Equity markets collapsed yesterday in in what it seems as a Déjà vu of what happened in February. Once again, market chatter suggests that the catalyst behind the bloodbath may have been the steep rally in US Treasury yields. The pound continued to gain yesterday following comments by EU Chief Negotiator Michel Barnier.

Wall Street Tumbles and Triggers a Sense of Déjà vu

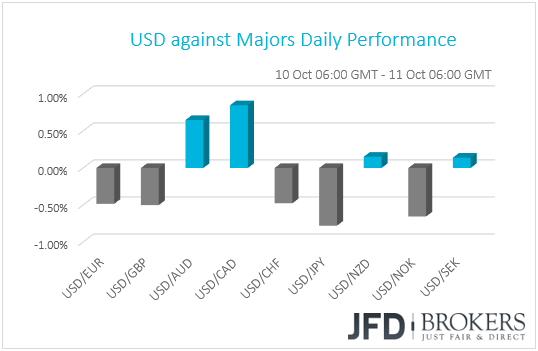

The dollar traded mixed against the other G10 currencies yesterday. The commodity-linked currencies CAD, AUD and NZD stayed on the back foot, while the safe-haven JPY was the main winner, as US equity plummeted in what it seems as a Déjà vu of what happened in February.

The Dow Jones and the S&P 500 experienced their worst day since the 8th of February, falling 3.11% and 3.29% respectively, while Nasdaq plummeted 4.08%, the most since Brexit. Once again, market chatter suggests that the catalyst behind the bloodbath may have been the steep rally in US Treasury yields, due to concerns of faster than previously anticipated rate increases by the Fed. As we noted several times, higher interest rates mean higher borrowing costs for companies, which could hurt their profitability. Thus, while yields were rising, investors have started abandoning the equity market.

That said, up until Tuesday, market participants exiting equities didn’t seem to be tempted by the more alluring bond market, perhaps keeping their money in cash, something that allowed the 10-year yield to hit a 7-year high of 3.261. This is the level where bonds may have started becoming attractive as 10-year yields ended Tuesday 0.77% down, which means there was some demand for bonds. Perhaps on Wednesday, more investors decided to jump from the equity to the tempting bond market, and thus the dive in stock indices. Indeed, 10-year yields were 1.00% down yesterday, suggesting that more participants decided to rush into bonds.

Even US President Donald Trump blamed the Fed for yesterday’s slump. “I think the Fed has gone crazy” the President said. “Actually, it’s a correction that we’ve been waiting for for a long time, but I really disagree with what the Fed is doing,” he added.

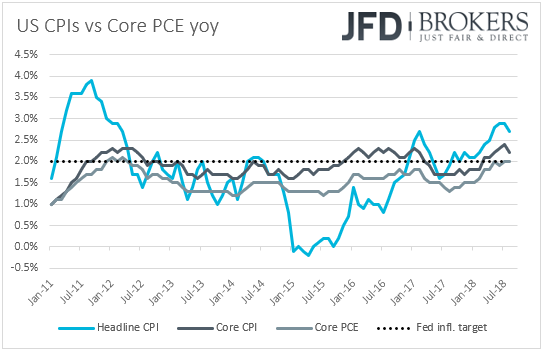

If, indeed, the catalyst behind the equity turbulence was rinsing yields due to expectations for faster Fed hikes, we expect the financial community to lock its gaze on today’s US inflation data for September. Expectations are for the headline CPI to have slowed to +2.4% yoy from +2.7% in August, while the core rate is expected to have ticked up to +2.3% yoy from +2.2%. Yesterday, the headline PPI rate declined to +2.6% yoy from +2.8%, while the core PPI rate rose to +2.5% yoy from 2.3%, supporting the case for a slowing headline CPI rate and accelerating underlying inflation. We believe that most of the attention is likely to fall on the core measure, which strips out the volatile items of food and energy. If the core CPI rate accelerates more than anticipated, this is likely to keep concerns of aggressive Fed hikes elevated and thereby, equity indices could fall further.

