Following a busy week, with three major central bank decisions, as well as the US jobs data, the calendar becomes lighter this week, especially during the first three days. However, bearing in mind the geopolitical tensions in Ukraine, we cannot rule out volatile market swings. On Thursday, we have the US CPIs, which could add to the case of more aggressive tightening by the Fed, while on Friday, we get the preliminary UK GDP for Q4, which could shape expectations on how the BoE plans to move forward.

On Monday, during the Asian session, we already got Australia’s retail sales for Q4, and China’s Caixin services and composite PMIs for January. Australia’s retail sales rebounded strongly, which may have allowed Aussie traders to keep bets over several hikes by the RBA this year elevated. The Chinese indices slid somewhat, but remained above the boom-or-bust zone of 50.

As for the rest of the day, we don’t have any major release on the agenda, but we do have a speech by ECB President Christine Lagarde. Last week, at the press conference following the ECB decision, she said that inflation remained elevated for longer than previously thought, and that the economy was hurt less than anticipated by the pandemic. She also added that the March and June meetings will be essential for evaluating their guidance, which means that they could, after all, decide to lift rates in 2022. Remember that prior remarks by her and several of her colleagues were highlighting the case of no liftoffs this year. Now, that door is open, and comments adding to that chance could allow some more euro buying.

On Tuesday, Asian time, we get Australia’s NAB business confidence index for January, for which no forecast is available, while later in the day, we have the US NFIB small business optimism index for January and Canada’s trade balance for December. No forecast is available for the NFIB index either, while Canada’s trade surplus is expected to have decreased to CAD 2.62bn from CAD 3.13bn.

On Wednesday, the only release worth mentioning may be Germany’s trade balance for December, with the forecast pointing to a small decline in the nation’s surplus, to EUR 10.4bn from EUR 10.9bn. That said, Germany’s trade balance has very rarely been a market mover and thus, we don’t expect any reaction by the common currency at the time of this release.

For more than half of the week, the economic agenda appears very light, but that doesn’t necessarily mean a quiet trading activity. Let’s not forget that tensions in Ukraine remain elevated and new developments could easily result in violent market swings. Following reports by US President Biden’s administration to the US Congress that Russia has build up 70% of the necessary force to invade Ukraine entirely, French President Macron is scheduled to speak with Russian President Putin today and tomorrow, while US President Joe Biden is scheduled to meet with German Chancellor Olaf Scholz today. Any resolution or escalation has the potential to not only affect oil prices, which hit USD 90 per barrel for the first time since 2014, but also the broader market sentiment.

On Thursday, the spotlight is likely to fall to the US CPIs for January, with both the headline and core rates expected to have continued to rise. Specifically, the headline CPI is expected to have accelerated to +7.3% yoy from +7.0%, and the core one to jump to +5.9% yoy from 5.5%.

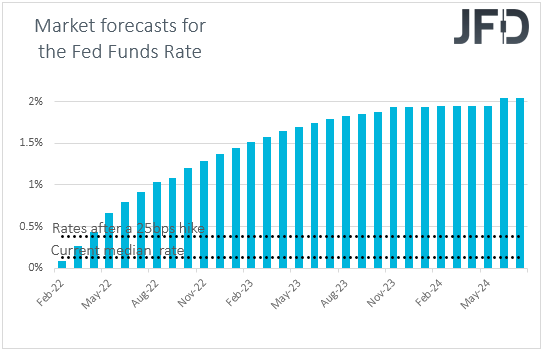

The message we got from the latest FOMC decision is that a hike is coming in March, but most importantly, there is a decent likelihood for more lift-offs this year than the December “dot plot” suggested. Although the US dollar slid in the days after the meeting, Friday’s better-than-expected jobs report sparked a fresh round of buying, perhaps adding more credence to the view of faster tightening. According to the Fed funds futures, investors are indeed fully pricing in a 25bps hike for March, while they see another four by the end of the year. Remember that the December “dot plot” pointed to only three quarter-point liftoffs for this year. So, with all that in mind, further acceleration in inflation could encourage participants to add to their bets and perhaps help the dollar move higher. At the same time, expectations over higher rates sooner could hurt equities, as this means higher borrowing costs, but also lower present values, especially for high-growth firms, which are usually valued by discounting expected cashflows for the months and years ahead.

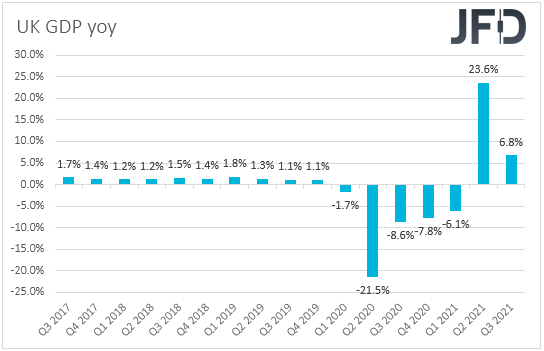

Finally, on Friday, attention is likely to turn to the UK, and the preliminary GDP for Q4, which is forecast to have grown 1.1% qoq, the same quarterly pace as in Q3. However, this is likely to take the yoy rate slightly lower, to +6.5% from 6.8%. At the same time, we get the nation’s industrial and manufacturing production rates for December, and both of them are expected to have declined notably.

At last week’s decision, the BoE decided to lift interest rates by 25bps, to 0.50%, via a 5-4 vote, with the 4 dissenters calling for a 50bps hike. Given that only one member needs to be convinced that a double hike may be appropriate at the next gathering, economic data may attract more attention moving forward. Therefore, a positive surprise could increase speculation for a double hike at the next BoE gathering and perhaps support the pound, while a disappointment could add to the case for another quarter-point liftoff, which could prove negative for the currency, as this is already fully priced in.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 73.82% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2022 JFD Group Ltd.