for a decline to 59.4 from 60.2 in June.

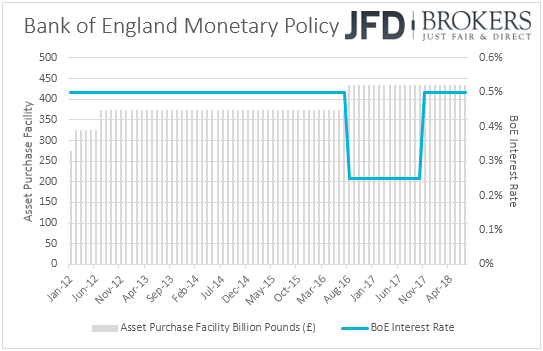

On Thursday, the central bank torch will be passed to the Bank of England. Actually, it will be a “Super Thursday” for the Bank, as besides the rate decision and the meeting minutes, it also releases its quarterly Inflation Report, which will be presented by Governor Mark Carney at a press conference after the decision.

Since the latest BoE gathering, when the Bank’s Chief Economist Andy Haldane joined the ultra-hawks Ian McCafferty and Michael Saunders in voting in favor of a rate increase, data have been mixed. All three of the June PMIs increased, while the NIESR GDP Model showed that the economy expanded +0.4% in the three months to June, in line with the Bank’s view. All these suggest that the economy may have indeed turned the corner following the slowdown in Q1. However, retail sales and, more importantly, the inflation data for June came on the soft side, with core inflation coming back below the Bank’s 2% target.

That said, the market remained overwhelmed with regards to a rate increase at this meeting. Thus, if the Bank indeed proceeds with hiking rates, investors are likely to turn attention to the votes to see whether the decision was a clear or close call, as well as to any signals with regards to the Bank’s future plans. They may be eager to find out whether the Bank is considering another increase by year end (or not).

As for Thursday’s indicators, the UK construction PMI for July is coming out, but we expect it to pass unnoticed as investors are likely to have their gaze locked on the BoE decision.

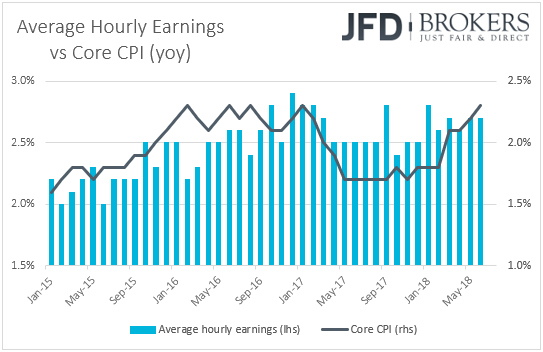

On Friday, the main event is likely to be the US employment report for July. Expectations are for non-farm payrolls to have increased 193k, after rising 213k in June. The unemployment is expected to have declined to 3.9% from 4.0%, while average hourly earnings are anticipated to have risen at the same yearly pace as previously (+2.7%).

Even though the initial market reaction may come from the NFP number, barring any major deviation from the forecast, the aftermath direction is likely to be dictated by wage growth. An upside surprise in wages could be translated to more spending and hence, accelerating inflation in the future. Conditional upon the Fed keeping the door wide open for two more hikes this year on Wednesday, this could strengthen further the case. On the other hand, a modest slide in the yoy earnings print could weigh somewhat on expectations on that front, but we doubt that it would be enough to drive them well down. In our view, we need to see a notable decline in the earnings rate in order for the probability of two more hikes in 2018 to drop below 50%.

As for the rest of Friday’s indicators, during the Asian morning, Australia’s retail sales for June and Q2 are due to be released. The June monthly rate is expected to have ticked down to +0.3% from +0.4%, but on a quarterly basis, retail sales are anticipated to have accelerated to +0.8% qoq from +0.2%. In China, the Caixin services PMI is coming out and expectations are for the index to tick up to 54.0 from 53.9.

As for the European day, we will get the final services and composite PMIs for July from the nations of which we get the manufacturing prints on Wednesday. Once again, the final prints are anticipated to confirm the preliminary estimates. Eurozone’s retail sales for June and the UK services PMI for July are also coming out.

From the US, besides the employment data, we get final services and composite PMIs for July, as well as the ISM non-manufacturing index for the month. From Canada, we have the trade balance for June.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

FX and CFDs are leveraged products. They are not suitable for every investor, as they carry high risk of losing your capital. You should be aware of all the risks associated with trading on margin. Please read the full Risk Disclosure.