This week, focus for USD-traders is likely to fall on the US core PCE index, the Fed’s favorite inflation gauge, while CAD-traders may lock their gaze on Canada’s GDP as they try to better assess the timing of the next BoC rate hike. Eurozone’s preliminary CPI data for August and Carney’s testimony on the Inflation Report could attract some attention as well.

On Monday, the calendar appears very light with the only release worth mentioning being the German Ifo survey for August. The current assessment index is anticipated to have risen to 105.5 from 105.3 in July, while the expectations one is forecast to have moved up to 98.5 from 98.2. This would drive the business climate index up to 102.0 from 101.7. The case for rising Ifo indices is also supported by the ZEW survey for the month, both indices of which have risen as well.

On Tuesday, the only relatively important event is BoE Governor Carney’s testimony on the August Inflation Report before Parliament’s Treasury Committee. The main message we got from Governor Carney at the press conference following the latest meeting, as well as in an interview for BBC soon thereafter, was that the Bank is probably done hiking for this year. He noted that market pricing for a hike per year for the next few years is a good rule of thumb, but with the caveat that it will depend on what happens with Brexit. With concerns over a no-deal Brexit at elevated levels, we find it hard for Carney to deliver anything more optimistic than he did then. In general, we expect pound traders to keep most of their attention on headlines surrounding the political front rather than monetary policy.

On Wednesday, the second estimate of the US GDP for Q2 is due to be released. Expectations are for a downside revision to 4.0% qoq SAAR from 4.1% qoq SAAR, but this would still mark the strongest rate in nearly four years. US pending home sales for July are also coming out and expectations are for a slowdown to +0.4% mom from +0.9% in June.

From Canada, we get current account data for Q2. Expectations are for the nation’s current account deficit to have narrowed somewhat, to CAD -15.3bn from CAD -19.5bn.

On Thursday, during the Asian morning, Japan’s retail sales for July are expected to have slowed to +1.2% yoy from +1.7% yoy in June. New Zealand’s ANZ business confidence index for August and Australia’s building approvals for July are also due to be released.

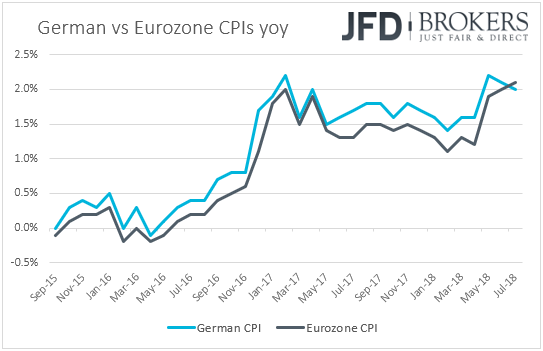

During the European morning, Germany’s preliminary inflation data for August are coming out. Expectations are for the German CPI rate to have remained unchanged at +2.0% yoy, which could raise speculation that Eurozone’s headline print, due out on Friday, may have held steady as well. Germany’s unemployment rate for August is due out as well, and it is expected to have stayed at 5.2%.

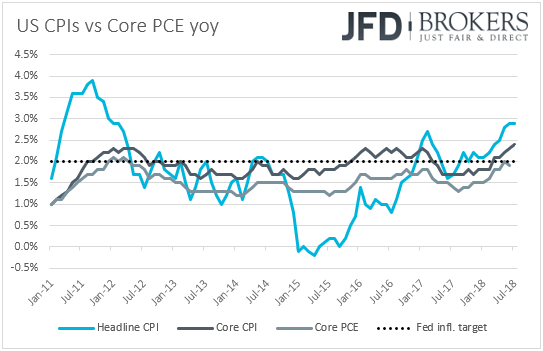

In the US, we get personal income and spending data for July, as well as the core PCE index for the month. Personal income is expected to have slowed somewhat, to +0.3% mom from +0.4%, while spending is expected to have risen +0.4% mom, the same pace as in June. That said, the accelerations in the monthly earnings and retail sales prints for the month suggest that the risks surrounding both the income and spending forecasts may be tilted to the upside.

