The US dollar came under strong selling interest yesterday following comments by several FOMC members, who noted that they should wait before proceeding with more rate hikes. The Bank of Canada kept interest rates unchanged but maintained the view that more hikes may be warranted over time. On the trade front, the US-China talks concluded on a positive note, but with no final accord. As for today, EUR-traders are likely to focus on the minutes from the latest ECB meeting.

Greenback Tumbles on Fed Speakers, ECB Minutes in Focus

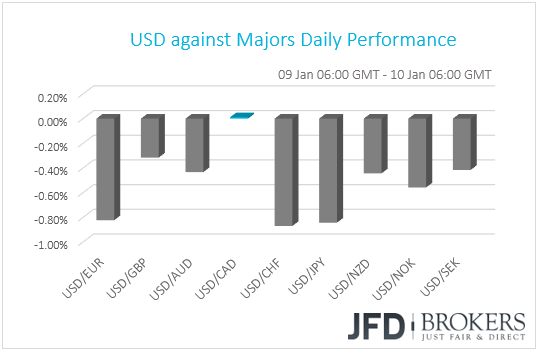

The US dollar traded lower against all but one of the other G10 currencies yesterday. The only currency that did not manage to outperform the US currency was CAD, with USD/CAD ending the day virtually unchanged. The main winners were CHF, JPY and EUR in that order, while the currency that gained the least was GBP.

The driver behind the dollar’s tumble were remarks by a number of Fed members, who said that they would wait before proceeding with more rate increases. Chicago President Evans and Boston President Rosengren supported more hikes this year but noted that they can wait, as more clarity is needed before adjusting policy. St. Louis President Bullard said that rates are in the right place and that no more are warranted but given that he is the most dovish voting member, this was to be expected. The main trigger for the tumble in the US dollar were remarks by Atlanta President Bostic, who also said that the Fed should wait to see how the economy evolves, but was the only one to note that policy could move in either direction and that he is open to a rate cut if downside risks all “come to bear”.

The minutes from the latest FOMC meeting were also published yesterday, with the dollar reacting little at the time of the release. Yesterday, we said it would be better to pay more attention to what Fed officials have to say at this point in time rather than the minutes. In any case, the minutes revealed that a number of policymakers said they could be patient about future interest rate increases, something that was more or less expected bearing the aforementioned remarks and last week’s dovish stance by Chair Powell. An interesting point, in our view, was that, even though voting members unanimously backed the December rate increase, a few others did not support the action.

As for today, we get more minutes, this time from the ECB. At its previous meeting, the Bank formally ended its asset purchasing program, while at the press conference following the decision, President Draghi noted that “The risks surrounding the euro area growth outlook can still be assessed as broadly balanced.” However, he added that the balance of risks is moving to the downside due to the persistence of uncertainties related to geopolitical factors, the threat of protectionism, vulnerabilities in emerging markets and financial market volatility.

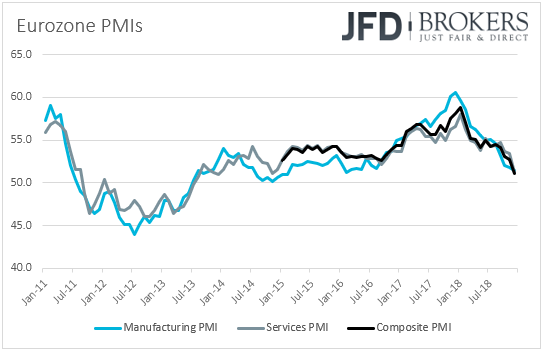

Since then, data has kept coming in on the soft side, with Eurozone’s composite PMI hitting its lowest since November 2014, headline inflation slowing by more than anticipated and the core CPI rate staying stubbornly at +1.0% yoy, well below the Bank’s objective of “below, but close to 2%”. This may have raised speculation that Draghi and co. may have to change their language around the economic outlook soon, noting that the risks have shifted to the downside. So, investors may dig into the minutes to find out how close to something like that the Bank is, and whether there were some officials already arguing for such a change to take place at that meeting.

With regards to the trade front, US and China concluded their trade talks on a positive note, but with not sealing any final deal. Remember that we’ve been highlighting throughout the week that we are skeptical whether a final accord could be reached in this round of negotiations. We stick to our guns that the next round may be at the World Economic Forum in Davos later this month, between US President Trump and China’s Vice President Wang Qishan. Although not clear by the FX performance, major equity indices closed in the green yesterday, suggesting that market participants remain confident that the two nations will soon reach common ground.

