With investors biting their nails due to concerns over whether rising energy prices could result in further acceleration in inflation, the main item on this week’s agenda may be the US CPIs for September. From the UK, we have the jobs and GDP data for August, but we don’t expect a massive market reaction if they come in on the strong side, as participants may have already priced in a hawkish BoE. Australia’s employment report for September is also due to be released.

Monday appears to be a quiet day, with no major events or economic indicators on the financial agenda.

On Tuesday, during the early European session, we get the UK employment data for August. The unemployment rate is expected to have ticked down to 4.5% from 4.6%, while the net change in employment is anticipated to show that the economy has added 243k jobs in the three months to August, compared to 183k in the three months to July. Average weekly earnings, both including and excluding bonuses, are expected to have slowed to 7.0% and 5.9% from 8.3% and 6.8% respectively.

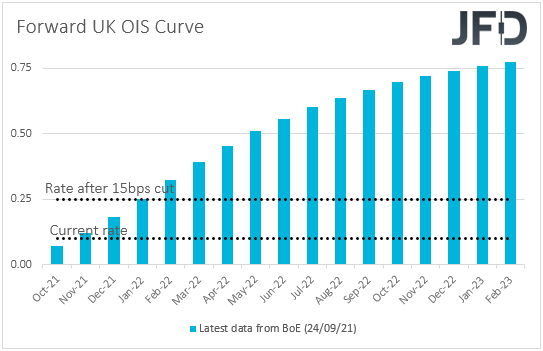

At its latest policy gathering, the BoE appeared more hawkish than expected, encouraging market participants to bring forth their rate hike expectations, with the UK OIS (Overnight Index Swaps) pointing to a 15bps hike to be delivered in January 2022. However, with the latest supply chain problems in the UK, we don’t believe that data concerning the period of August will be able to drive the pound, even if they come out on the strong side, which means greater likelihood for early hikes by the BoE. With the same logic, we don’t expect Wednesday’s GDP data for the month of August to prove a major market mover for the pound either. We believe that, due to the pound’s strengthening correlation with risk sentiment lately, the currency will stay linked to developments surrounding that front rather than expectations around monetary policy. After all, we believe that a hawkish BoE is already priced in, and any pound strength due to increasing bets over a hike, could be limited.

A few hours after the UK employment data, we have the German ZEW survey for October, with both the current conditions and economic sentiment indices expected to have declined slightly, to 29.5 and 24.0 from 31.9 and 26.5. Later, in the US, JOLTs job openings for August are coming out and the forecast points to a small decline.

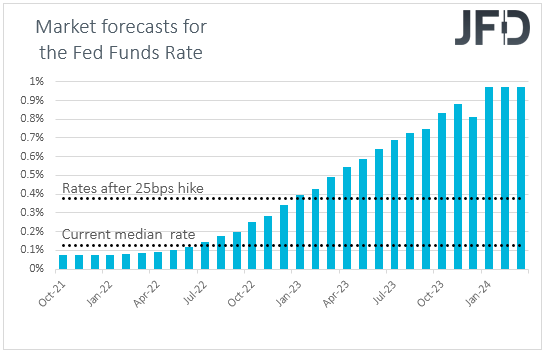

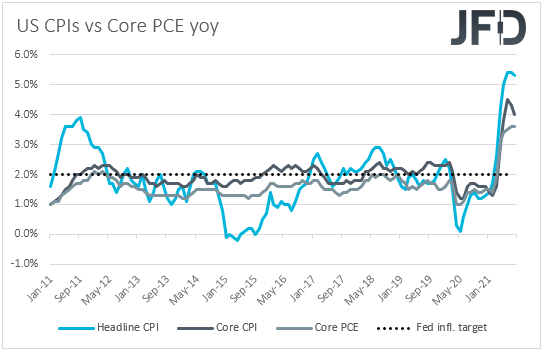

On Wednesday, the main event on the agenda may be the US CPIs for September. Both the headline and core CPI rates are expected to have held steady at 5.3% and 4.0% respectively, well above the Fed’s objective of 2%. Although the US employment report revealed a disappointing number of added jobs during the month of September, market participants maintained their bets with regards to a possible November tapering by the Fed and a rate hike during the first months of 2023. According to the Fed funds futures, a 25bps rate hike is more than fully priced in for January 2023.

