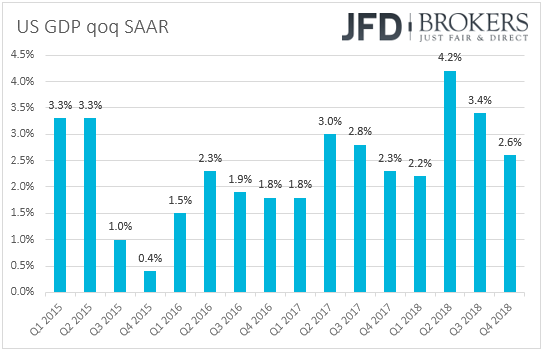

The dollar traded north yesterday after preliminary data showed that US GDP growth slowed to +2.6% qoq SAAR from 3.4% in Q3. Although this was in line with consensus according to some economic calendars, it was better than expected according to others, and prompted investors to reduce their bets with regards to a Fed rate cut. As for today, EUR-traders are likely to turn their attention to Eurozone’s inflation data for February, as they try to assess whether the ECB will hike later this year (or not).

Dollar Strengthens After Preliminary US GDP Data

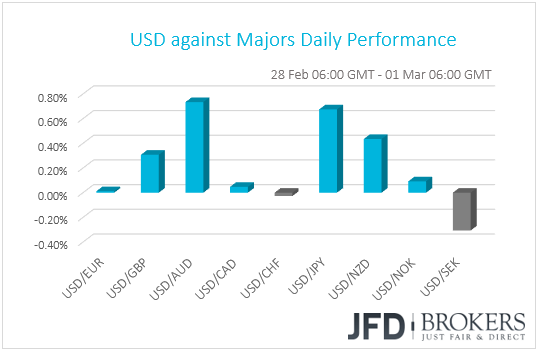

The dollar traded higher or unchanged against all but one of the other G10 currencies on Thursday. It gained against AUD, JPY, NZD and GBP, while it traded virtually unchanged against EUR, CAD, CHF, and NOK. The only currency that managed to eke out some gains was SEK.

The dollar came under buying interest yesterday after preliminary data showed that US GDP growth slowed to +2.6% qoq SAAR from 3.4% in Q3. Although this was inline with consensus according to some economic calendars, it was better than expected according to others. What’s more, as we noted yesterday, the Atlanta Fed GDPNow model had suggested a +1.8% growth rate, which may have led some to anticipate a much worse figure. For the whole year, GDP was up 2.9%, which is just shy of President’s Trump administration’s 3% target, and the strongest since 2015.

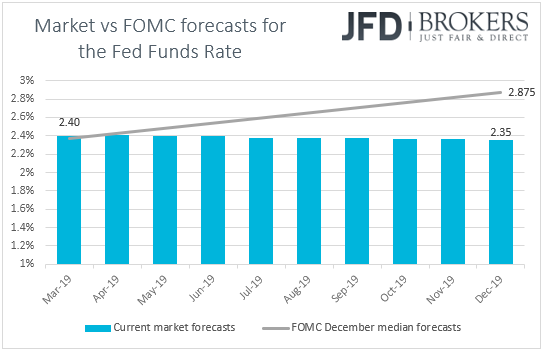

According to the Fed funds futures, the release may have encouraged market participants to reduce their rate-cut bets for this year, but failed to boost notably speculation with regards to a hike. The probability for a cut decreased to 6% from 14% yesterday morning, while the hike percentage just ticked up to 4% from 3%, with the market being nearly 90% confident that the FOMC will not push the hiking button in 2019.

Focus for USD-traders could now slowly start turning to the upcoming Fed gathering, scheduled for March 20th. It will be one of the “bigger” meetings, which are accompanied by updated economic projections and a new “dot plot”. According to the minutes of the latest meeting, all participants are willing to stop reducing their balance sheet later this year, while during his congressional testimony this week, Chair Powell said that the Committee is close to finalizing such a plan. With regards, to interest rates, the minutes revealed split views. Several members suggested that a hike would be necessary only if inflation accelerates higher than their baseline outlook, while several others argued that they see the case of raising rates later this year as appropriate, even if the economy evolves as expected.

