Wall Street’s main indices slid yesterday as Senate Majority Leader put off a vote on Trump’s demand for USD 2000 coronavirus relief checks to millions of Americans. However, investors may have had second thoughts during the Asian session, as the delay means that the Republican-controlled Senate is not immediately considering blocking the plan.

Asian Stocks Gain on Hopes of Trump’s Plan Passing in Senate

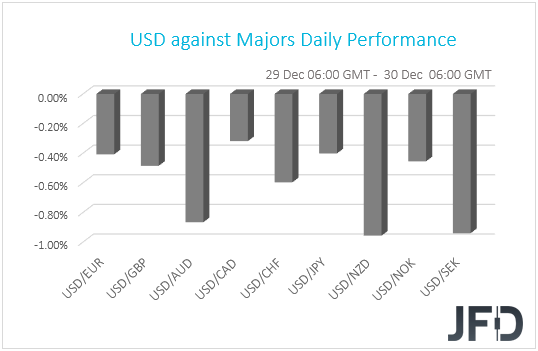

The US dollar tumbled against all the other G10 currencies on Tuesday and during the Asian session Wednesday. It lost the most ground versus NZD, SEK, and AUD in that order, while it underperformed the least against CAD.

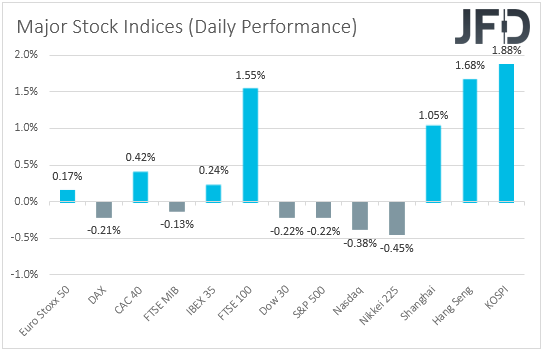

The weakening of the safe-haven dollar, combined with the strengthening of the risk-linked currencies Kiwi and Aussie, suggests that markets traded in a risk-on fashion yesterday and today in Asia. That said, looking at the performance in the equity world, we see that EU indices traded mixed within a ±0.50% range, with the only exception being UK’s FTSE 100, which jumped 1.55% in its first day of trading after the sealing of a Brexit trade accord last Thursday. In the US, all three of Wall Street’s main indices slid on average 0.27% each, but investors’ appetite improved notably during the Asian trading today. Although Japan’s Nikkei 225 retreated 0.45%, China’s Shanghai Composite, Hong Kong’s Hang Seng, and South Korea’s KOSPI gained 1.05%, 1.68% and 1.88% respectively.

On Monday, the US House of Representatives voted to meet President Trump’s demand for USD 2000 coronavirus relief checks, instead of the initial USD 600 proposal, sending the measure onto the Senate, which convened yesterday. That said, the chamber did not vote on the matter as Majority Leader Mitch McConnell put off a vote, saying that they would address the call during the week. The delay may have been the reason why market participants decided to lock some profits on US equities, especially after all three of Wall Street’s main indices hit new all-time highs on Monday. However, they may have had second thoughts during the Asian session, as the delay means that the Republican-controlled Senate is not immediately considering blocking the plan. The proposal needs 60 votes to pass, which means that 12 Republicans would have to back it. Headlines suggest that at least five of them have so far voiced support, which means that there are decent chances for approval today or tomorrow. Maybe that’s why Asian indices traded higher.

If the Senate votes in favor of the plan, then equities could drift higher, while the opposite may be true in case of a rejection. However, we don’t expect a rejection-related retreat to last for long. We would treat it as a corrective move in the broader upside path. In other words, it may be a fresh opportunity for investors to buy equities at a lower price. Even with the USD 600 checks, the government’s overall spending plan has been signed into law by President Trump on Sunday. Thus, we stick to our guns that the covid vaccinations, the fiscal stimulus in the US, the Brexit accord, and a Biden Presidency, may continue benefiting risk assets, while safe havens could stay under selling interest. This means that apart from equities, we could see decent gains in currency pairs consisting of a risk-linked currency and a safe haven, the likes of AUD/JPY, AUD/USD, NZD/JPY, and NZD/USD.