Nasdaq 100 Cash – Technical Outlook

Yesterday, Nasdaq 100, together with the other indices, plummeted, repeating the scenario seen in February. During yesterday’s sell-off, the US technology index was the biggest loser, compared to the S&P 500 or the DJIA. The index lost more than 4% on the day and it looks like that the bear-party could not be over yet. From the technical side, Nasdaq 100 slid from near the lower side of the range between the 7385 and 7690 levels, and dropped without giving the bulls even a chance to breathe. Overall, the index is still above this year’s uptrend line taken from the low of the 9th of February, but it looks that the it could soon be heading towards that line for a test. For now, we remain bearish in the short run, but we would expect a bit of correction back to the upside, where the bears could take advantage of the higher price and jump into the action again.

The index eventually hit support slightly below 6930 and rebounded back above that level. Another break below the 6930 support zone, marked by the low of the 28th of June, could open the gate to the next potential area of support at 6855, which acted as both, support on the 18th of May and resistance on the 19th of April. Slightly below lies the abovementioned upside support line that could initially stall the price until the bulls and the bears decide who takes the driver’s seat from there. As mentioned in the first paragraph, there could be a scenario, where the index makes a retracement back up again and then drops back down. A good potential area of resistance could be seen near the 7180 level, marked by the low of the 30th of July.

Alternatively, in order to get comfortable with the upside, we would need to see Nasdaq 100 traveling all the way back above the previously mentioned lower side of the range at 7385. Only then we could try and examine higher levels like 7600, or even the upper bound of the range, which is at 7690, marked by the highs of the 2nd of October and the 4th of September.

![]()

Barnier lifts the Pound, Euro-traders Focus on ECB Minutes

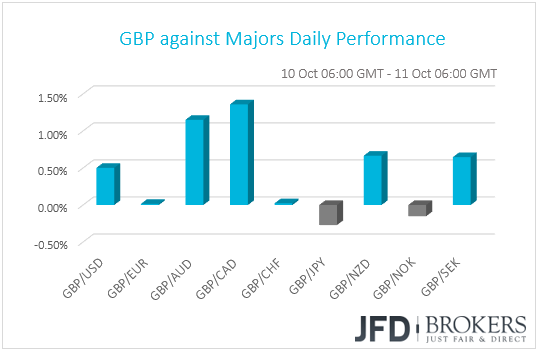

The pound continued to gain against most of its G10 peers yesterday. It lost some ground only against JPY and NOK, while it traded virtually unchanged versus EUR and CHF. The main losers against the British currency were CAD and AUD.

The pound remained well supported as headlines surrounding the UK’s exit from the EU continue to suggest that a deal between the two sides is becoming increasingly more likely. Yesterday, EU Brexit negotiator Michel Barnier said that 80-85% of the withdrawn deal is already agreed and that Irish border checks would be carried out "in the least intrusive way possible." His comments follow a Wall Street Journal Report on Tuesday, saying that the terms of the UK’s exit from the EU could be settled next week, and perhaps as early as Monday, just ahead of the EU summit which is scheduled to begin next Thursday.

As for our view, it remains the same as yesterday. Barring any headlines suggesting otherwise, the pound could continue gaining due to increased optimism that a Brexit deal could be agreed soon. However, as we get closer to next week’s EU summit, we believe that GBP-bulls will start getting more cautious and any further gains may not be as steep as this week.

One of the currencies against which the pound failed to gain and instead traded virtually unchanged was the euro. The euro was also higher against most of the other G10 currencies, perhaps underpinned by optimism for a Brexit deal, as well as by comments from Italy’s finance minister Giovanni Tria, who reiterated that the government will do whatever it takes to regain the confidence of financial markets.

