Last week was an eventful one, with equity markets sliding due to fresh concerns over the US-China trade saga, as well as the inversion of the US Treasury yield curve. What’s more, on Friday, OPEC and its allies agreed to cut production by 1.2mn bpd, which helped oil prices to rebound. This week appears very busy as well, with the epicenter being the Brexit vote in the UK Parliament. We also have three G10 central banks holding their last meetings for the year: the Norges Bank the SNB and the ECB.

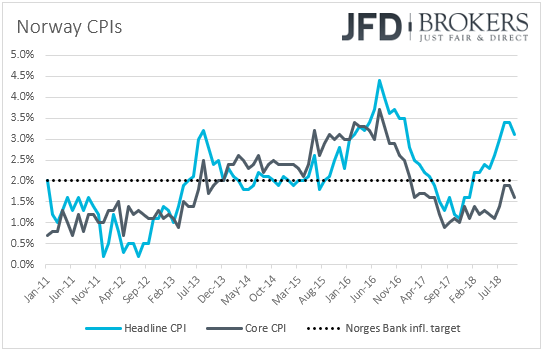

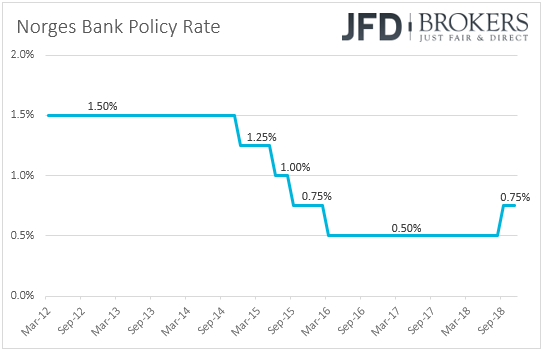

On Monday, during the European morning, we get Norway’s CPIs for November. Expectations are for the headline rate to have stayed unchanged at +3.1% yoy, but for the core one to have rebounded to +1.8% yoy from +1.6% in October, after falling to that print from September’s +1.9%. It would be interesting to see whether the rebound in the core rate would be enough for Norges Bank officials to maintain their view for another rate increase in Q1 2019, or whether the slowdown in economic growth would prompt them to change their mind (See Thursday).

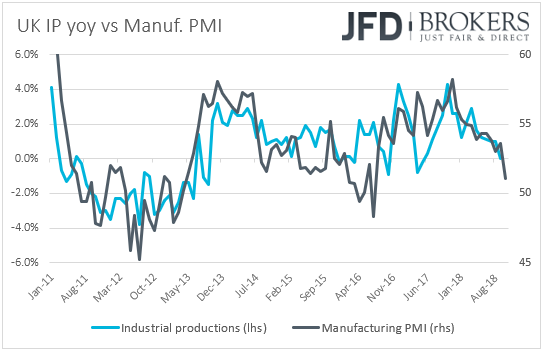

From the UK, we get industrial and manufacturing production data for October. Industrial production is expected to have slid 0.4% mom after stagnating in September, something that is likely to drive the yoy rate into negative territory. Manufacturing production is expected to have slowed to +0.1% mom from +0.2%, which is likely to drive the yoy rate down to +0.4% from +0.5%. The case for declining yoy rates is also supported by the UK manufacturing PMI for the month, which slid to 51.1 from 53.6 in September. We get also get the nation’s monthly GDP for October, as well as the NIESR GDP estimate for the three months ending in that month.

Having said all that though, we expect the UK data to attract less market attention than usual. The only driver in town for the British pound remains Brexit, and Monday is likely to be no exception. Following remarks by an EU senior legal advisor last Tuesday, who said that the UK could revoke its divorce notice without the saying of other member states, the EU’s Court of Justice will officially decide whether the nation can actually reverse Brexit. The decision comes just a day before the UK Parliament vote over the withdrawal deal agreed by PM Theresa May and EU officials.

Later in the day, we get the US JOLTs Job openings for October. Canada’s housing starts for the same month and building permits for November are also due to be released.

On Tuesday, all lights are likely to fall on the vote of the UK Parliament over the Bexit deal agreed by PM Theresa May and the EU. Given the opposition from all sides, the plan is highly unlikely to pass through the Parliament and thus, the big question is what happens in the aftermath of the vote.

Reports that the UK could revoke its Brexit notice if it wants to do so and a vote giving more power to Parliament of what happens next if the plan gets rejected may have reduced the likelihood of a disorderly exit on the 29th of March. However, following the reports over reverting Brexit, May’s spokesman said that the government is not going to proceed with revoking its notice, and let’s not forget that the EU has repeatedly noted that the agreed plan is not negotiable. Although a report last week said that the EU could consider some Brexit tweaks at the EU summit scheduled for Thursday and Friday, it is doubtful that those tweaks would prove game changers.

