This week, the spotlight is likely to fall on the US mid-term elections. Polls suggest that there is an increasing likelihood for Democrats to take control of the House, but the chances of gaining majority in the Senate are less. We also have three central banks deciding on interest rates: the FOMC, the RBA and the RBNZ. That said, all three Banks are expected to keep interest rates untouched.

On Monday, during the European morning, the UK services PMI for October is due to be released and expectations are for the index to have declined for the second consecutive month. Specifically, the index is forecast to have declined to 53.3 from 53.9.

We get October PMIs from the US as well. The final Markit composite and services PMIs are coming out, as well as the ISM non-manufacturing index for the month. The final Markit prints are expected to confirm their preliminary estimates, while the ISM index is anticipated to have declined to 64.5 from 65.2.

On Tuesday, all lights are likely to fall on the US mid-term elections. All 435 seats in the House will be contested, as well as 35 of the 100 seats in the Senate. Currently, the Republicans hold the majority in both chambers of Congress and the big question is whether they will maintain full control. Polls suggest that there is an increasing likelihood for Democrats to take charge in the House, but the chances of gaining majority in the Senate are less.

So, what happens in case Democrats take the House and what does this means for the markets? With a split Congress, President Trump may find it hard to proceed with his political agenda, which may include further tax reforms. What’s more, a House led by Democrats may open the door for more investigations over Trump and perhaps lead to attempts to impeach him. However, we see the removal of the President as an unlikely outcome. A Democratic-led House could easily vote to impeach him by a simple majority, but for the President to be removed, it would require a two-third majority in the Senate.

With regards to market reactions, this outcome could spook the stock market and perhaps hurt the dollar as it could lessen the chances for more tax cuts and further deregulation. Remember that US equity markets surged following Trump’s election on speculation that his agenda will spur growth and help the economy. Political instability in the form of investigations and/or impeachment attempts could also weigh in the US markets.

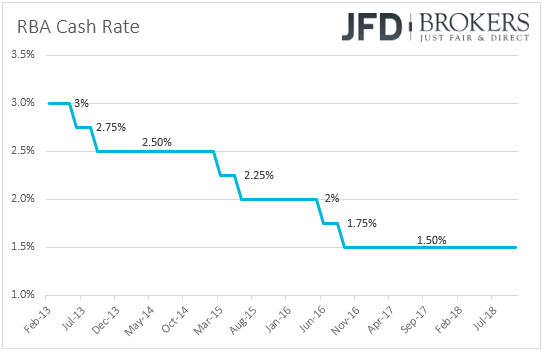

As for the rest of Tuesday’s events, during the Asian morning, the Reserve Bank of Australia decides on monetary policy, but once again we don’t expect any major surprises. The Bank has been stubbornly keeping interest rates at +1.50% since August 2016, and according to its latest Statement on Monetary Policy, the cash rate is expected to increase around the end of next year.

Last week, Australia’s inflation data showed that the headline CPI rate slid to +1.9% in Q3 from +2.1% in Q2, while the trimmed mean rate ticked down to +1.8% from +1.9%. Even though both rates are still slightly above the Bank’s latest forecasts for the second half of 2018, they remain below the 2-3% target range, suggesting no imminent change in the thinking of RBA officials. We believe that market participants may prefer to wait for the new quarterly Statement on Monetary policy, due out on Friday, which will include the Bank’s updated economic projections.

During the European day, we get the final services and composite PMIs from the nations of which we had the manufacturing data on Friday. As usual, the bloc’s final prints are expected to confirm their preliminary estimates. Eurozone’s PPI data and Germany’s factory orders, both for September are also coming out. Eurozone’s PPI rate is forecast to have remained unchanged at +4.2% yoy, while German factory orders are anticipated to have declined 0.6%mom, after rising 2.0% in August.

Later in the day, the US JOLTs job openings for September are due out, as well as Canada’s building permits for the same month.

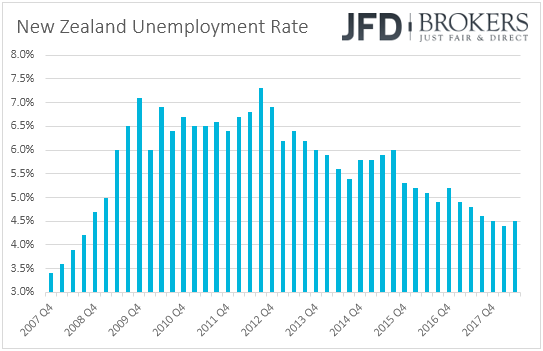

On Wednesday, in the early Asian day, New Zealand’s employment data for Q3 are scheduled to be released. The unemployment rate is expected to have remained unchanged at 4.5%, just a tick above 4.4%, which was seen in Q1 and is the lowest since Q3 2008. The net change in employment is expected to have risen at the same pace as in Q2. As for the labor costs index, it is expected to have slowed to +1.9% yoy from +2.1%. The nation’s 2-year inflation expectations for the quarter are also due to be released, but no forecast is currently available.