With regards to the core PCE yearly rate, the Fed’s preferred inflation measure, it is expected to have ticked back up to the Fed’s objective of 2.0%. This is supported by the fact that the core CPI rate for the month ticked up as well. A 2.0% core PCE rate could raise some speculation that the Fed could change its inflation language when it meets next, from inflation remains near its target to inflation has reached the target, and is likely to keep the Fed on track for raising rates two more times this year.

On Friday, at Jackson Hole, Fed Chairman Jerome Powell reiterated that gradual hikes are likely appropriate if strong income and job growth continue, but he also noted that there is little risk for inflation to accelerate beyond the Fed’s target. In our view, although this still keeps the door open for two more rate hikes this year, it suggests that as soon as interest rates reach their neutral level (which the Fed sees close to 3%), policymakers may decide to pause instead of keep tightening. According to the Fed’s latest dot plot, officials anticipate 3 more hikes in 2019, but the Fed funds futures suggest that market participants are almost fully pricing in only one. Thus, we believe that investors may soon start shifting their attention to the 2019 rate path. Even if the Fed decides to hike in September, bearing in mind that this is almost fully priced in and that the likelihood for a December hike remains decent as well, investors may prefer to pay more attention to the updated dot plot and the 2019 dots. Following Powell’s remarks, they may be eager to see whether the 2019 median be revised lower or not.

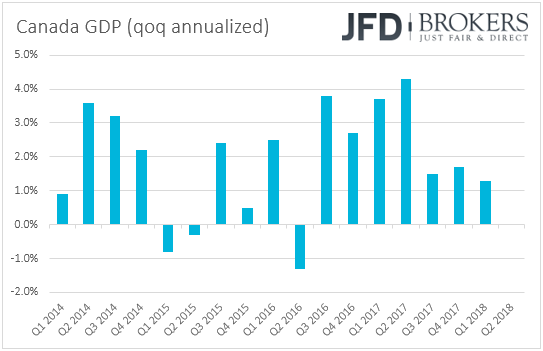

In Canada, we get GDP data for both June and Q2. With regards to the monthly rate for June, expectations are for a slowdown to +0.1% mom from +0.5% in May, but the qoq annualized rate for Q2 is forecast to have risen to +3.0% from +1.3% in Q1. Canada’s latest economic data have been more than encouraging. Both headline and core inflation metrics accelerated more than anticipated in July, while the unemployment rate for the same month slid to 5.8% from 6.0% in June. Thus, an acceleration in the nation’s qoq annualized growth rate could further increase the likelihood for another BoC rate increase by the end of the year. While most participants believe that October is the most likely candidate, a better than expected GDP print could tempt some participants to place bets that the hike could be delivered even at the September gathering.

Finally, on Friday, we get the usual end-of-month data dump from Japan. The nation’s unemployment rate for July is expected to have stayed unchanged at 2.4%, while the preliminary industrial production data for the month are anticipated to show that IP rebounded +0.2% mom after falling 1.8% in June. The Tokyo CPIs for August are also due to be released. Both the headline and core rates are expected to have ticked down to +0.8% yoy and +0.7% yoy, from +0.9% and +0.8% respectively.

From China, we have the official manufacturing and non-manufacturing PMIs for August. Expectations are for both PMIs to have declined to 51.0 and 53.8, from 51.2 and 54.0 respectively.

During the European morning, Eurozone’s preliminary inflation data for August are coming out and expectations are for both the headline and core rates to have remained unchanged at +2.1% yoy and +1.1% yoy respectively, something that is unlikely to alter market expectations with regards to the ECB’s future plans. Even a small upside surprise is doubtful to do that. At the press conference following the latest ECB meeting, President Draghi noted that according to money markets, expectations of the future rate path are very well aligned with the anticipation of the Governing Council, backing the market consensus for a hike in late 2019, and disappointing those expecting to get clues that summer months are also candidates for such a move. In our view the “at least through the summer of 2019” interest-rate guidance means that rates could start rising in September 2019 the earliest. Thus, even if inflation accelerates somewhat, there is not much room for hike expectations to come forth. Germany’s retail sales for July are due to be released as well.

From the US, we have the final UoM consumer sentiment index for August, which is expected to have been revised up to 95.5 from 95.3. The final UoM 1- and 5-year inflation expectations for the month are also coming out.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.