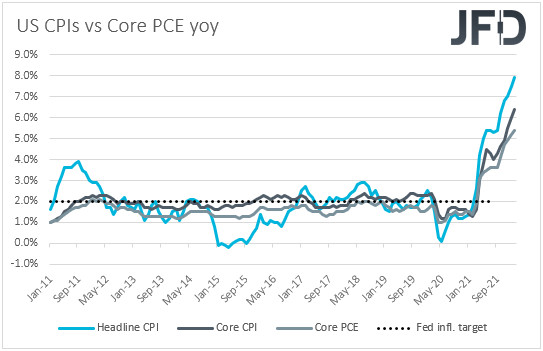

Today, the spotlight is likely to fall on the US CPIs for March, with both the headline and core rates expected to have continued drifting north, something that could add more credence to the view that the Fed may need to proceed with larger than quarter-point rate increments in the months to come. Tonight, during the early Asian session, the RBNZ decides on interest rates and although a hike is a done deal, the question is whether it will be of 25bps or 50.

Will The CPIs Cement the Case for Double Hikes by the Fed?

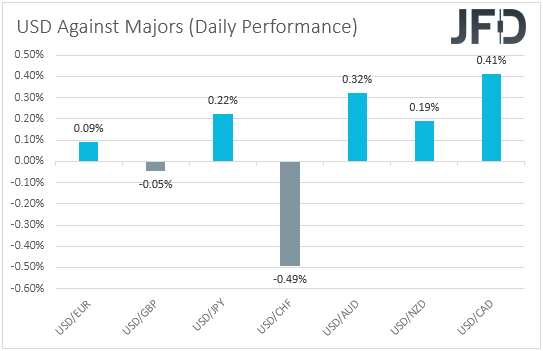

The US dollar traded higher against most of the other major currencies on Monday and during the Asian session Tuesday. It underperformed only against CHF, while it was found virtually unchanged against GBP. The greenback gained the most versus CAD, AUD, and JPY, in that order.

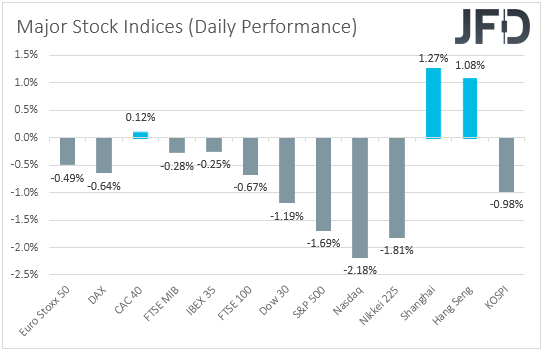

The strengthening of the US dollar and the Swiss franc, combined with the weakening of the risk-linked Loonie and Aussie, suggests that financial markets may have traded in a risk-off manner yesterday and today in Asia. Only the weakening of the yen points otherwise. Indeed, turning our gaze to the equity world, we see that most major EU indices traded in the red, with the negative appetite intensifying during the US session. It improved partially during the Asian session today.

In our view, investors may have continued reducing their risk exposures on fears that the Fed may proceed with an even more aggressive rate path than projected in the last “dot plot”, and this is supported by the rise in Treasury yields as well.

With that in mind, today, the spotlight is likely to fall on the US CPIs for March. Both the headline and core rates are forecast to have continued rising, despite the Fed and other major central banks around the world beginning a normalization process. Specifically, the headline rate is anticipated to have risen to +8.4% yoy from +7.9%, while the core one is anticipated to have inched up to +6.6% yoy from +6.4%.

At the prior FOMC gathering, the Committee hiked interest rates by 25bps for the first time since 2018, with the updated “dot plot” pointing to 6 more quarter-point increases until the end of the year. This means one lift off at each of the remaining gatherings for 2022. That said, since then, Fed officials, including Fed Chair Jerome Powell, appeared even more hawkish, noting that they could use larger liftoffs if needed, something also confirmed by the minutes of the last meeting, released last week.