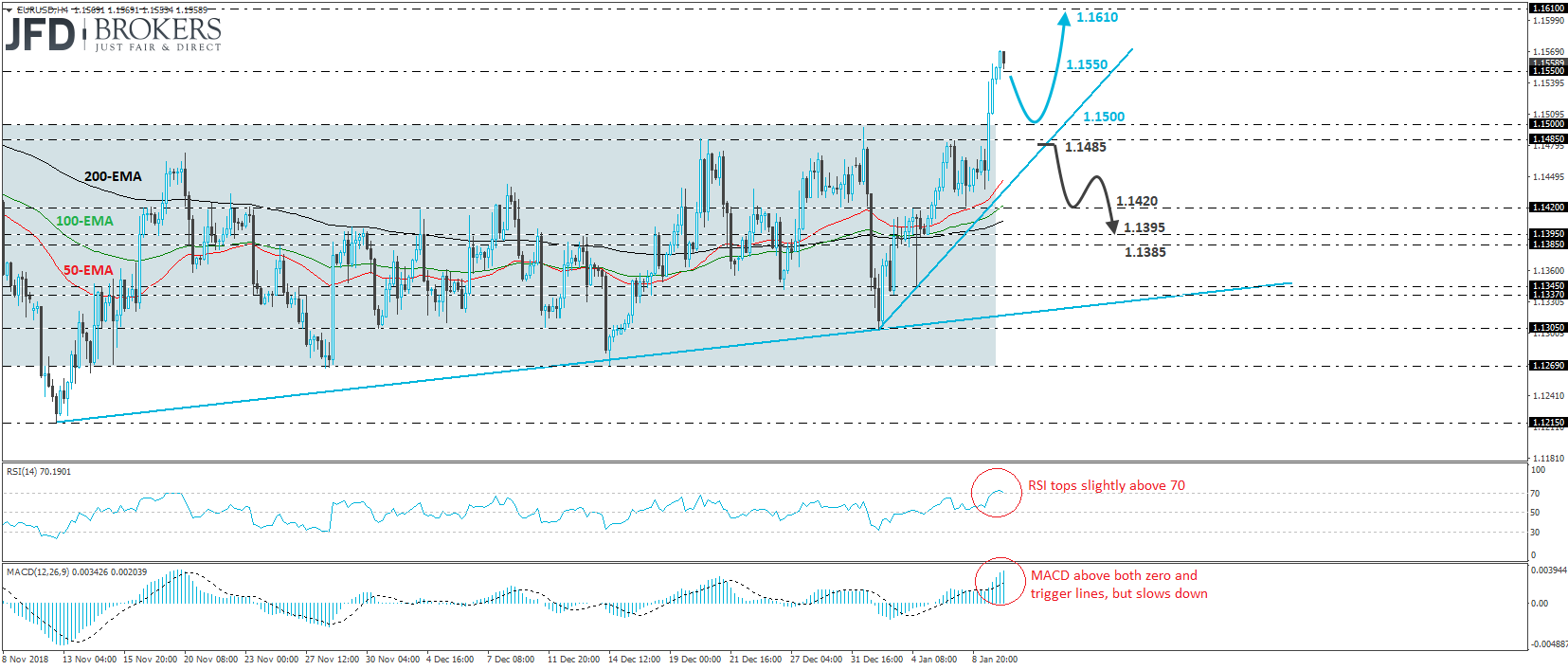

EUR/USD – Technical Outlook

EUR/USD surged yesterday, breaking above the psychological zone of 1.1500, which was also the upper bound of the sideways range that had been containing most of the price action since the 22nd of October. Subsequently, the pair emerged above the 1.1550 barrier, marked by the high of that day. In our view, the exit out of the aforementioned range suggests that there is further upside potential for this exchange rate.

We believe that the bulls may take charge again in the near future and perhaps aim the 1.1610 territory, which acted as a decent resistance from the 12th until the 16th of October. However, before the next positive leg, given yesterday’s steep rally, we see the case for a retreat back below 1.1550, perhaps for the pair to challenge the 1.1500 zone as a support this time.

Our view for a pullback is also supported by our short-term oscillators. The RSI topped within tis above-70 zone and now looks ready to fall back below 70, while the MACD, although above both its zero and trigger lines, shows signs of slowing down.

