‘Risk on’ was once again the main game in town yesterday as headlines that US-China talks entered a third day increased hopes that a deal may be closer than previously thought. As for today, apart from news on the trade front, CAD traders are likely to focus on the BoC rate decision. No action is expected but given that this is one of the “bigger” meetings, attention is likely to fall on the statement, the economic projections and the press conference by Governor Poloz. The minutes from the latest FOMC meeting are also published.

‘Risk-on’ Prevails as Hopes for US-China Truce Increase

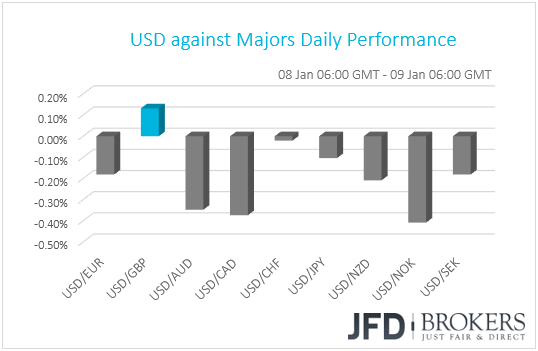

The dollar traded lower against most of the other G10 currencies on Tuesday. It gained only against GBP, while it traded virtually unchanged versus CHF. NOK, CAD, AUD and NZD were the main winners, while the yen was the currency that gained the least.

The strengthening of the commodity-linked currencies and the failure of the safe-havens to gain ground suggests that the broader risk appetite remained supported. Indeed, European and US equity indices were a sea of green yesterday, with the positive sentiment rolling into the Asian morning Wednesday. This was mainly due to headlines that the US and China will extend trade talks for a third day, something that may have increased hopes that the two nations may eventually find common ground, and even sooner than previously anticipated. US President Trump fueled those hopes using his twitter account to say that “Talks with China are going very well!”.

As we noted yesterday, headlines pointing to that direction are likely to add to the recent recovery in equity markets, and this could also be the case today. However, even amidst elevated hopes surrounding a US-China trade truce, we remain skeptical as to whether a final accord can be agreed today. In our view, there are still challenging issues unresolved, like intellectual property rights and market access, and with nearly two months until the deadline for sealing a final deal, we believe that the two sides may prefer to use some of this time to their benefit. We stick to our guns that these negotiations may open the way for more talks, with the next round perhaps taking place at the World Economic Forum in Davos later this month, between US President Trump and China’s Vice President Wang Qishan.

Oil prices gained as well due to expectations that the two nations are close to give an end to their conflicts, with both Brent and WTI gaining around 2.2% and 3.0% respectively. However, the main driver for the black liquids may have been the supply cuts agreed by OPEC and its allies, which took effect at the turn of the year.

Back to the currencies, the pound came under selling interest as comments by UK Brexit minister Stephen Barclay that the government sticks to its plan on departing from the EU on the 29th of March may have prompted GBP- traders to liquidate some of their prior long positions. Barcley’s comments came as a denial to Monday’s headlines that UK and EU officials are discussing the possibility of an extensions.

This week, GBP traders are likely to keep their gaze locked on the Parliamentary debate over PM May’s plan, with the vote scheduled to take place next week. With May still facing opposition from all sides within the Parliament, the plan is set to be rejected. Unless of course the Prime Minister secures concessions from the EU and then manages to convince MPs to support her deal, a conditional probability we see as very low, given the EU’s stance that the current deal is not negotiable.

NASDAQ 100 – Technical Outlook

The Nasdaq 100 cash index traded higher yesterday and today during the Asian morning it managed to break above the 6560 barrier. Although the index is still trading below the medium-term downside resistance line drawn from the peak of the 1st of October, since the 26th of December, it has been printing higher peaks and higher troughs above a short-term upside support line. Therefore, we believe that there is room for some further recovery.

We would expect the bulls to take charge again soon and drive the battle higher, towards the 6710 zone, marked by an intraday peak formed on the 14th of December. Another break above that resistance may pave the way towards the aforementioned downside line or the 6840 hurdle, which provided decent resistance from the 5th until the 13th of December. However, before that happens, we see the case for a small setback, perhaps for the price to test the 6455 level, or the short-term upside support line.

Our view for a corrective pullback is derived from our short-term oscillators. The RSI has started to top near its 70 barrier, while the MACD, although above both its zero and trigger lines, shows signs of topping as well. It could fall back below its trigger soon.

That said, in order to start examining whether buyers have totally abandoned the battlefield, at least in the near-term, we would like to see a clear and decisive dip below 6380. Such a dip could confirm the break below the short-term upside line and could initially aim for the 6285 level, marked by the inside swing high of the 3rd of January. Another break below that support could extend the slide towards the 6140 area, which proved to be a good support on the 2nd, 3rd and 4th of the month.