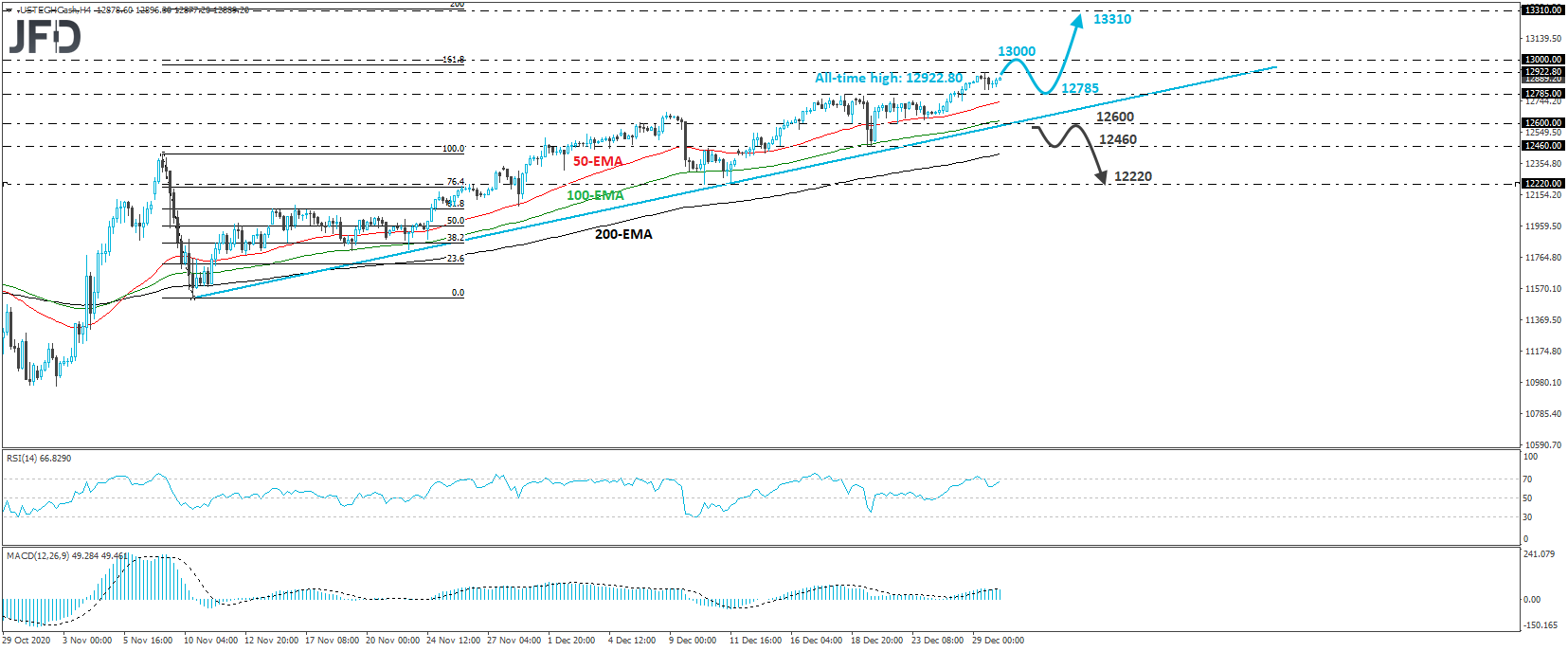

NASDAQ 100 – Technical Outlook

The Nasdaq 100 cash index traded lower after it hit a new record high at 12922.80. That said, the index rebounded somewhat during the Asian trading today. Overall, the index continues to print higher highs and higher low above the upside support line drawn from the low of November 10th, and thus, we would consider the near-term outlook to be positive.

A clear break above the all-time high of 12922.80 may tempt the bulls to challenge the psychological zone of 13000. They may decide to take a break after hitting that zone, thereby allowing the index to correct lower. However, as long as it stays above the pre-mentioned upside line, we would see decent chances for a rebound and another leg north, perhaps above 13000. This may see scope for larger upside extensions, perhaps towards the 13310 territory, which coincides with the 200% extension level of the November 9th and 10th setback.

In order to abandon the bullish case, at least in the short run, we would like to see Nasdaq 100 falling below the upside line, as well as below the 12600 barrier, defined as a support by the low of December 22nd. Such a move may initially aim for the low of the day before, at 12460, the break of which may allow the bears to push the battle towards the low of December 10th, at 12220.

NZD/USD – Technical Outlook

NZD/USD traded higher yesterday, and continued to do so today in Asia, breaking above the peak of December 17th, at 0.7172, thereby confirming a forthcoming higher high. In the short run, the pair has been supported by the 0.7010 key zone since November 27th, while since December 21st, it’s been respecting a new-born upside line. Therefore, we would see decent chances for this exchange rate to continue drifting north.

At the time of writing, NZD/USD looks to be headed towards the 0.7200 zone, marked as resistance by the inside swing low of April 20th, 2018, the break of which may encourage the bulls to climb towards the inside swing low of April 6th, 2018, at 0.7240. Another break, above 0.7240, may carry larger bullish implications, perhaps paving the way towards the inside swing low of April 18th, 2018, at 0.7300.

On the downside, a dip below 0.7010 may allow for a larger correction lower. This will also take the rate below the 200-EMA on the 4-hour chart and the bears may pull the trigger for the 0.6945 level, marked by an intraday low formed on November 24th. If that barrier is broken as well, then we may experience extensions towards the low of the day before, at around 0.6896.

As for Today’s Events

Besides any potential headlines surrounding the Senate vote, the only data releases to pay attention to are the US pending home sales for November, and the EIA (Energy Information Administration) report on crude oil inventories for last week. Pending home sales are expected to have rebounded 0.2% mom, after tumbling 1.1% in October, while the EIA is expected to report a 2.583mn inventory fall after a 0.562mn slide the week before. That said, bearing in mind that, yesterday, the API (American Petroleum Institute) revealed a 4.785mn tumble, we would consider the risks surrounding the EIA forecast as tilted to the downside. A negative surprise could prove positive for oil prices.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72.57% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2020 JFD Group Ltd.