Risk sentiment improved somewhat yesterday, with EU and US indices ending their sessions in positive territory. However, this was proven temporary. After the US close, equity futures turned back down, something that rolled over into Asia. The ECB made no changes to its policy and guidance, with President Draghi repeating that the risks to euro area’s outlook remain broadly balanced, despite the latest softness in economic data.

Investors’ Morale Stays Fragile, ECB Still Sees Balanced Risks

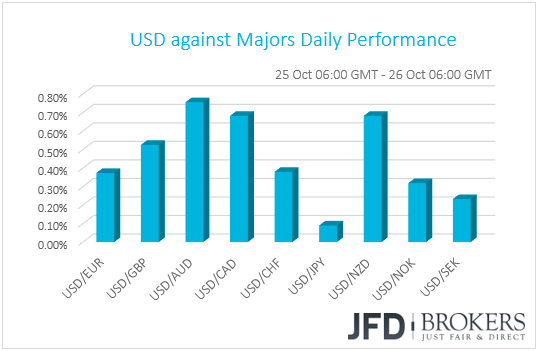

The dollar traded higher against all the other G10 currencies yesterday. The currencies that underperformed the most were the commodity-linked AUD, CAD and NZD, while the safe-haven JPY was the only one which managed to resist the greenback’s strength.

Even though major EU and US equity indices ended their sessions in positive territory, rebounding after Wednesday’s tumble, the FX-performance pattern suggests that the improvement in risk sentiment was just temporary. This is also evident by the Asian markets, which tumbled overnight. Although Wall Street was helped by positive earnings from Microsoft, after the closing bell, disappointing results by Amazon and Alphabet weighted on investors’ morale, with US equity futures turning back down, something that rolled over into Asia. As we noted yesterday, uncertainty over the outlook for US corporate profits is the latest piece added to a blend of persisting risks, including the Italian budget, Brexit, as well as fears over global trade and economic growth.

The Norwegian Krone, although it ended the day lower against its US counterpart, it barely reacted to the Norges Bank decision. The Bank repeated that the key policy rate would most likely be increased further in 2019 Q1, and noted that, since the previous meeting, the balance of risks does not appear to have changed substantially.

A few hours after the Norges Bank decision, the ECB kept its policy unchanged as was widely expected, while the accompanying statement contained no surprises. The Bank reiterated its view that asset purchases are likely to end in December but did not confirm it. It kept the decision subject to incoming data confirming the medium-term inflation outlook.

The lack of any new information in the statement kept the euro untouched at the time of the release, with market participants staying on the edge of their seats in anticipation of President Draghi’s press conference. Despite the softness seen in recent data, at the conference, the President repeated that the risks surrounding Eurozone’s economic outlook remain broadly balanced and that the underlying strength of the economy continues to support the Council’s confidence that the convergence of inflation towards the Bank’s target will be maintained.

When asked over the outlook assessment, the President noted that officials acknowledged the somewhat weaker momentum but pointed out that even though most survey indicators have eased, they remain well above historical averages. “It’s simply that we're having growth returning to potential after 2017, where it was clearly above potential”, the President added. With regards to inflation, he said that the Governing Council does not see much of a change. He noted that negotiated wages keep on going up, and the increases are going to stay. “We have no sense that we should doubt our confidence that inflation is gradually converging to our aim”, he added. With regards to Italy, Draghi made it clear that the ECB will not step in to help the nation, saying “To finance deficits is not part of our mandate. Our mandate is price stability”. That said, he expressed confidence that an agreement between the Italian government and the EU Commission will be eventually found.

