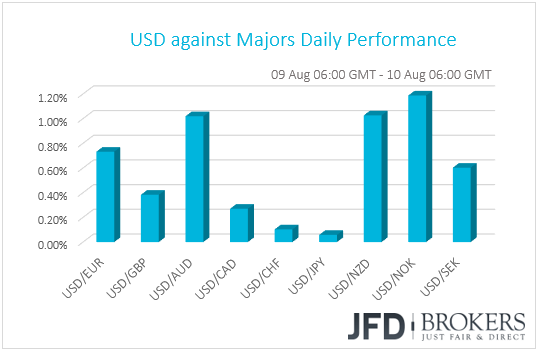

The dollar strengthened against most of its G10 counterparts on Thursday ahead of today’s US CPIs for July. The currencies that managed to resist the dollar’s strength were the safe havens CHF and JPY in what it seems to be a somewhat risk-averse market environment. Besides the US inflation data, Canada’s employment report is likely to gather extra attention as well.

Greenback Gains Against Most Majors, Safe Havens Resist

The dollar traded higher against all but two of the other G10 currencies on Thursday. It gained the most against NOK, NZD and AUD in that order, while it traded virtually unchanged against the safe havens CHF and JPY.

The pattern suggests a somewhat risk-averse market environment, with the commodity-linked currencies AUD and NZD among the main losers and the safe havens CHF and JPY resisting the greenback’s strength. Indeed, equity markets support the notion as well. The S&P 500 and Dow Jones ended their trading slightly negative, while most Asian indices are in the red, with Japan’s Nikkei and China’s Shanghai Composite down 1.25% and 0.30% respectively.

In our view, the tit-for-tat tariffs between the US and China, as well as geopolitical tensions between the US and other countries, like Russia and Turkey, may be the reason behind the investors’ fragile sentiment. On Wednesday, China said that it will impose tariffs of 25% on USD 16bn worth of US imports, a retaliation to the US announcement on Tuesday that it will proceed with similar measures on the 23rd of August.

As for Russia and Turkey, on Wednesday, the US announced a fresh round of sanctions over Russia, a move aimed to punish the nation for a nerve-agent attack in the UK, while yesterday, Turkish and US officials failed to find common ground with regards to a diplomatic rift over the imprisonment of an American pastor in Turkey. The news sent the Russian ruble and the Turkish lira plummeting, with the latter sinking to a fresh all-time low against its US counterpart, also weighed by concerns about President Erdogan’s influence over monetary policy.

Back to the greenback, attention for USD traders today is likely to fall on the US CPI data for July. Expectations are for the headline rate to have ticked up to +3.0% yoy from +2.9%, while the core rate is anticipated to have remained unchanged at +2.3% yoy. That said, bearing in mind that yesterday’s data showed that both the headline and core PPIs for the month slowed somewhat, we view the risks surrounding the forecasts as tilted slightly to the downside.

However, even if the CPIs slow somewhat, as long as they remain above the Fed’s 2% objective, we don’t expect something like that to change market expectations much with regards to the Fed’s future plans. At last week’s gathering, the FOMC left interest rates unchanged but kept the door open for two more rate hikes by the end of the year. According to the Fed funds futures, the market is almost certain that the next rate increase to occur in September, while there is a 65% chance for another one to come in December.

USD/JPY – Technical Outlook

The yen continues to strengthen against the US dollar, as geopolitical tensions resume. On Wednesday, USD/JPY broke its short-term upside support line, taken from the low of the 29th of May, this way showing that the pair is clearing its way for some more downside. If this “risk off” sentiment continues, then we could start aiming for lower levels.

The first potential area of support we are targeting is the 110.60 level, marked by the low of the 26th of July. If this area is not able to withhold the rate from dropping further, this could open the way to the next potential support zone at 110.30, which was the low of the 5th of July. Certainly, we could see maybe a few bulls, who could try to jump into the pair and lift, but if they fail to do that, a break below that support zone could set the stage for further declines. The next potential strong obstacle on the bears’ way could be seen around the 109.70 hurdle, marked near the low of the 27th June. Slightly below that lies another good potential area, where the rate could get held from dropping, the 109.35 barrier. This played out as strong support on the 25th and 26th of June, from which USD/JPY moved higher.