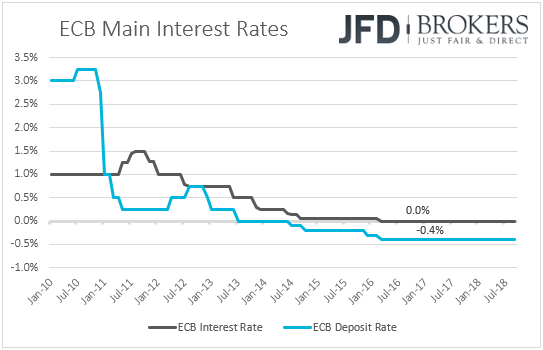

As for today, euro traders are likely to turn their attention to the minutes of the latest ECB policy meeting. At that meeting, the Bank repeated that asset purchases are likely to end in December and maintained the guidance that interest rates are likely to stay at current levels “at least through the summer of 2019”. At the press conference following the decision, despite the downgrade in the Bank’s growth projections, Draghi appeared fairly optimistic, noting that the balance of risks surrounding growth has not changed. What’s more, speaking at the Economic and Monetary Affairs of the European Parliament hearing a few weeks ago, Draghi said that he sees a “relatively vigorous” pickup in underlying inflation as the tightening labor market is resulting accelerating wage growth. Thus, although we don’t expect to get any surprises from the minutes on the guidance front, it will be interesting to see whether other officials, besides Draghi, are upbeat on the Euro-area economic and inflation outlooks.

EUR/GBP – Technical Outlook

The British pound has been outperforming the common currency since the last days of summer and for now, it seems that this could continue being the case in the near future. The pair is trading below its downside resistance line, taken from the peak of the peak of the 28th of August. That said, from a very short-term perspective, we could see some correction back to the upside, as EUR/GBP is quite oversold on the 4-hour chart, but overall, we remain bearish over the longer-term outlook.

After finding good support near the 0.8725 level, EUR/GBP managed to bounce back a little. That’s why we will examine the possibility for the pair to retrace back up to the 0.8775 resistance zone that could hold the rate down. The bears could try to jump in again and take the pair lower. For a more conservative approach of the downside scenario, a good confirmation could be seen on a break of the abovementioned support of 0.8725, which could open the path towards support areas like 0.8695, or even 0.8665, marked by the inside swing high of the 13th of April.

The short-term upside scenario could be, if EUR/GBP decides to continue correcting higher and breaks the 0.8807 level, marked by the peak of the 8th of October. This way, the bulls could try and lift the pair higher towards the next potential area of resistance at 0.8855, which acted as strong support on the 3rd and 1st of October, and also on the 20th of September. If that area is not able to withhold the buying action, EUR/GBP could travel a bit higher. But the upside could be limited due to the previously mentioned short-term downside resistance line, which could hold the rate down.

![]()

As for the Rest of Today’s Events

Besides the US CPIs and the ECB minutes, we also have Sweden’s inflation data for September on today’s agenda. The forecasts suggest the CPI rate rebounded to +2.2% yoy from +2.0% in August, while the CPIF print is expected to have risen to +2.4% yoy from +2.2%. That said, once again, we will pay more attention to the core CPIF inflation metric, which excludes energy.

At its latest policy meeting, the Riksbank kept interest rates on hold and noted that rates will be held unchanged at the October gathering, and then raised either in December or February. However, after that meeting, inflation data showed that the core CPIF rate fell to +1.2% yoy, its lowest since January 2017. Thus, another slowdown in this inflation metric, or even an unchanged rate, could raise concerns that at is upcoming gathering, scheduled for the 23rd of October, the world’s oldest central bank may dismiss the December option and note that rates could be raised at the beginning of next year. We believe that a notable rebound in the core CPIF rate is needed for the Bank to keep the door open for a December hike.

The US initial jobless claims for the week ended on the 5th of October, and the Energy Information Administration (EIA) crude oil inventories are also due to be released.

As for the Asian morning Friday, we get China’s trade data for September. Expectations are for the nation’s trade surplus to have declined to USD 21.0bn from USD 27.9bn in August. Both exports and imports are expected to have slowed to +9.1% yoy and +15.0% yoy from +9.8% and 19.9% respectively.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.