Risk appetite improved at the opening yesterday, with the US dollar coming under selling interest, as US President Donald Trump and his Chinese counterpart Xi Jinping agreed over the weekend to put tariffs on hold and try to solve their differences within 90 days. The Aussie, although it pulled back later in the day, it was one of the best performers at the opening. The currency rebounded again during the Asian morning Tuesday after the RBA appeared somewhat more upbeat.

US and China Agree to Put Tariffs on Hold

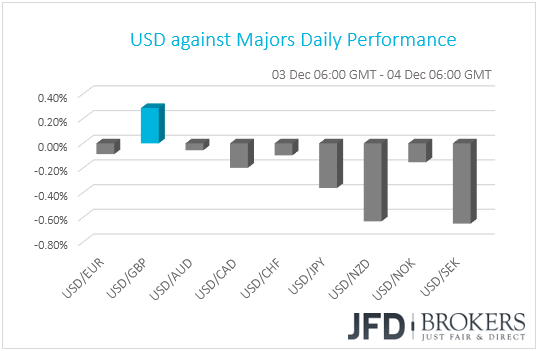

The dollar traded lower against most of the other G10 currencies on Monday. It gained only against the British pound, which came back under selling interest on concerns over the UK Parliament’s vote on Brexit next week. The main winners against the dollar were SEK, NZD and JPY.

Although not clear by the FX performance throughout the whole day, the week opened with a strong boost in risk appetite. Riskier assets, like equities and the commodity-linked currencies, opened higher, while safe-havens, like the dollar and the yen, came under selling interest. Investors’ mood was better reflected in the stock market. Following the rally on Fed Chair Jerome Powell’s dovish remarks last week, equities staged another recovery. EU and US indices were a sea of green yesterday. However, the euphoria eased during the Asian morning Tuesday.

The risk-on mood was triggered by the outcome of the meeting between US President Donald Trump and his Chinese counterpart Xi Jinping in Buenos Aires. Over the weekend, the two leaders agreed to put tariffs on hold and try to solve their differences within 90 days. On Friday, we noted that we don’t expect a final accord, but the two leaders to just agree on further talks. And this is what happened, we believe. What’s more, even though both nations said that the US will delay a tariff increase to 25% from 10% on USD 200bn Chinese imports, planned for the 1st of January, their official statements had several differences of what was agreed. For example, the 90-day deadline was not mentioned in China’s statement, neither the hot topics of technology transfer and intellectual property production, which were part of the US account.

In our view, there is not much to cheer about. This is maybe the reason why most Asian stock indices turned south today. Even if risk appetite continues to improve in the days to come, we will remain skeptical with regards to the longer-term picture as the two nations have still a long way to go before they seal a final accord. Instead of an agreement, we would characterize the outcome in Buenos Aires as kicking the can further down the road. A failure to reach common ground on several key issues, like intellectual property, may bring tensions back to the spotlight, which may weigh again on investors’ morale. On the other hand, headlines suggesting that every round of negotiations brings the two countries closer to a final deal is likely to keep market participants happy and encourage them to increase their risk exposure.