Therefore, if MPs decide to take the deal down, it would be hard for them convince the EU in accepting any significant amendments. In order to avoid a disorderly Brexit, they would have to revert Brexit, and with the government clearly saying that it won’t revoke its notice, the options may be a second referendum or a no-confidence vote that could lead to general elections. Having said that though, hardliners within the Parliament may not like the idea of staying within the EU. After all, they reject the existing plan because it keeps the UK closely tied to the EU. Thus, they may prefer to accept May’s accord in a second round of voting, if May’s defeat in the first vote is by a tight margin.

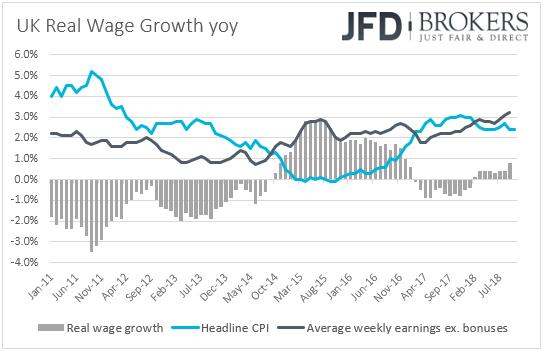

As for Tuesday’s economic data, in the UK, we get the employment report for October. Expectations are for the unemployment rate to have remained unchanged at 4.1%, while average weekly earnings, both including and excluding bonuses, are anticipated to have grown at the same pace as in September (+3.0% yoy and 3.2% yoy respectively). The case is supported by the IHS Markit/REC Report on Jobs for the month, which noted that starting salaries continued to rise sharply, with the rate of inflation holding close to September’s 41-month record. In any case, this is likely to be another UK release overshadowed by politics, especially with the Parliament vote scheduled on the same day.

From Germany, we have the ZEW survey for December. Both the current conditions and economic sentiment indices are expected to have declined to 55.6 and -25.0, from 58.2 and -24.1 respectively.

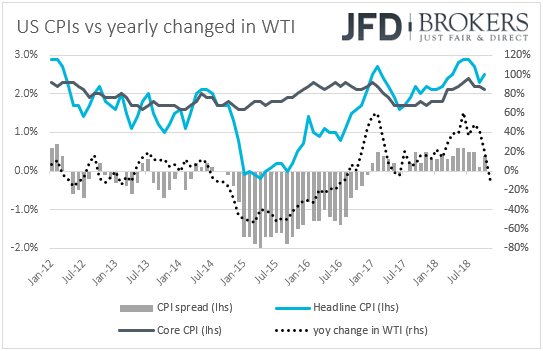

Later in the day, the US PPIs for November are coming out. The headline PPI rate is forecast to have declined to +2.5% yoy from +2.9%, while the core rate is anticipated to have remained unchanged at +2.6% yoy. This could raise some speculation that the CPIs, due out on Wednesday, may move in a similar fashion.

On Wednesday, during the European morning, we get November inflation data from Sweden. Both the CPI and CPIF rates are anticipated to have declined to +2.0% yoy and +2.2% yoy from +2.3% and +2.4% respectively. That said, once again, we will pay more attention to the core CPIF metric, which excludes energy. At its latest policy gathering, the Riksbank maintained the view that interest rates will be raised either in December or February. Since then, October’s CPI data disappointed somewhat, with the core CPIF rate ticking down to +1.5% yoy from +1.6% yoy. Thus, another decline in this inflation metric could raise speculation that the Bank may refrain from hiking at its upcoming gathering, and instead note that interest rates could rise in February.

We get November CPIs from the US as well. The forecasts suggest that the headline CPI slowed to +2.2% yoy from +2.5%, but the core rate ticked up to +2.2% from +2.1%. The case for a slowdown in headline inflation is supported by the forecast of the headline PPI for the month, the rate of which is expected to have declined as well. However, the core PPI rate is anticipated to have remained unchanged and thus, we see the risks surrounding the core CPI forecast as tilted somewhat to the downside. The pattern suggests that the decline in the headline print may be owed to the latest tumble in energy prices.

In any case, even if the core CPI accelerates somewhat, we don’t expect something like that to change much expectations around the Fed’s future plans. Following the dovish remarks by Fed Chair Powell, the minutes from the latest FOMC meeting, and last week’s WSJ report which said that Fed officials are considering whether to adopt a wait-and-see approach after hiking at their next meeting, the market sees only 1 hike throughout 2019. A few weeks ago that number was around 2. Friday’s employment report did not help revive expectations for more hikes either.

On Thursday, we have three G10 central banks holding their last monetary policy gatherings for the year: the Norges Bank, the SNB and the ECB.

Kicking off with the Norges Bank, at its latest meeting, the Bank kept interest rates unchanged at +0.75% – after raising them from +0.50% in September – and repeated that the key policy rate would most likely increase further in Q1 2019. The bank has also noted that from the September meeting, the balance of risks did not change substantially.

