The greenback rebounded yesterday to trade higher against most of its major counterparts. Today, the US tariffs on USD 16bn Chinese goods kicked in amid talks between the two nations, with China expected to hit back. The talks continue today, but besides that, investors are likely to also focus on the Jackson Hole Symposium. The minutes from the latest ECB meeting are due to be released as well.

Fed Officials Willing to Continue Hiking, Jackson Hole Symposium Begins

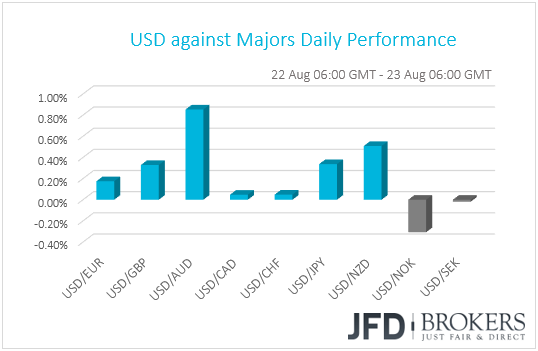

The US dollar reversed course yesterday and outperformed most of the other G10 currencies. It gained the most against AUD, NZD and JPY in that order, while it lost ground only against NOK. It traded virtually unchanged against SEK, CHF and CAD.

The Aussie was the main loser among the G10s amid growing uncertainty in Australia’s political landscape after the resignations of several senior ministers, which put PM Tunrbull’s position at risk.

Yesterday, the minutes of the latest FOMC meeting revealed that many participants expect another rise in interest rates “soon”, while it was noted that officials generally expected further gradual increases. It was also repeated that many wanted to revise the accommodative monetary policy description in the not-too-distant future. With regards to the trade front, most policymakers suggested that an escalation in trade disputes was a potentially consequential risk for economic activity.

Once again, the key takeaway is that Fed officials are willing to continue hiking rates in the foreseeable future, but they remain concerned on the trade front. At the time of the release, the dollar slid somewhat, perhaps as there was nothing new in the report, but recovered in the following minutes and continue trading north throughout the rest of the day. According to the Fed Fund futures, the probability for the next rate increase to come in September has risen to 96% from 94%, while there is now an almost 65% change for another one in December. That probability was near 61% yesterday.

With regards to the US-China trade story, the planned US tariffs on USD 16bn worth of Chinese products have already kicked in, with China saying that its own tariffs will go into effect later in the day. The tariffs come in the midst of negotiations between two sides, but as we noted on Tuesday, expectations that this round of talks would bear fruit are very low. Even President Trump said that he does not expect much progress from this round of talks.

Apart from the trade front, market participants are likely to also focus on the annual Jackson Hole Economic Symposium, which begins today. This year, the theme will be “Changing Market Structure and Implications for Monetary Policy”, and the spotlight is likely to fall on Fed Chair Powell’s speech. The Fed Chairman is scheduled to step up to the rostrum on Friday to speak on “Monetary Policy in a Changing Economy”.

AUD/USD – Technical Outlook

AUD/USD tumbled overnight, breaking back below the 0.7320 hurdle, which acted as the lower bound of the sideways range that contained the price action from the 14th of June until the 10th of August. The fall was stopped near the 0.7282 level, but bearing in mind the break back below 0.7320, we see the case for some further downside extensions.

If the bears are strong enough to take the driver’s seat again soon, then we may see them pushing the pair below 0.7282, a move that could open the way for our next support of 0.7255. Another dip below that hurdle could set the stage for the 0.7210 zone, slightly above the low of the 15th of August.

Taking a look at our short-term oscillators, we see that the RSI slid below its 50 line, while the MACD lies below its trigger line and appears ready to obtain a negative sign soon. These indicators support somewhat the notion for AUD/USD to continue drifting south in the near term.