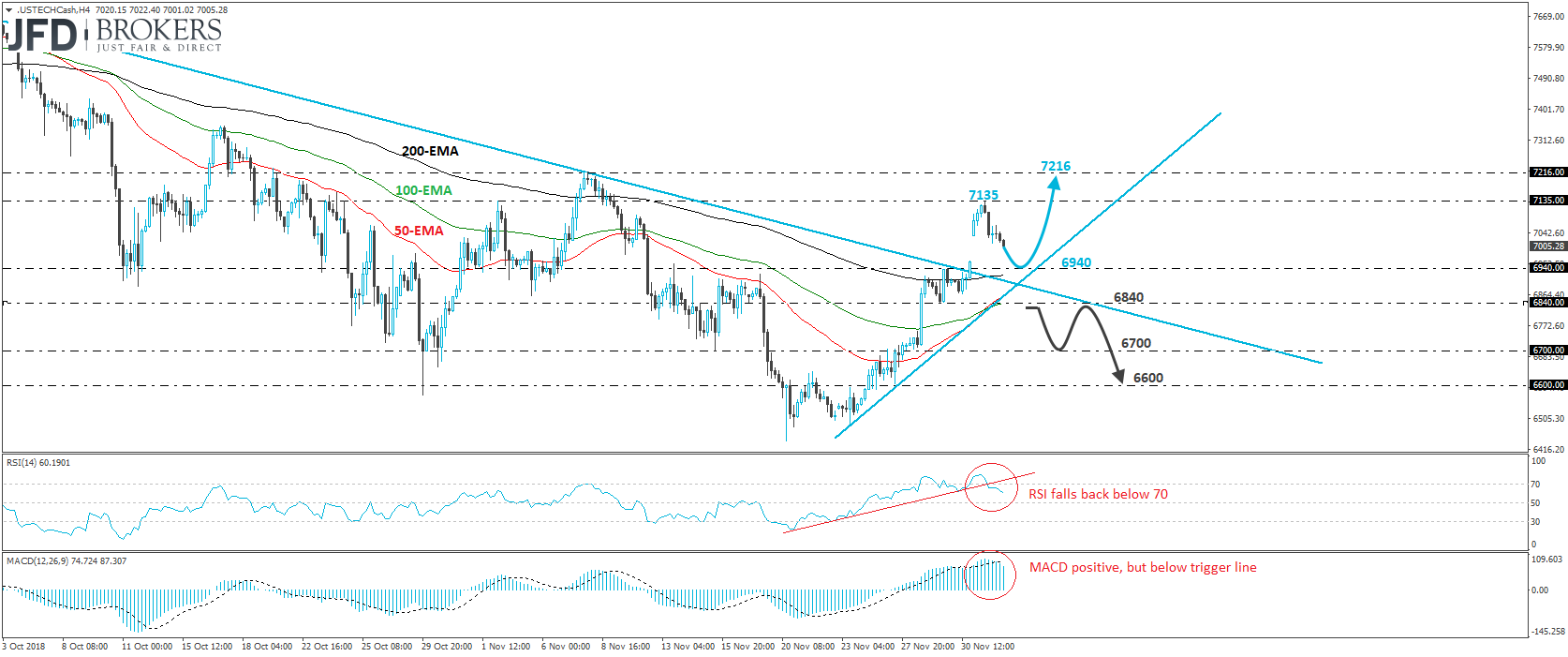

Nasdaq 100 – Technical Outlook

The Nasdaq 100 cash index opened with a positive gap yesterday, moving further above the downside resistance line drawn from the peak of the 1st of October. However, the cash index hit resistance at 7135 and then it pulled back. The price continues to trade above the aforementioned downside line, as well as above the upside one drawn from the low of the 23rd of November. Therefore, we would consider the short-term outlook to be cautiously positive for now.

We would expect the bulls to take charge again at some point soon, perhaps aiming for another test near the 7135 zone. If this time around, they managed to push through that level, then we may see them targeting our next resistance at around 7216, defined by the high of the 8th of November.

Looking at our short-term oscillators though, we see signs that some further retreat may be looming before, and if, the bulls decide to shoot again, perhaps for a test near the 6940 barrier, or the crossroads of the aforementioned two lines. The RSI has topped within its above-70 zone and moved back below 70, while the MACD, although positive, has topped as well and dipped below its trigger line.

That said, in order to abandon the bullish case and start examining whether the bears have gained the upper hand, at least in the short run, we would like to see a clear dip below 6840. Such a break may confirm the return of the index below the downside line taken from the peak of the 1st of October and could open the path for the 6700 zone. Another dip below 6700 could extend the slide towards 6600, a support marked by the low of the 27th of November.

Aussie Stays Strong After RBA

Even though the Australian dollar traded nearly virtually unchanged against its US counterpart, it was the second-best performing currency following the opening yesterday. The best performer was NZD. Both Australia and New Zealand have strong trade ties with China and that’s why their currencies were the main G10 winners following the Trump-Jinping meeting.