The euro edged higher as Draghi downplayed the recent softness in economic data but hit resistance slightly above 1.1430 against its US counterpart, and in the aftermath of the conference it tumbled. Yesterday we noted that, even if Draghi was to maintain its optimistic stance, something he did, any gains in the euro are likely to stay capped. Uncertainty surrounding the Italian budget has been the main catalyst behind the euro’s latest downtrend and the matter is far from resolved. Thus, we remain somewhat bearish on EUR/USD, but not so much on EUR/GBP. The pound is also subject to political uncertainty, with PM Theresa May stuck between a rock and a hard place, just 5 months ahead of the official Brexit date. Although May received a show of support from her parliamentary party on Wednesday, yesterday’s tumble in the pound suggests that investors are far from convinced that a Brexit deal can be struck soon.

Nikkei 225 Cash Index – Technical Outlook

As we all know, the equity market is not the place to be right now, as we are seeing a huge slump in the global indices. Nikkei 225 joins that team of the unfortunate ones and could be heading initially towards the lowest point of this year, which was hit in March. In addition to all this, the index broke through its long-term upwards moving support line this week, which clears the path towards much lower levels. For now, the near-term outlook does not look promising and we could see a further slide lower.

A drop below the 20920 level, which was near yesterday’s low and also marks the low of the 2nd of April, could open the way for lower levels like 20665, which acted as a strong support on the 27th and 28th of March. If the bear-pressure remains strong, we could see the Japanese index falling even further and potentially testing the 20286 barrier, marked near the lowest point of this year.

Alternatively, if Nikkei 225 breaks back above the aforementioned long-term upside support line, this could be a positive sign for the buyers. The only issue here is the steep tentative short-term downside resistance line drawn from the low of the 4th of October. If the index continues traveling higher and moves above, not only that downside line, but also above the 22160 zone, marked by the lowest point of September, then we could get more comfortable with the upside scenario. We could then aim for test of the 22690 area, marked by the Monday’s high. A further acceleration of the price could lead towards the strong resistance area between the 22945 and 23020 level, which acted as both good resistance and support throughout this year.

![]()

We can clearly see on the 4-hour chart that yesterday, EUR/GBP managed to rush though its short-term downside resistance line drawn from the 28th of August. The break also placed the pair above key resistance level at 0.8857, which was also seen acting as strong support during August and September. Since the 10th of October, EUR/GBP keeps making higher lows, which combined with the yesterday’s break of the above-mentioned downside line, turns the near-term outlook into a more positive one for now.

Another good push higher, but this time through the 0.8885 zone, which was near yesterday’s high, could open the path towards the 0.8915 level. This area kept the rate down on the 28th of September and also on the 1st and the 3rd of October. But if the bulls remain strong, we could see the pair getting lifted even higher, where the next potential area of resistance could be at 0.8937, marked by the high of the 27th of September.

On the downside, because EUR/GBP is still close to the aforementioned downside resistance line that got broken, we will slightly remain cautious, as a sharp drop back down below it, could make us start worrying about the upside. A better confirmation that the bulls are abandoning the field could be a drop below the 0.8825 line, which acted as a good support on Tuesday and Wednesday, and also was seen as resistance last week, on Monday. If such a scenario happens, we would expect the pair to travel down towards the 0.8775 hurdle, a break of which could lead to a test of the 0.8752 barrier, marked by the 16th of October.

![]()

As for Today’s Events

We get the 1st estimate of the US GDP for Q3. Expectations are for the US economy to have expanded 3.3% qoq SAAR, a slowdown from the stellar 4.2% qoq growth rate in Q2, which was the fastest pace in nearly four years. However, although a slowdown, this would mark the strongest back-to-back quarters since 2014, with strong consumption and solid business investment being in the driver’s seat. The Atlanta Fed GDPNow model suggests that the economy expanded 3.6%, supporting the case for another quarter of solid growth, but the New York Fed Nowcast model points to a 2.2% rate of expansion. Thus, it’s hard to say to which direction the risks of the forecast are tilted to. We also get the final UoM consumer sentiment index for October, alongside the final UoM 1-year and 5-year inflation expectations.

As for the speakers, ECB President Mario Draghi will speak again, while a few minutes later we will hear from ECB Executive Board member Benoit Coeuré.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.