Since then, both headline and core inflation metrics slowed in October, to +3.1% yoy and +1.6% yoy from +3.4% and 1.9% respectively, while mainland GDP for Q3 slowed to +0.3% qoq from 0.7% in Q2. As we already noted, data on Monday are expected to show that the headline inflation rate remained unchanged, while the core one is expected to have rebounded.

Although the headline inflation rate remains well above the Bank’s objective of 2.0%, it is just a tick below the Bank’s projection for the month, which is at +3.2%. The core CPI rate, if Monday’s forecast is met, would be above the Bank’s estimate, but GDP growth is well below the +0.7% qoq forecast. So, having all these in mind, although the Bank is not expected to proceed with any changes in interest rates at this meeting, it would be interesting to see whether officials will decide (or not) to push further back the timing of when they expect rates to rise further.

Moving on with the SNB, when they last gathered, Swiss policymakers kept their benchmark rate unchanged at -0.75%, reiterating that they will remain active in the FX market as necessary and repeating that the Swiss franc is highly valued. They also revised down their inflation forecasts, suggesting that the CPI rate is likely to hit the Bank’s 2% target in Q2 2021. The decision was taken at a time when the rate was at +1.2% yoy and this was conditional upon interest rates staying at current levels for the whole forecast horizon. Last Tuesday, Switzerland’s inflation slowed to +0.9% yoy in November from 1.1% yoy, which is in line with the Bank’s projections for Q4. Thus, we see it unlikely for SNB officials to change their stance around policy at this gathering.

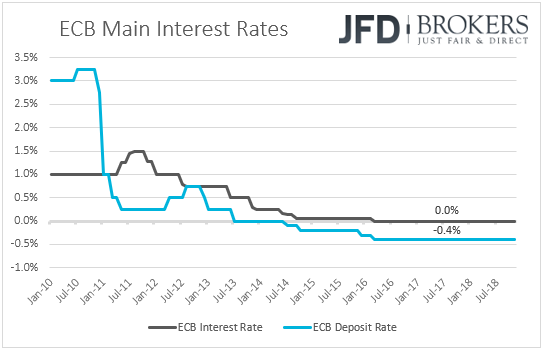

Now let’s pass the ball to the ECB. When they last met, ECB policymakers decided to keep policy unchanged as was widely expected, while the accompanying statement contained no surprises. The Bank reiterated its view that asset purchases are likely to end in December but did not confirm it. It kept the decision subject to incoming data confirming the medium-term inflation outlook.

At the press conference following the decision, President Draghi downplayed the softness in data releases saying that the risks surrounding the Euro-area economic outlook remain broadly balanced. Since then, data continued to come on the soft side. GDP growth slowed to 0.2% qoq in Q3 from 0.4% in Q2, while the composite PMI for November hit its lowest level since September 2016. With regards to inflation, according to preliminary data, both the headline and core rates slid to +2.0% yoy and +1.0% yoy in November from +2.2% and +1.1% respectively.

Therefore, we expect market attention to fall on whether the Bank will confirm the end of asset purchases this month and whether President Draghi will continue seeing balanced risks with regards to the bloc’s economic and inflation outlooks. When he testified before the European Parliament’s Economic and Monetary Affairs Committee on the 26th of November, the ECB Chief acknowledged the recent loss in growth momentum, but noted that some of the slowdown may be temporary. He also repeated that he still anticipates bond purchases to end in December. Since then, his remarks were echoed by several ECB members, something suggesting that the Bank is unlikely to alter its plans for ending QE, and that policymakers may maintain the view that the risks surrounding the bloc’s economic outlook remain broadly balanced.

Finally, on Friday, during the Asian morning, we get China’s fixed asset investment, industrial production and retail sales, all for November. Both fixed asset investment and retail sales are expected to have accelerated to +5.8% yoy and +9.0% yoy from +5.7% and +8.6% respectively, while the industrial production yearly rate is anticipated to have held steady at +5.9%. In Japan, we have the Tankan survey for Q4. Both the large manufacturers and large non-manufacturers indices are expected to have declined to 17 and 21 from 19 and 22 respectively.

During the European day, we get preliminary PMIs for December from several European nations and the Eurozone as a whole. The bloc’s manufacturing index is anticipated to have held steady at 51.8, while the services index is forecast to have ticked up to 53.5 from 53.4. This is likely to leave the composite PMI unchanged at 52.7. Eurozone’s wages and the Labor Cost Index for Q3 are also coming out but no forecasts are currently available.

We get preliminary PMIs for December from the US as well. The Markit manufacturing print is expected to have declined to 55.1 from 55.3, while the services index is forecast to have risen somewhat, to 55.0 from 54.7. The US retail sales and industrial production, both for November, are also scheduled to be released. Retail sales are anticipated to have slowed in both headline and core terms, while industrial production is expected to have accelerated somewhat.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2018 JFD Brokers Ltd.