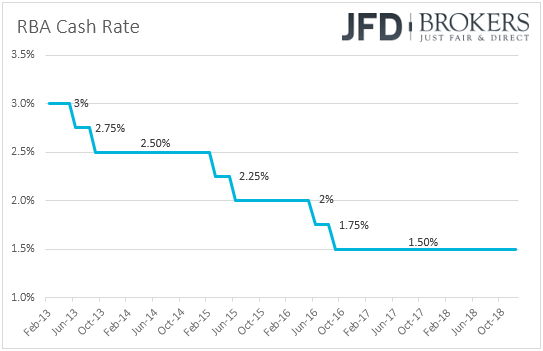

The Aussie pulled back later in the day, perhaps as investors took a more cautious stance with regards to the US-China trade saga after they dug into the details, but the RBA meeting overnight was enough to keep the setback limited. The Australian central bank decided to keep once again its benchmark interest rate unchanged at +1.50%, but the accompanying statement included some more optimistic tweaks.

The Bank reiterated that one continuing source of uncertainty for the Australian economy is the outlook for household consumption, but removed the part saying that one ongoing uncertainty for the global outlook stems from the direction of international trade policy in the US. Officials also reiterated that the Bank’s central scenario is for GDP growth to average around 3.5% over this year and the next, and maintained the view that the outlook for the labor market remains positive. They acknowledge the pick-up in wage growth and, this time around, they refrained from saying that it remains low.

That said, despite the more upbeat tone in the statement, the market reaction is far from suggesting a big changed in market expectations with regards to a hike by this Bank. According to its latest quarterly Statement on Monetary Policy, the cash rate is expected to increase in 2020. With the Bank’s upcoming gathering scheduled for the 5th of February, we expect Aussie’s near-term direction to be dictated by changes in investors’ risk appetite, and especially developments around the US-China trade sequel. However, for now, Aussie traders may want to keep an eye on the economic calendar as tonight, during the Asian morning Wednesday, Australia’s GDP for Q3 is due to be released. Expectations are for a slowdown to +0.6% qoq from +0.9% in Q2, something that could drive the yoy rate down to +3.3% from +3.4%.