Alternatively, a move back up and a close above the aforementioned upside support line could interest the bulls in getting in and to try to lift USD/JPY higher towards the 111.35 zone, marked by the high of the 6th of August. If the zone is not able to resist the rate acceleration, then a break could open the way to the 112.15 barrier, marked by the peak of the 1st of August.

![]()

CAD Traders Lock Gaze on Canada’s Employment Data

The Canadian dollar slid only slightly against its neighboring US dollar, perhaps as positive NAFTA headlines kept CAD’s losses in check. Yesterday, Mexico’s economy minister said that his nation and the US are getting close to agree over auto manufacturing, which could allow Canada to join the talks as early as next week.

As for today, CAD traders are likely to turn their gaze to Canada’s employment report for July. Expectations are for the unemployment rate to have ticked down to 5.9% from 6.0% in June, while the net change in employment is forecast to have declined to 17.5k from 31.8k. Following the acceleration in May’s GDP and the rise in the headline inflation rate for June, as well as yesterday’s positive NAFTA headlines, a decent employment report may increase further market participants’ confidence over the prospect of another BoC rate hike by year end.

GBP/CAD – Technical Outlook

GBP/CAD continues to trade below its short-term downside resistance line, taken from the peak of the 22nd of June. Given that the British pound continues to get hit by sellers, there is a big chance to see this pair drifting lower again. That said, before GBP/CAD could makes its way lower again, the pair could experience a bit of correction back up, where the bears could take advantage again of the higher levels.

For now, we will aim for the downside and if the recently-found strong support level at 1.6720 is broker, this could open the way to further declines. The next potential support area that could fall on our radar is the 1.6585 obstacle, marked by the low of the 13th of November 2017. If this area is not able to withhold the rate from dropping further, this could open the path towards the 1.6385 hurdle, which was the low that was seen on the 20th of October last year.

But let’s not exclude the possibility of a good correction to the upside, before GBP/CAD could make its way back down. Certainly, there are some strong resistance levels to keep an eye on, where the pair could get held. The first one to watch could be the 1.6825 zone, which was yesterday’s peak. Above that, the next resistance to keep an eye on is the 1.6925 obstacle, which if broken, could set the stage for a test of the 1.7025 hurdle, marked by the low of the 1st of August, which also coincides with the aforementioned downside resistance line.

For us to start considering higher levels, we would need to see a break above the previously mentioned downside resistance line. This way we could start considering resistance levels like the 1.7100, which was near the high of the 2nd of August. Above that sits the next potential area of resistance at the 1.7175 barrier, marked by the high of the 31st of July.

![]()

As for the Rest of Today’s Events

During the European morning, Norway’s inflation accelerated in both headline and core terms. The headline rate rose to +3.0% yoy from 2.6%, while the core one increased to +1.4% from +1.1%. At its latest meeting, the Norges Bank decided to keep interest rates unchanged and noted that “the key policy rate will most likely be raised in September 2018”, Thus, today’s data support the Bank’s view. The next Norges Bank meeting is scheduled for the 16th of August, were we expect the Bank to maintain the view that rates are likely to be raised in September.

We get inflation data from Sweden as well. The CPI rate is expected to have remained unchanged at +2.1% yoy, while the CPIF rate is anticipated to have risen at 2.3% yoy. At its latest meeting, the Riksbank kept interest rates untouched and maintained the view that slow repo rate rises will be initiated towards the end of the year. However, apart from the usual dissenter, Deputy Governor Ohlsson, we had another member with reservations. Deputy Governor Floden advocated for an initial increase of interest rates by 25bps in September or October. That said though, the June inflation data showed that the excluding energy CPIF decelerated. Thus, even if the headline CPIF rate rises somewhat in July, a decent acceleration in core CPIF is needed before SEK traders start raising bets that the Bank may act sooner than previously thought.

From the UK, we get the first estimate of GDP for Q2, as well as industrial and manufacturing production data for June. The first GDP estimate is expected to show that the economy expanded +0.4% in Q2 from +0.2% in Q1, in line with the BoE’s view, as well as the NIESR GDP Estimate model. Industrial production is anticipated to have rebounded to +0.4% mom in June after falling 0.4 in May, while manufacturing production is expected to have slowed somewhat, to +0.3% mom from +0.4%. The key message we got from the latest BoE meeting is that officials are probably done hiking for this year. Thus, if the forecasts are met, we doubt that this data set will alter investors’ opinion around the BoE’s future plans. The UK trade balance for June is also coming out.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.