During the European morning, Eurozone’s retail sales for September are expected to have rebounded 0.1% mom after sliding 0.2% in August. This is likely to bring the yoy rate down to +0.8% from +1.8%. Germany’s industrial production is also due to be released. Later in the day, we get Canada’s Ivey PMI for October. The index is anticipated to have risen somewhat, to 50.9 from 50.4.

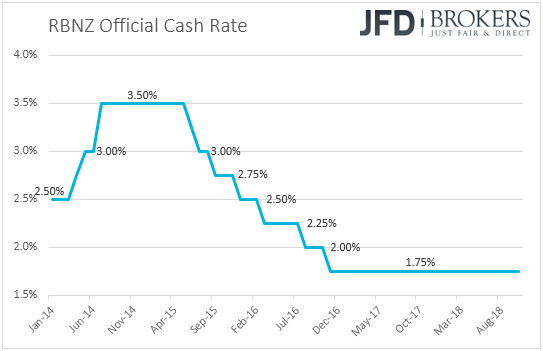

On Thursday, two more central banks decide on monetary policy. During the early Asian morning, we have the RBNZ, while later, in the US session, it’s the turn of the FOMC.

Kicking off with the RBNZ, at their latest meeting, policymakers kept interest rates unchanged at +1.75% as was widely anticipated, while the statement contained little new information. The Bank repeated that interest rates are likely to remain at this level through 2019 and into 2020, and that the next direction could be up or down. With regards to the economy, officials acknowledged that growth was stronger than anticipated in Q2, but they noted that downside risks remain and that their projection for the economy has little changed.

Latest CPI data showed that inflation accelerated to +0.9% qoq in Q3 from 0.4% in Q2, something that pushed the yoy rate up to +1.9% from +1.5%. This is well above the Bank’s own projections of 1.4% in the latest quarterly Monetary Policy Statement, and near the midpoint of its 1-3% target range. Although the Bank is not expected to proceed with any policy changes at this meeting, it would be interesting to see whether it will revise up its inflation projections in its new quarterly report, and whether officials will decide to bring forth the timing of when they expect interest rates to start rising. According to the August forecasts, interest rates are expected to start rising in the last quarter of 2020.

Passing the ball to the FOMC, this would be one of the “smaller” meetings that are not accompanied by new economic projections, neither a press conference by Fed Chair Jerome Powell. Expectations are for the Committee to keep interest rates untouched within the 2.00-2.25% range, with the market assigning a near 95% probability for such an outcome. Thus, if this is the case, market participants are likely to quickly turn their attention to the accompanying statement.

The key takeaway we got from the latest FOMC meeting, as well as by the minutes of that gathering, is that Fed officials are willing to continue raising rates mainly guided by economic data, instead of how close to their neutral level interest rates are. What’s more, a number of policymakers believe that it would be necessary to raise rates above neutral for some time.

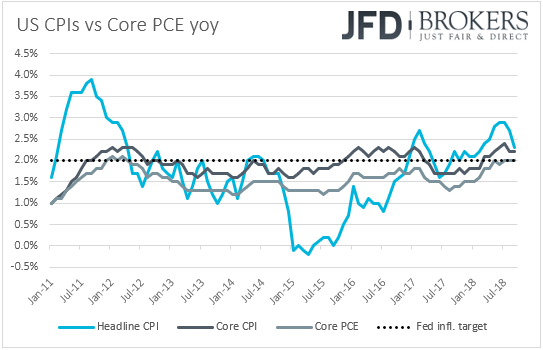

After that gathering, data showed that the headline CPI slowed to +2.3% yoy in September from +2.7%, but the core CPI rate remained unchanged at +2.2% yoy. The yearly core PCE rate for the month, the Fed’s favorite inflation measure, also held steady, at +2.0%. What’s more, although the economy slowed in Q3, according to preliminary data, it still grew at a strong pace (+3.5% qoq SAAR). Last but not least, Friday’s employment figures showed stellar job gains and with wage growth hitting its highest rate since 2009. In our view, the data keep the Fed well on track for keep raising rates and thus, we don’t expect to get any surprises from this meeting’s statement. We expect officials to repeat that the labor market has continued to strengthen, that economic activity has been rising at a strong rate, that inflation remains near 2%, and that they expect further gradual increases in interest rates.