In order to abandon the bullish case, we would like to see EUR/USD closing back below 1.1485. This could confirm the rate’s return back within the aforementioned range, as well as the break below the short-term upside support line taken from the low of the 2nd of January. The bears may then drive the battle lower, towards the 1.1420 area, the break of which could extend the slide towards the 1.1395 or the 1.1385 levels.

BoC Still Anticipates More Hikes, GBP-Traders Keep Gaze Locked on Brexit

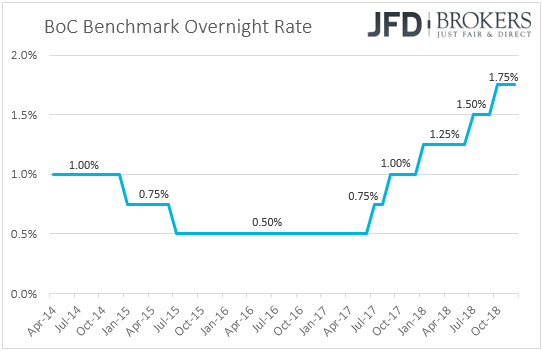

The Canadian dollar strengthened at the time the BoC announced its rate decision but gave back the gains later in the day to trade virtually unchanged against its neighboring US dollar. The Bank decided to keep its interest rate unchanged at +1.75% as was widely anticipated, while the statement did not paint a particularly different picture than the previous time. So why did the Canadian dollar strengthen at the time of the release?

Remember that yesterday, we noted that for the Loonie to decline, a statement more dovish than the previous one was needed. The Bank reiterated its concerns with regards to the latest slide in oil prices noting that it has a material impact on the Canadian outlook and that the nation’s oil sector is projected to weaken further. What’s more, officials noted that growth has been running close to potential, which is a somewhat more sanguine note compared to the part saying, “there may be additional room for non-inflationary growth”, which was included in the previous statement. With regards to inflation, they acknowledged the slowdown in headline inflation, noting that this was expected due to the lower gasoline prices, and that it is projected to edge further down. Most importantly though, the Governing Council kept the view that interest rates are likely to increase further into a neutral range, something that may disappointed those who thought that the Bank of Canada is finished raising rates, and that’s why the Loonie may have strengthened at the time of the release.

The pound was the third weakest currency on the G10 least, behind the US and Canadian dollars. Yesterday, May’s Brexit plan took another hit after the Parliament voted that the government comes up with an alternative plan within three working days if the existing deal is rejected next week. In our view, unless May manages to secure concessions from the EU and convince MPs to support her deal, something we see as very unlikely, the deal is doomed to be voted down. A good question is: What happens if the Parliament votes down the deal and the government does not return with an alternative within three days? With all this uncertainty surrounding the UK’s future, we maintain the view that the pound may stay pressured and that any rallies are likely to be short-lived, at least until the fog clears out.