Bank of Canada Holds the First G10 Policy Meeting for 2019

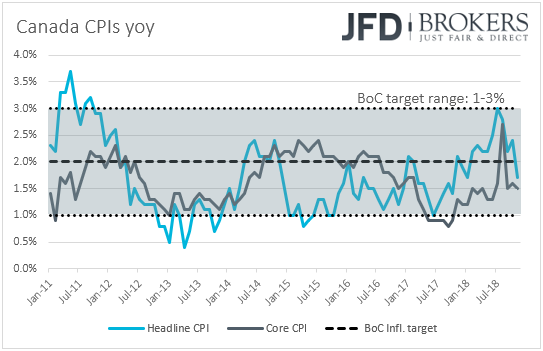

Today, we have the first G10 central bank meeting for 2019, and it’s from the BoC. At their previous meeting, Canadian policymakers kept interest rates unchanged at +1.75% as was widely anticipated, but the accompanying statement had a dovish flavor compared to the hawkish one we got in October. The key takeaway was that the economy is not as close to its potential as previously thought, which implies slower rate increases moving forward than previously thought. What’s more, officials also noted that the steep slide in oil prices may result in materially weaker-than-expected activity in the energy sector.

This may have prompted market participants to take their January-hike bets off the table. Although Canada’s record employment numbers for November may have revived some hopes on that front, the disappointment in Canada’s inflation prints for the month, combined with the further slide in oil prices in the aftermath of that meeting may have wiped out any such hopes. Even after the December employment report, which showed that the labor market remained strong, we doubt that the Bank will rush into hiking rates at this meeting. If this is the case, given that unchanged interest rates are now widely anticipated by the financial community, we expect all the attention to fall in the accompanying statement, the updated economic projections and the press conference by Governor Poloz.

In our view, the prior dovish statement leaves little room for policymakers to appear even more dovish. Yes, inflation disappointed in November, but the Bank has already said that it expects the CPI to ease by more than it has previously forecast, due to lower gasoline prices. What’s more, oil prices have been on a steady recovery since the beginning of the year, while trade tensions have eased notably, with both China and the US willing to give an end to their conflict.

We believe that this may allow officials to maintain the view that interest rates will need to rise further, which may support the Loonie somewhat. Even if it doesn’t, any further gains in oil prices combined with further encouraging headlines surrounding the global trade front may keep the Canadian dollar supported for a while. In order for CAD-traders to get disappointed and thereby, liquidate their long positions, the Bank has to sound even more dovish than it did at the prior meeting.

USD/CAD – Technical Outlook

USD/CAD hasbeen in a steep slide since the turn of the year, and on the 7th of the month, it fell below the medium-term uptrend line drawn from the low of the 1st of October. Yesterday, the pair dipped below the 1.3270 support and now looks ready to challenge the 1.3220 zone. In our view, the break below the aforementioned uptrend line has turned the near-term outlook to the downside and thus, we would expect the pair to continue drifting lower for a while more.

If the bears stay in the driver’s seat and manage to push the rate below the 1.3220 zone, then we may see them targeting the lows of the 3rd and 4th of December, at around 1.3160. Another break below 1.3160 could allow them to put the 1.3125 obstacle on their radars, a support marked by the low of the 16th of November.

Taking a look at our short-term momentum studies, we see that the RSI lies well within its below-30 territory and points down, while the MACD, at extreme low levels, lies fractionally above its trigger line. Both indicators detect strong downside momentum, but the fact that the MACD has bottomed and moved above its trigger make as cautious that a corrective bounce may be in the works soon, perhaps from current levels, or after the rate challenges the 1.3160 barrier.

Now in case such a rebound extends above 1.3270, the bears may decide to abandon the action for a while. Such a break may open the path for the 1.3330 zone, the break of which may extend the recovery towards the 1.3370 territory, or the aforementioned prior medium-term uptrend line. Having said that though, even if this is the case, the broader outlook would still be cautiously negative we believe. We would like to see a clear close back above the uptrend line and the 1.3415 area before we start examining whether the bulls have gained the upper hand.

As for the Rest of Today’s Events

The minutes from the December FOMC meeting are also due to be released. At that meeting, the Committee decided to raise interest rates to the 2.25-2.50% range and revised lower its rate path projections, with the median dot for 2019 pointing to 2 hikes instead of 3 as the September plot suggested. Having in mind that this was one of the “bigger” meetings, and also that we got Fed Chair Powell’s view on monetary policy last Friday, we believe that there is not much new information to get from these minutes. Instead, given that we have several Fed speakers throughout the week, including another speech by Powell on Thursday, we prefer to concentrate more on what officials have to say at this point of time. Today, we will get to hear from Atlanta Fed President Raphael Bostic, Chicago Fed President Charles Evans and Boston Fed President Eric Rosengren.

With regards to the economic data, during the European morning, we get Switzerland’s CPI for December and expectations are for the yoy rate to have ticked down to +0.8% from +0.9% in November. From the Eurozone, we have the bloc’s unemployment rate for November, which is forecast to have held steady at 8.1%, and Germany’s trade data for the month, which is expected to show that the German surplus has increased somewhat.

As for the speakers, apart from the aforementioned Fed officials and BoC Governor Poloz, who will hold a press conference after the rate decision, we also have BoE Governor Mark Carney on the agenda.

As for tonight, China’s CPI and PPI for December are scheduled to be released. The yoy CPI rate is expected to have ticked down to +2.1% from +2.2%, while the PPI is forecast to have slowed to +1.7% yoy from 2.7%. This would be the lowest growth rate in producers’ prices since October 2016 and may add to concerns over China’s economic performance.

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Group, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Group analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD Group prohibits the duplication or publication without explicit approval.

68% of the retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2019 JFD Group Ltd.