Market sentiment remained supported yesterday, but Asian markets suggest that investors took a somewhat more cautious stance today, as the US-China talks entered a high-level phase. Yesterday, a report noted that President Trump is considering pushing back the March 1st deadline by 60 days, which suggests that the talks are progressing in the desired direction. In the UK, the Parliament will debate on a motion to approve May’s request for more time to renegotiate with the EU, with a chance of another round of voting on proposed amendments.

Investors Lock Gaze on US-China High-level Talks

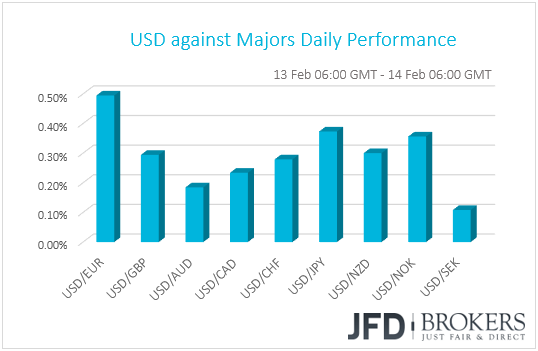

After taking a breather on Tuesday, the dollar rebounded yesterday, outperforming all its G10 peers. The main loser was EUR, with JPY and NOK taking the second and third place respectively. The currencies that underperformed the least were SEK and AUD in that order.

The dollar rebounded after a Tuesday’s setback, perhaps aided by the slightly better-than-expected US inflation data. Headline inflation slowed to +1.6% yoy in January from +1.9%, in line with expectations, but the core rate held steady at +2.2% yoy, instead of ticking down to +2.1% as the forecast suggested. According to the Fed funds futures, this has raised somewhat the chances for a Fed hike by year end, to 12%, and reduced the likelihood of a cut, from 10% to 6%.

The euro was yesterday’s big loser, perhaps pulled down by Eurozone’s disappointing industrial production data for December. The data showed that production continued shrinking for the second consecutive month, and although at a slower pace than November, the pace was faster than anticipated. This is another release entering the basket of those suggesting that the Euro-area economic activity continues to slow, adding to speculation that the ECB may not proceed with raising interest rates this year.

The Swedish Krona was the currency that lost the least ground, resisting the dollar’s strength after the Riksbank kept interest rates unchanged at -0.25%, reiterating that the next increase is likely to come during the second half of 2019 and keeping its repo-rate path unchanged. Officials also noted that although growth is more subdued, economic activity is still strong and that the conditions for inflation to remain close to 2% have not changed to a great extent. The Bank also dropped its intervention mandate, with Governor Stefan Ingves saying that the need no longer exists. All this may have come as a surprise to those expecting a more cautious stance, and that’s why the Swedish currency strengthened at the time of the release, ending the day higher against all the G10s, except the dollar.

With regards to the broader market sentiment, although not so clear by the performance in the FX sphere, the equity world suggests that it remained supported. Major EU and US indices closed their sessions slightly in the green, but Asian markets suggest that investors took a somewhat more cautious stance today, as the US-China talks entered a high-level phase.

“Looking forward to discussions today,” US Treasury Secretary Steven Munching told according to media reports as he left his hotel, while on Wednesday, US President Trump said that the talks were “going along very well,” adding further fuel to expectations that a final accord is getting closer. Most importantly, a Bloomberg report citing people familiar with the matter noted that the President is considering pushing back the March 1st deadline by 60 days. If this is true, it implies that indeed the talks are progressing in the desired direction and that Trump and China’s Xi Jinping could sign a deal soon and end the dispute. Yesterday, we noted that we see the delay as a one-way path if Trump actually wants to secure a deal, and this is what the headline suggests. As for our view it remains the same as yesterday. Further positive remarks could keep investors’ morale supported for a while more, but for a more sustained recovery in risk appetite, we would like to see the two leaders signing a final accord.

USD/JPY – Technical Outlook

This week, USD/JPY continued to grind higher, breaking above the 110.10 barrier and reaching the 111.00 zone yesterday. Now the big question is, can the pair maintain its gains till the end of the week? The positive aspect of USD/JPY is that it continues to trade above, not only its upside support line taken from the low of January 3rd, but also above a very short-term upside line drawn from the low of January 31st. For now, even if we see a small correction back down, as long as the above-mentioned short-term upside line remains intact, we will continue aiming higher.

A move lower could send USD/JPY for a re-test of the 110.70 level, which recently acted as resistance, and now it may take the role of support. Even if the rate travels a bit lower, still, there is that aforementioned short-term upside line, which may support the pair. This is when the bulls might come back in again and drive USD/JPY higher, towards the next potential strong resistance area, at 111.40, marked by the high of December 26th. Another break, above 111.40, could carry more upside extensions and perhaps open the way for the 112.10 zone.

Alternatively, a rate-drop below the short-term upside line might temporarily spook the bulls from the field, which would allow the bears to push USD/JPY lower towards the 110.10 obstacle, marked by the highs of last week. If the pair continues to slide, we may see a test of the 109.60 support zone, which is also close to the previously mentioned upside support line, taken from the low of January 3rd. This is where the rate may get held, until the bulls and the bears figure out who takes control from there.