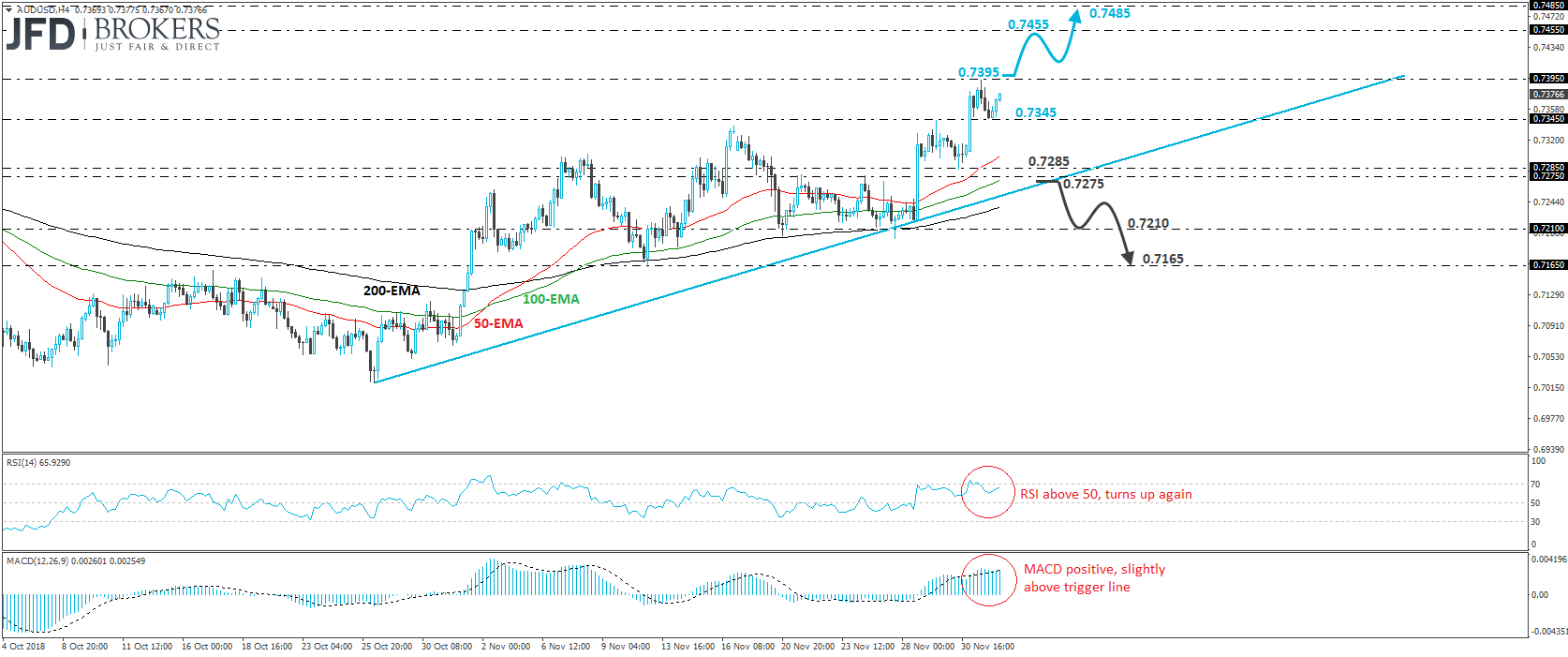

AUD/USD – Technical Outlook

AUD/USD surged at yesterday’s opening, breaking above the 0.7345 barrier, marked by the peak of the 29th of Thursday. Although the pair hit resistance at 0.7395 thereafter and retreated, the break above 0.7345 has confirmed a forthcoming higher high. What’s more, the retreat remained limited near the 0.7345, which has turned into support, and then, the rate rebounded again. Having all that in mind, as well as that the pair is trading above the upside support line drawn from the low of the 26th of October, we will adopt a positive stance for now.

We believe that the bulls may attempt to challenge once again the 0.7395 hurdle soon, and if they manage to break it, we may see extensions towards 0.7455, the high of the 9th of August. Another move above that level could pave the way towards the 0.7485 obstacle, marked by the peaks of the 9th and 10th of July.

Shifting attention to our short-term oscillators, we see that the RSI, although it exited its above-70 zone yesterday, it turned up again. The MACD, already positive, has just poked its nose above its trigger line. These indicators detect positive momentum and corroborate our view for further advances.

On the downside, even if the rate dips below 0.7345, we would still consider the short-term outlook to be cautiously positive. There would still be a decent chance for the bulls to jump in from near the aforementioned upside support line, or the 0.7285 barrier. We would like to see a clear break below 0.7275 before se start examining the case of a short-term reversal. Such a dip may set the stage for the 0.7210 zone, the break of which could curry extensions towards the low of the 13th of November, at around 0.7165.

As for Today’s Events

During the European day, Switzerland’s CPI for November is due to be released and is expected to have slowed to +1.0% yoy from +1.1%. At its latest meeting, the Swiss National Bank kept its benchmark rate unchanged at -0.75%, reiterating that it will remain active in the FX market as necessary and repeating that the Swiss franc is highly valued. It also revised down its inflation forecasts, suggesting that the CPI rate is likely to hit the Bank’s 2% target in Q2 2021. The decision was taken at a time when the inflation rate was at +1.2% yoy and this was conditional upon interest rates staying at current levels for the whole forecast horizon. Therefore, even if the CPI rate does not tick down as the forecast suggests and stays unchanged, or even rise somewhat, we see it unlikely for SNB policymakers to be tempted to alter their policy stance.

The UK construction PMI for November is also coming out and expectations are for a decline to 52.7 from 53.2 in October. Usually, the market tends to pay more attention to the services index, which comes out tomorrow, but given that the political scene has overshadowed economic developments in the UK, we don’t expect this set of PMIs to prove critical with regards to the pound’s forthcoming direction. The British currency is likely to stay anchored to headlines surrounding the Brexit landscape.

With regards to the energy market, we get the American Petroleum Institute (API) weekly report in crude oil inventories, but as usual, no forecast is available.

We also have three speakers on today’s agenda: BoE Governor Mark Carney, BoE MPC member Gertjan Vlieghe, and New York Fed President John Williams.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.