Thus, the attention is likely to fall on whether the Fed will indeed officially announce a stop in the reduction process of its asset holdings, but most importantly, investors are likely to lock gaze on the new dot plot. The December plot suggests 2 hikes for 2019, but following the Fed “patient” shift in January, we expect a downside revision. That said, given that the market is not anticipating any increases throughout the year, a plot suggesting even one hike by December 2019 could be enough to support the greenback.

The Swedish Krona was the only G10 currency that managed to gain ground against the US dollar. SEK rallied during the European morning yesterday, after data showed that the Swedish economy expanded twice as fast as the forecast suggested. Specifically, Sweden’s GDP grew +1.2% qoq in Q4 from an upwardly revised -0.1% in Q3, beating estimates of +0.6%, something that drove the yoy rate up to +2.4% from +1.5%. Following the disappointing inflation data for January, which may have raised concerns with regards to the Riksbank’s ability to proceed with its plans and push the hiking button during the second half of the year, the strong GDP growth rate for Q4 may have revived expectations on that front. That said, the next Riksbank gathering is scheduled for April 25th, and up until then, we have the February and March inflation data. Thus, we prefer to wait for these numbers before we start examining whether the world’s oldest central bank will decide to stick to, or alter, its plans.

USD/JPY – Technical Outlook

Finally, USD/JPY managed to get above its key resistance at 111.13 and pushed further up to break another important barrier, at 111.40, which is the high of December 26th. The pair created a higher high and seems to be picking up momentum, which may lead it towards higher levels. For now, we remain bullish and will continue aiming higher.

If the bulls continue to dictate the rules, USD/JPY may continue sailing north, where its next potential destination might be around the 112.10 hurdle, marked by the low of December 19th. This is where the rate hold-up may occur. The pair could then correct itself a bit lower, but if it continues to trade above the 111.40 level, this may be a good sign for the bulls to step in again and drive USD/JPY higher, which may lead to a break of the 112.10 obstacle. Such a move could open the door to the pair’s next potential target, at 112.65, marked by the high of December 19th.

Alternatively, a drop back below the previously-mentioned 111.13 level, could temporarily spook the buyers from the field and the allow the pair to correct a little bit lower. The rate may fall to test the yesterday’s low, at 110.66, which if broken could send the pair towards the short-term upside support line, drawn from the low of January 3rd.

![]()

EUR-Traders Turn Attention to Euro Area Inflation

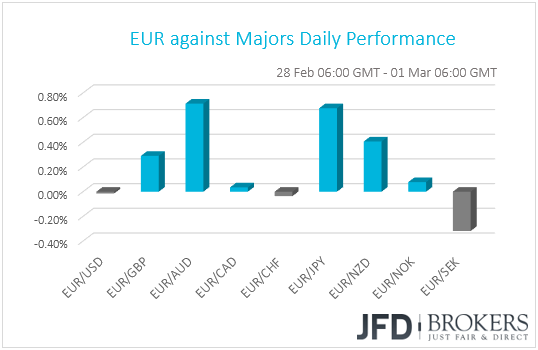

The euro was found virtually unchanged against its US counterpart this morning, which means that it traded in a similar fashion against the other G10 currencies. It gained the most against AUD and JPY, while it lost ground only against SEK.

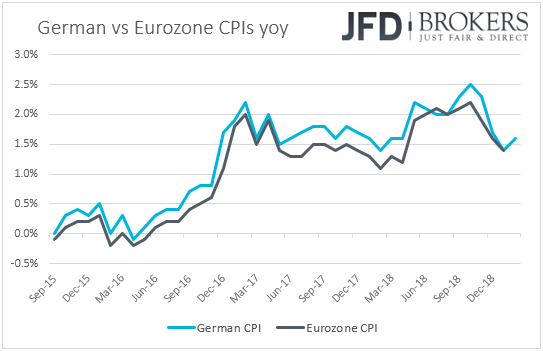

Today, traders of the common currency are likely turn their attention to Eurozone’s preliminary inflation data for February. Expectations are for the headline CPI rate to have ticked up to +1.5% yoy from +1.4%, while the core one is anticipated to have held steady at +1.1%. The case for a higher headline print is supported by yesterday’s French and German rates, which both rose.

At the latest ECB meeting, policymakers reiterated that interest rates are likely to remain unchanged “at least through the summer of 2019”, but at the conference following the decision, ECB President Mario Draghi noted that the risks surrounding the bloc’s economic outlook have “moved to the downside”. What’s more, he said that the markets place the first hike in 2020 and this shows that they understood the Bank's reaction function, something that was mentioned in the minutes of that meeting as well. Although last week’s PMIs were overall better than expected, with the composite index slightly rising after six consecutive slides, they are far from suggesting a rebound in the bloc’s economic activity.