According to the CME FedWatch Tool, investors are now pricing in an 84.3% chance for a double hike at the upcoming meeting, scheduled for the 4th of May, while they assign a 55.5% probability for another double increase to follow in June. They even see a 35.5% likelihood for a 75bps increase in June. Thus, following another strong employment report around 10 days ago, further acceleration in inflation could add credence to the view of very aggressive tightening by the Fed and may push the US dollar higher. At the same time, equities are likely to continue correcting south.

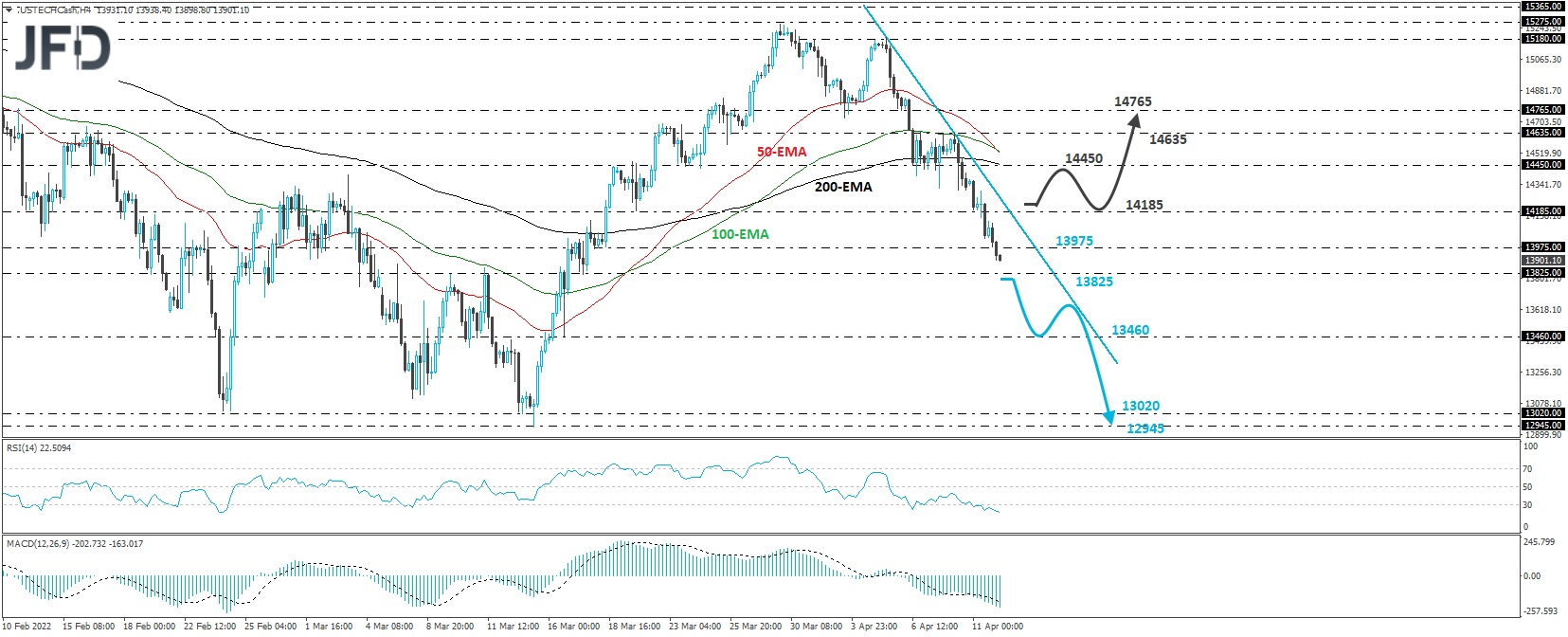

Nasdaq 100 – Technical Outlook

The Nasdaq 100 cash index continued drifting south yesterday, breaking below the 14185 barrier marked by the low of March 21st. Overall, the index has been in a short-term downtrend after it reversed south by completing a failure swing top on April 6th. The short-term downtrend is marked by a downside line taken from the peak of April 5th.

At the time of writing, the cash index looks to be headed towards the low of March 17th, at 13825, the break of which could invite more bears and perhaps pave the way towards the low of the day before, at around 13460. If that barrier doesn’t hold, then its break could carry larger bearish implications, perhaps paving the way towards the 13020 or the 12945 zones, marked by the lows of February 24th and March 15th, respectively.