On the upside, clear break above 0.7370 would confirm a forthcoming higher high on the 4-hour chart and could be a sign that the bulls want to keep the rate back within the aforementioned sideways range. Such a break may initially aim for the 0.7410 zone, the break of which could open the way for the crossroads of the 0.7445 resistance and the medium-term downtrend line drawn from the peak of the 16th of February.

ECB Takes its Turn in Releasing Minutes

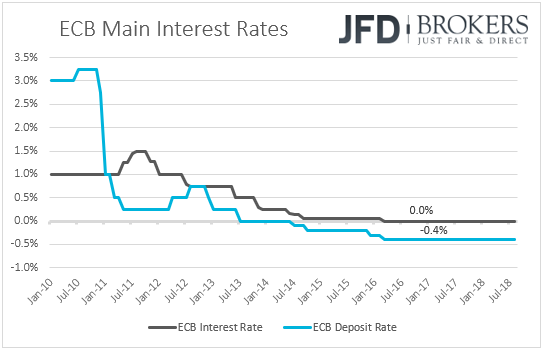

Today, the ECB takes its turn in releasing the minutes of its latest policy gathering. At that meeting, President Draghi noted that expectations of the future rate path were very well aligned with the anticipation of the Governing Council, backing the market consensus for a hike in late 2019. This may have come as a disappointment to those expecting to hear that summer months are also candidates for a rate hike.

Although following the June meeting, a report noted that officials are split over when they may hike rates, with some saying that July 2019 should not be ruled out, the minutes of that meeting showed that policymakers were unanimous to support the policy proposals. Thus, we see it very unlikely that these minutes will reveal any divisions among the Governing Council. We believe that all policymakers remain in support of the “at least through the summer of 2019” interest rate guidance, which, in our view, means that interest rates are likely to start rising in September 2019 the earliest.