At this point, market participants don’t need inflation to accelerate further in order to increase their tightening bets. Even staying unchanged and not pulling back may be enough, as this adds credence to their view that the surge in consumer prices may, eventually, not be as transitory as the Fed has initially expected. We may get more hints and clues as to how likely a November tapering may be, from the minutes of the latest FOMC meeting, which come out later in the day.

As for the rest of Wednesday’s data, during the Asian session, China’s trade balance for September is coming out, with the nation’s surplus anticipated to have declined, while during the early European session, as we already noted, we have the UK monthly GDP for the month of August. Alongside the GDP, we will get the industrial and manufacturing production rates for the month. We get August industrial production data from the Eurozone as well, and Germany’s final CPIs for September.

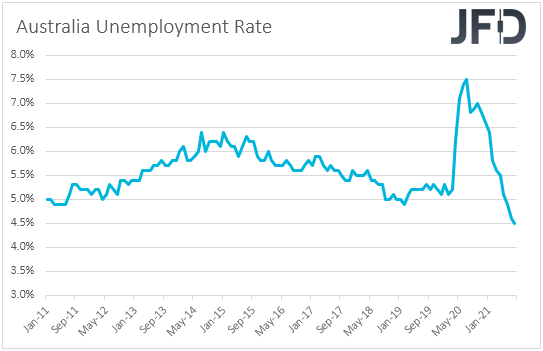

On Thursday, Asian time, Australia’s employment data for September are due to be released. The unemployment rate is expected to have risen to 4.8% from 4.5%, while the net change in employment is anticipated to show that the economy has lost 120k jobs, after losing 146.3k in August.

At last week’s gathering, the RBA kept all its policy settings unchanged with officials repeating that they will continue to purchase government securities at the current pace until at least mid-February and maintaining the view that interest rates are unlikely to rise before 2024. We believe that a soft employment report may add more credence to the RBA’s dovish stance and may push the Aussie somewhat lower.

However, bearing in mind that Aussie traders may have already digested a dovish RBA, we believe that the Aussie’s faith will depend mainly on developments surrounding the broader market sentiment. In the second half of last week, investors’ morale improved as Russia indicated that energy supply to Europe could increase, soothing concerns over the latest supply shortages, as well as after US Senate Democrats and Republicans agreed to raise the nation’s debt ceiling until December. All these developments may allow market participants to increase their risk exposure for a while more, which could prove positive for risk-linked currencies like the Aussie. However, we are reluctant to trust a long-lasting advance.

In the energy saga, we only have talks and no concrete action yet and thus, with energy prices staying in steep uptrends, we believe that market participants may stay concerned over high energy prices translating into further acceleration in inflation. What’s more, in the US, the probability of a catastrophic government shutdown is not zero. Officials just extended the funding until December. A fresh standoff between Democrats and Republicans suggesting a shutdown in a couple of months, could weigh further on investors’ morale. Therefore, we believe that any recovery in equities is likely to prove to be temporary and another downside correction may be looming. At the same time, we expect the US dollar to resume its latest uptrend, and the risk-linked currencies to come under renewed selling interest.

As for the rest of Thursday’s events, during the Asian session, we have China’s CPI and PPI for September, both the yoy rates of which are expected to have increased somewhat. Japan’s preliminary industrial production for August is also coming out but no forecast is available. Later in the day, apart from the US initial jobless claims, which we get every Thursday, we also have the US PPIs for September, with both the headline and core yoy rates expected to have risen further, something that could intensify concerns over further acceleration in consumer prices in the months to come, and thereby increase speculation over faster tightening by the Fed.

Finally, on Friday, the main items on the agenda are the US retail sales for September, the New York Empire State manufacturing index for October, and the preliminary UoM consumer sentiment index for the same month. Headline sales are expected to have slid 0.2% mom, after rising 0.7% in August, while the core rate is anticipated to have declined to +0.5% from +1.8%. The Empire State index is forecast to have declined to 27.00 from 34.30, while the UoM index is expected to have risen to 73.8 from 72.8.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 73.90% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2021 JFD Group Ltd.