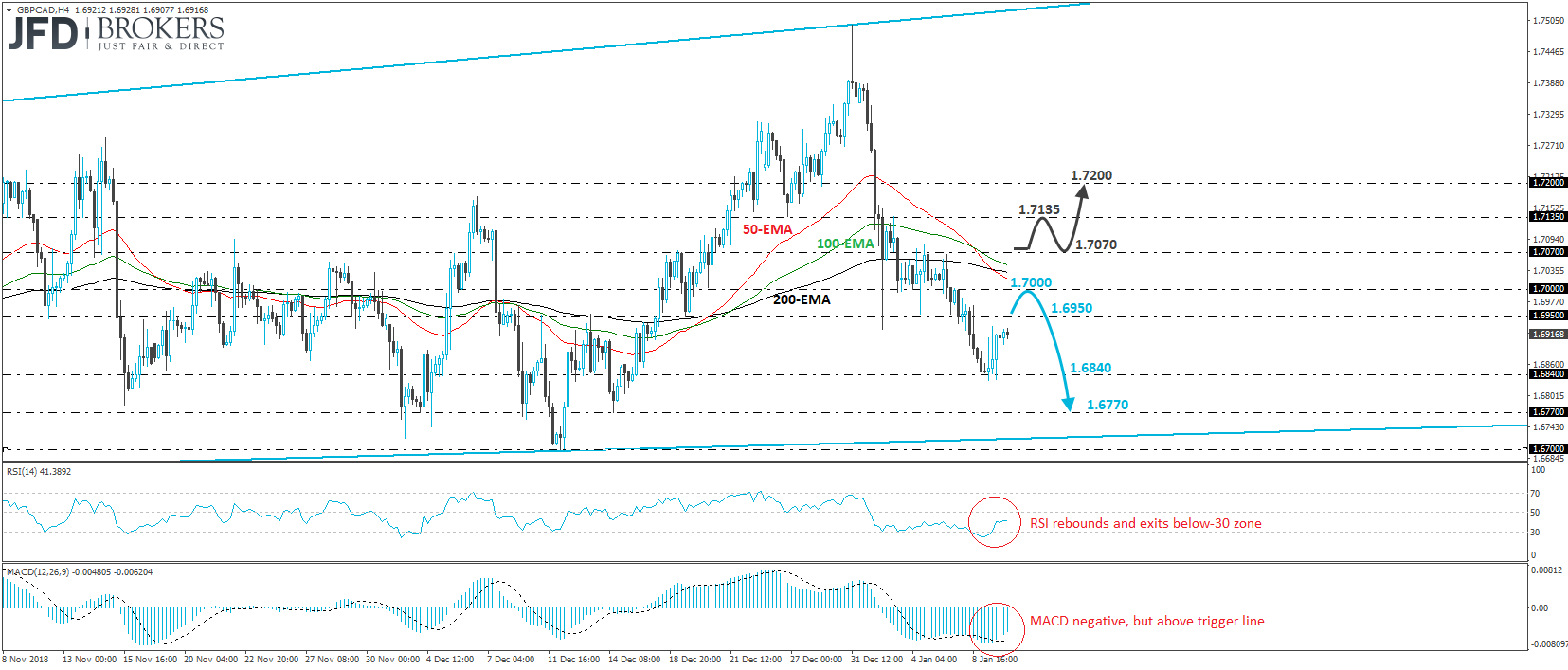

GBP/CAD – Technical Outlook

GBP/CAD traded higher yesterday, after it hit support near the 1.6840 zone. Although in the bigger picture, the pair continues to trade above the upside support line drawn from the low of the 15th of August, in the short run, the price structure still suggests a near-term downtrend, which still has some way to go before the rate hits that upside support line. Therefore, even if the rate corrects somewhat higher, we would stay cautiously negative for now.

The current recovery may continue towards the 1.6950 level, or even the psychological zone of 1.7000, but we expect the bears to take charge from near those territories and push the rate back down, perhaps for another test near the 1.6840 hurdle. If that barrier fails to halt the decline this time, then we may experience extensions towards the low of the 14th of December, at around 1.6770, which is slightly above the aforementioned medium-term upside support line.

Looking at our short-term momentum indicators, we see that the RSI rebounded and exited its below-30 zone, while the MACD, although negative, has bottomed and crossed above its trigger line. These indicators support the idea for some further recovery before, and if, the bears decide to take charge again.

We would like to see a clear recovery back above 1.7070 before we start examining whether the bears have abandoned the field, and that the short-term picture has turned to a somewhat positive one. Such a break would bring the rate above all three of our moving averages and may initially aim for the 1.7135 resistance hurdle. Another break above 1.7135 may allow the bulls to lift the pair towards the 1.7200 zone.

As for the Rest of Today’s Events

Norway’s inflation data are already out. The headline CPI rate held at +3.5% yoy, instead of ticking down to +3.4% yoy as was expected, while the core declined to +2.1% yoy from +2.2%. The core forecast was for a slide to +2.0% yoy. In our view, this data keeps the Norges Bank on course for hiking again in March.

Later in the day, apart from the ECB minutes, we also get the US initial jobless claims for the week ended on the 4th of January, as well as Canada’s building permits for November. Initial jobless claims are expected to have declined to 225k from 231k, while Canada’s building permits are forecast to have fallen at a faster pace than in October.

We also have four Fed speakers on the agenda: We will get to hear again from Chair Jerome Powell, St. Louis President Bullard, and Chicago President Evans. The new person on the list is Richmond Fed President Thomas Barkin, but he is not a voting member.

As for tonight, during the Asian session, Japan’s household spending and current account data, both for November are coming out. Household spending is expected to have rebounded 0.2% yoy after sliding 0.3% yoy in October, while the nation’s current account surplus is forecast to have increased. Australia’s retail sales for November are due out as well and the forecast points to a 0.3% increase, the same pace as in October.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Group, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Group analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD Group prohibits the duplication or publication without explicit approval.

68% of the retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2019 JFD Group Ltd.