As for the rest of Thursday releases, during the Asian session, we get the BoJ’s summary of opinions from its latest gathering but given that the meeting resulted in no fireworks, we don’t expect the summary to do so. In China, the nation’s trade surplus is forecast to have increased to USD 36.3bn in October, from 31.7bn in September. Later, in the European morning, we get trade data from Germany as well. The nation’s surplus is expected to have slightly narrowed. Canada’s housing starts for October are also due to be released.

Finally, on Friday, during the Asian morning, we get China’s CPI and PPI for October. The CPI rate is anticipated to have stayed unchanged at +2.5% yoy, while the PPI one is expected to have slid to +3.4% yoy from +3.6%. Australia’s home loans for September are also coming out.

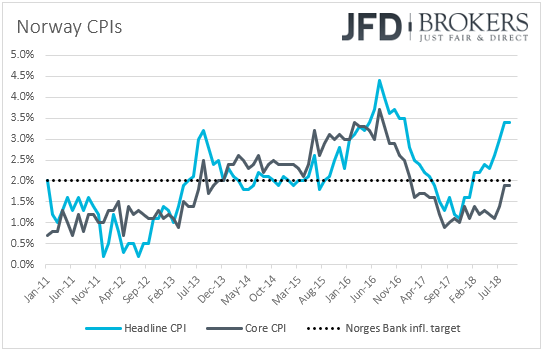

During the European day, Norway’s inflation data for October are due to be released. The headline rate is forecast to have held steady at +3.4% yoy , but the core CPI rate is expected to have slid to +1.8% from +1.9%. At its previous meeting, the Norges Bank kept its key policy rate unchanged at +0.75% and repeated that it would most likely be increased further in 2019 Q1. It also noted that since the previous meeting, the balance of risks surrounding the economy did not appear to have changed substantially. The next meeting is scheduled for the 13th of December and up until then, we have another set of inflation data to be released. Therefore, we don’t expect a tick down in the core CPI to alter expectations around the Bank’s future plans. We believe that a more severe slowdown is needed for market participants to start examining the likelihood of the Bank pushing back its hike timing.

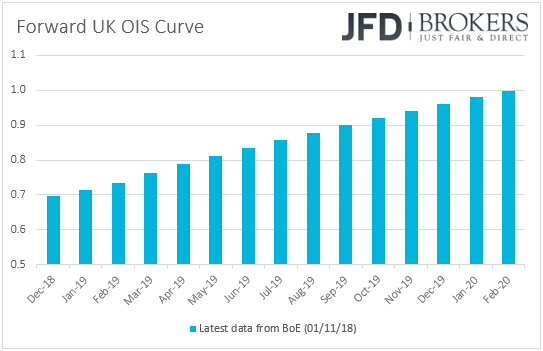

From the UK, we get the 1st estimate of Q3 GDP. The forecast suggests that the UK economy expanded 0.6% qoq in the three months to September, an acceleration from +0.4% in Q2. This is likely to drive the yoy rate up to +1.5% from +1.2%, which would be in line with the BoE’s forecasts in last week’s Inflation Report. In our view, this data set is unlikely to change BoE’s plans. It could bring forth market expectations with regards to the next rate increase, but not much. Market participants still believe that any policy move is more likely to come after the official Brexit date, which is on the 29th of March 2019. According to the BoE’s OIS forward curve, the market is not even fully pricing in a hike for next year. Specifically, following last week’s BoE policy meeting, the market is fully pricing in the next rate increase to come in February 2020. Thus, we believe that the data can only bring that timing back in the last three months of 2019. The UK industrial and manufacturing production data, as well as the nation’s trade balance, all for September, are coming out as well.

In the US, the PPIs for October are coming out. The headline rate is expected to have remained unchanged at +2.6% yoy, while the core rate is forecast to have declined to +2.3% yoy from +2.5%. This could raise speculation of a slowdown in the core CPI rate as well. However, even if the core CPI slows somewhat, we don’t expect something like that to prevent Fed officials from pushing the hiking button at the December gathering. The market already sees a 72% for such an action and we think that a notable tumble below 2% may be needed to force them scale that back. The preliminary UoM consumer sentiment index for November is also coming out, alongside the preliminary UoM 1- and 5-year inflation expectations.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.