On the upside, we will start examining the case of a decent recovery upon a break above 14185. This could confirm the break above the aforementioned downside line as well, and may encourage advances towards the 14450 zone, marked by the lows of March 24th and 25th. If the bulls are not willing to stop there, then we may see them marching towards the 14635 level, or the 14795 zone, marked by the high of April 8th, and the inside swing low of April 1st, respectively.

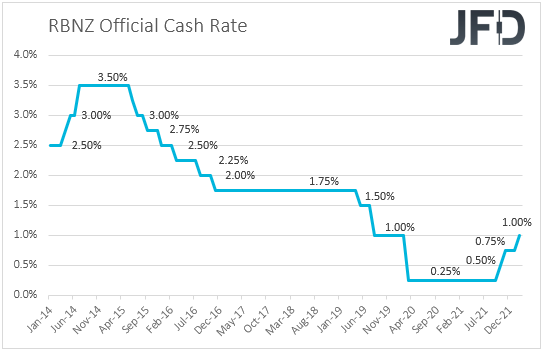

Will The RBNZ Hike by 25 or 50bps?

Tonight, during the Asian session Wednesday, we have a central bank deciding on its own interest rates and this is the RBNZ. When they last met, officials of this Bank decided to push the hike button for the third straight meeting, lifting interest rates by another 25bps, to 1%. The Bank also steepened its rate-path projections, with officials projecting that the OCR will hit 3.35% by the end of 2024, instead 2.6% predicted in November. For the end of this year, they see the rate being lifted to 2.5%, a quarter-point higher from 2.25% seen in November.

At this gathering, the Bank is expected to continue lifting rates, by another 25bps, but some participants call for a half-point increase to +1.50%. Perhaps this is because supply chain disruptions and a tight labor market have pushed inflation up to a three-decade high of +5.9% yoy in the last quarter of 2021. Remember that the target range of the RBNZ is between 1 and 3%. That’s double the upper bound. Having said all that though, we have yet to receive inflation data for the first quarter of this year, and thus, we believe that policymakers will just proceed with the expected 25bps increase until they have concrete evidence as to whether more is needed.

Therefore, a 25bps increase by itself is unlikely to move much the New Zealand dollar. For the Kiwi to rebound, this needs to be accompanied by an even more hawkish language than previously, pointing to even faster rate hike. Now, in case the narrative is more or less the same as last time, the currency is likely to slide, especially against its US counterpart, bearing in mind the expectations over a very aggressive Fed. The third scenario, and the one that carries the least likelihood in our view, and consequently the biggest element of surprise, is a double hike. This could result in a stronger and longer rebound than in the case of just a hawkish language.