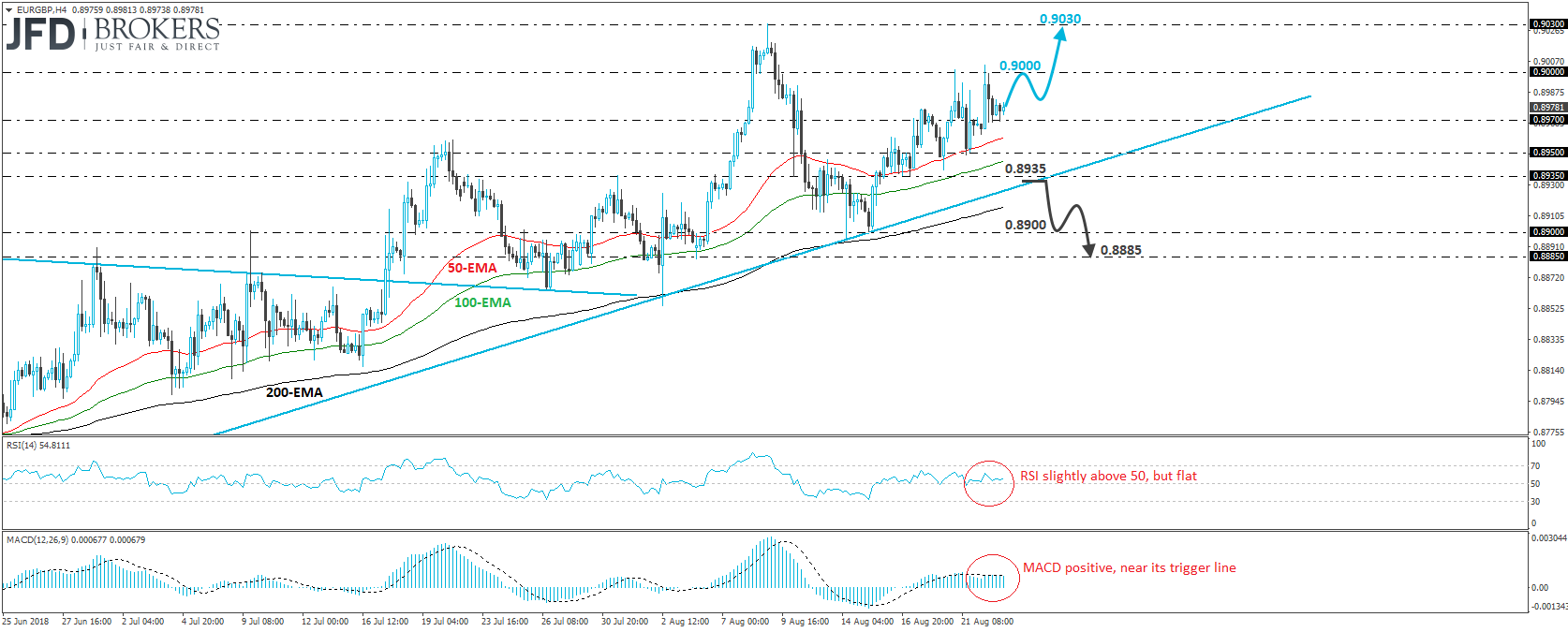

EUR/GBP – Technical Outlook

EUR/GBP traded lower yesterday after it hit resistance slightly above the 0.9000 zone. However, the pullback was stopped near the 0.8970 level and since then, the rate has been trading in a consolidative manner slightly above that barrier. Given that the pair continues to print higher peaks and higher troughs above the uptrend line drawn from the low of the 21st of June, we would consider the near-term outlook to be positive.

We would expect buyers to jump back into the action soon and perhaps drive the rate up for another test near the 0.9000 zone. If they manage to break that zone, then we may see extensions towards 0.9030, a resistance marked by the high of the 9th of August.

Both our short-term momentum studies lie within their bullish territories, but they point sideways. This make us cautious that further consolidation may be on the cards before the next positive leg, or another setback, perhaps towards 0.8950 or the aforementioned uptrend line.

But even if this is the case, we would still see a positive picture. We would like to see a clear close below the aforementioned trendline and the 0.8935 support before we abandon the bullish case. Such a dip could pave the way for the 0.8900 territory, the break of which could extend declines towards the 0.8885 level, defined by the low of the 5th of August.

As for the Rest of Today’s Events

During the European morning, besides the ECB minutes, we get preliminary manufacturing and services PMIs for August from several European nations and the Eurozone as a whole. The bloc’s manufacturing index is anticipated to have declined to 54.6 from 55.1 in July, while the services one is expected to have risen to 55.0 from 54.2. This will push the composite index a tick higher, to 54.4 from 54.3.

We get preliminary Markit manufacturing and services PMIs for August from the US as well. However, as we noted in the past, the market tends to pay more attention to the ISM indices due out on the 4th and 6th of September. New home sales for July and initial jobless claims for the week ended on the 17th of August are also due to be released.

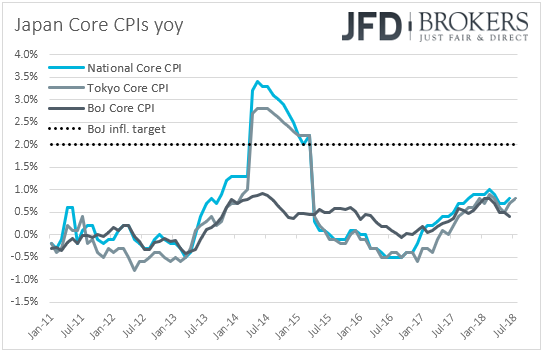

As for tonight, during the Asian morning Friday, we get Japan’s National CPIs for July. No forecast is currently available for the headline rate, while the core one is anticipated to have remained unchanged at +0.8% yoy. That said, bearing in mind that both the headline and core Tokyo CPIs for the month accelerated, to +0.9% yoy and +0.8% yoy from +0.6% and +0.7%, we see the case for the national figures to follow suit.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.