Thus, even if the headline CPI rate ticks up, an unchanged core print would still be well below the Bank’s objective of “below, but close to 2%” and may allow market participants to keep on the table their bets with regards to no action by the ECB this year. That said, given that the “at least through summer of 2019” is an open-ended notion, a higher headline inflation print may ease pressure on policymakers to revise their guidance when they meet next week.

EUR/AUD – Technical Outlook

Once again, EUR/AUD is knocking on the door of the upper bound of the range, in which the pair continues to trade. The range is between the 1.5725 and 1.6040 levels. Of course, before we examine the upside, we would like to see a firm break above the upper bound, but until then we will remain cautiously-bullish and will continue carefully monitoring the price action.

As mentioned above, a push above the 1.6040 barrier may open the door to some higher areas, where the first good potential resistance zone could be found near the 1.6110 hurdle. The last time that hurdle got tested was on January 9th. If the buying remains strong, then a push above 1.6110 could lead to a test of the 1.6155 barrier, which is the peak of January 19th. Slightly above lies another potential resistance area, at 1.6190, which marks the inside swing low of January 2nd.

On the other hand, if the pair fails to get above the upper side of the aforementioned range, this is where the bears may take control, especially if EUR/AUD moves below the 1.5995 obstacle. This could keep the pair within the aforementioned range for a while more and might clear the path for a further slide, towards the 1.5900 support zone, which on February 26th acted as a good resistance, until it was broken the following day. If the selling doesn’t end there, EUR/AUD may continue feeling the bear-pressure and slide further south, where the next support might be seen near the 1.5810 level. This level is the low of this week.

![]()

As for the Rest of Today’s Events

During the European morning, besides the Euro area inflation data, we get final manufacturing PMIs from several European nations and the Eurozone as a whole. As it is usually the case, the final numbers are expected to confirm the preliminary estimates. We get the February manufacturing PMI from the UK as well and expectations are for the index to have slid again, to 52.0 from 52.8.

In the US, personal income and spending for December, as well as the core PCE rate for the month are due to be released. Expectations are for income to have accelerated somewhat, to +0.3% mom from +0.2%, while spending is expected to have slid 0.2% mom after rising 0.4%. The case for accelerating income is supported by the increase in the average hourly earnings monthly rate for the month while the 1.2% mom slump in retail sales suggests that the risks surrounding the spending forecast may be tilted to the downside, perhaps for a larger-than-expected decline. As far as the core PCE rate is concerned, it is expected to have stayed unchanged at +1.9% yoy, which is supported by the core CPI rate for the month, which also held steady. The final Markit manufacturing PMI for February, as well as the ISM manufacturing index for the month are also coming out. The Markit print is expected to confirm the first estimate, but the ISM index is expected to have slid to 55.5 from 56.6.

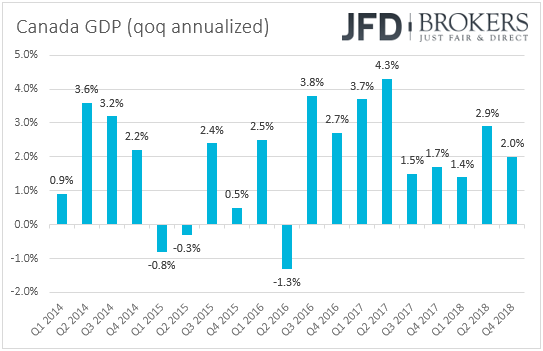

From Canada, we get GDP data for December and Q4. The monthly rate is forecast to have risen to 0.0% from -0.1% mom, something that is likely to drive the qoq annualized rate for Q4 down to +1.2% from +2.0%. Following November’s negative rate and the slide in both the headline and core inflation rates for January, a decent rebound is needed for CAD-traders to start examining whether the next BoC hike can occur this year. Although last week, Governor Poloz reiterated that the Bank’s plans continue to be of more rate increase over time, he also noted that the timing is “highly uncertain”. Thus, another soft set of GDP data could keep rate-hike expectations well into the future.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Group, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Group analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD Group prohibits the duplication or publication without explicit approval.

76% of the retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2019 JFD Group Ltd.