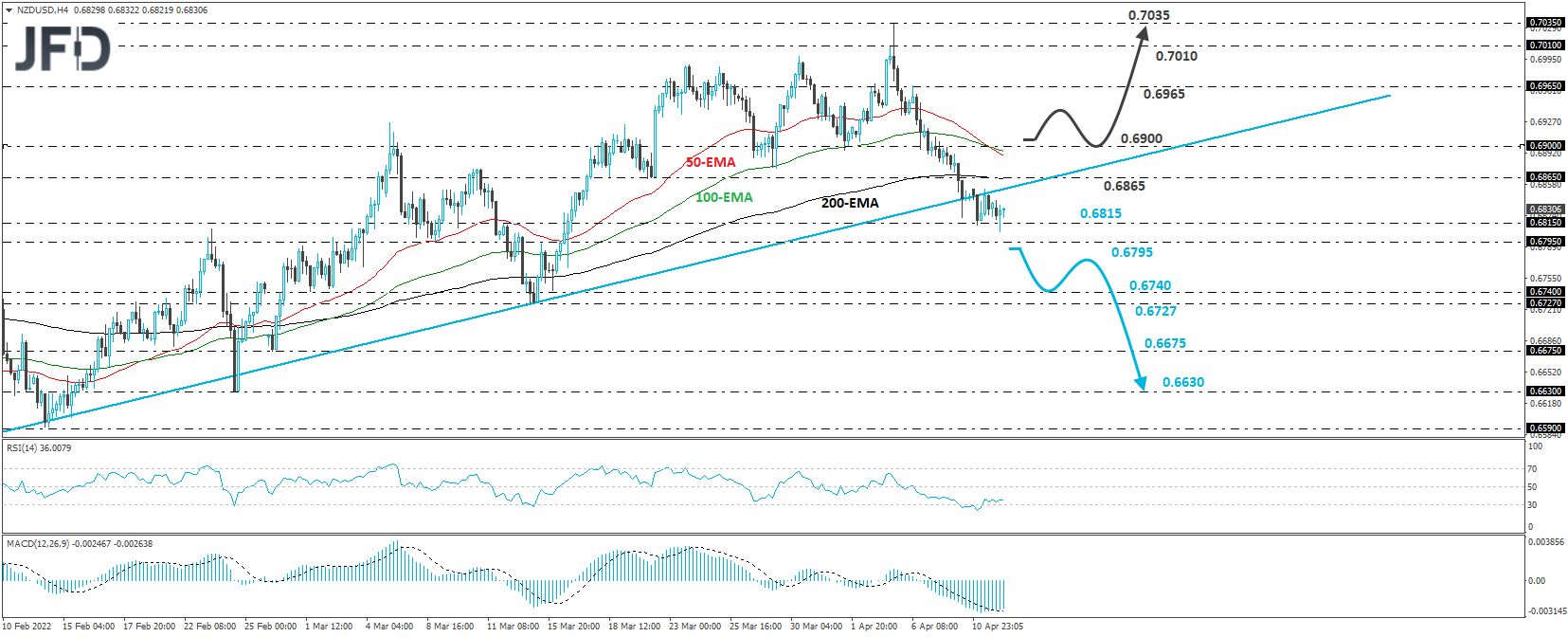

NZD/USD – Technical Outlook

NZD/USD traded in a consolidative manner yesterday and today in Asia, after breaking below the upside support line drawn from the low of January 28th. With that in mind, we will abandon the bullish case for now, and turn neutral. We will start examining the completion of a bearish reversal upon a dip below 0.6795, a support marked by the low of March 9th.

This would confirm a forthcoming lower low on the 4-hour chart and may pave the way towards the 0.6727/40 area, marked by the lows of March 15th and 16th respectively. Another break, below 0.6727, could see scope for more declines, perhaps towards the low of February 27th, at 0.6675, or even the low of February 24th, at 0.6630.

We will start examining the resumption of the prevailing uptrend upon a break back above the 0.6900 zone, marked by the low of April 1st. This may encourage the bulls to climb towards the 0.6965 hurdle, marked by the peak of April 6th, the break of which could carry extensions towards the peak of the day before, at around 0.7035.

As for the Rest of Today’s Events

During the early EU session, we already got the UK employment report for February. The unemployment rate ticked down to 3.8% from 3.9%, while the net change in employment showed that the economy has gained 10k jobs after losing 12k in January. The forecast was for a 50k gain.

In a while, the German ZEW survey for April is coming out, with both the current conditions and expectations indices expected to have fallen even deeper into the negative zone.

As for tomorrow, a few hours after the RBNZ decision, we get the UK CPIs for March, with both the headline and core rates expected to have continued drifting north. At their last gathering, BoE officials decided to hike interest rates by another 25bps via an 8-1 voting, with the dissenter calling for no increase at all. Remember that at the February gathering, officials lifted rates by 25 bps as well, but the vote was 5-4, with the dissenters calling for a 50bps increase. Compared to that, March’s decision revealed a more cautious approach by policymakers and raised questions as to whether they will indeed proceed as aggressive as the market has been pricing in heading into the gathering.

That said, with inflation accelerating in February, and expected to continue so in March, market participants are likely to stay convinced that the BoE may need to act more quickly, something that could support the British pound, especially against the Japanese yen. Remember that the BoJ has pledged to keep its policy extra loose at a time when other major central banks are in a race of tightening. This monetary policy divergence is likely to continue weighing on the Japanese currency.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 73.82% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2022 JFD Group Ltd.