![]()

Pound Traders Await for UK Parliament's Debate

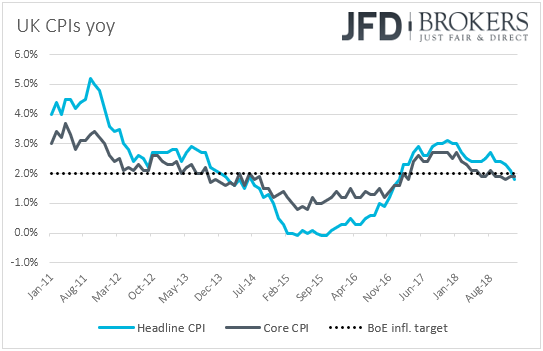

For pound traders it's all about Brexit, and this is proven by the fact that they reacted very little to the UK inflation data. The data showed that headline inflation slowed by more than anticipated, to +1.8% yoy from +2.1%, while the core rate remained unchanged at +1.9% yoy. Under normal circumstances, this would have hurt the pound, as with both rates below the BoE’s 2% objective, the chances for a BoE rate hike in the months to come would have fallen. That said, we repeat that pre-Brexit inflation data do not matter for traders at the moment as everything could change after the UK departs from the EU. A potential no-deal outcome could cause the pound to plummet, something that could push inflation up again.

Yes, growth would get hurt, but the Bank’s view remains that interest rates could move in either direction, even in case of a disorderly withdrawal. As we have repeatedly noted in the recent past, we agree with that view. The Bank will have to assess the tradeoff and if bringing inflation back down to target appears a more urgent task than supporting growth, then the Bank may decide to raise rates. If the opposite is true, then a cut may be appropriate.

As for today, the UK Parliament is scheduled to debate on Brexit, with a chance of another round of voting on proposed amendments. The debate will be on a motion to approve May’s request for more time to renegotiate with the EU. On Tuesday, PM May promised lawmakers that they will have another chance to express their opinion on February 27th if a revised deal is not accepted by then.

So, what could happen today? If May’s motion passes, nothing. In our view, it is a “kicking the can down the road” motion, and we would have to wait until February 27th. Yes, EU officials agreed to resume talks with May, but stayed adamant to their position to not renegotiate the existing agreement. EU chief negotiator Michel Barnier insisted earlier this week that Brussels will not give in to the UK’s demands on the Irish backstop, which suggests that the chances for May coming back with a broadly accepted accord remain very low.

With regards to the amendments, even if some pass today, they are not binding on the government. However, they could show where the Parliament stands and what we may get on February 27th if May fails to secure a deal. With only one and a half month until the official divorce date, approving amendments which include extending Article 50, like the one proposed by Cooper on January 29th, could ease somewhat fears that the UK will crash out of the EU without in a chaotic manner and the pound could rebound somewhat. On the other hand, a repeat of the decisions taken on 29th could add to no-deal Brexit fears, and the British currency could extend its latest downtrend.

GBP/CAD – Technical Outlook

GBP/CAD keeps on trading below its tentative short-term downside resistance line taken from the high of January 29th. Yesterday, the bulls made an attempt to drive the pair higher, but failed near the 1.7130 hurdle, from where the bears took control again. We will continue aiming a bit lower, at least for a little while.

A further move lower could make GBP/CAD test the 1.7005 obstacle, which is yesterday’s low. The pair could rebound slightly, but if it remains below the 1.7050 barrier, more bears could join in and bring the rate even lower. This is when we will target the strong support zone, at 1.6960, a break of which may send the pair further down towards the 1.6930 hurdle, marked by the high of January 9th.

On the other hand, in order to get comfortable with the upside, we would like to see a break of the aforementioned downside resistance line first and then a rate-rise above the 1.7130 barrier. This way, the path could get cleared towards higher resistance areas, like the 1.7190 level, which is near the high of February 11th. If the buying doesn’t end there, the bulls could continue driving GBP/CAD to its next potential resistance zone, at 1.7270, marked by the high of February 8th.

![]()

As for the Rest of Today’s Events

During the European morning, Eurozone’s second estimate of Q4 GDP is coming out and is expected to confirm its preliminary print of +0.2% qoq. Later in the day, we may get the US retail sales for December, which were delayed due to the government shutdown. The release is expected to show that the headline rate ticked down to +0.1% mom from +0.2% in November, and that core sales stagnated after rising +0.2% as well. The US PPIs for January and initial jobless claims for the week ended on February 8th are also on the agenda. Both the headline and core PPI rates are expected to have declined, to +2.1% yoy and +2.5% yoy from +2.5% and +2.7% respectively, while jobless claims are expected to have decreased to 225k from 234k.

As for tonight, during the Asian morning Friday, China’s CPI and PPI data for January are coming out. The CPI rate is expected to have held steady at +1.9% yoy, while the PPI is forecast to have slowed to +0.3% yoy from +0.9%. Japan’s final industrial production for December is also due to be released and it is expected to confirm its preliminary estimate, namely that production slid 0.1% mom.

With regards to the speakers, we have three on the agenda: BoE MPC member Gertjan Vlieghe, Philadelphia Fed President Patrick Harker, and RBA Assistant Governor Christopher Kent.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Group, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Group analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD Group prohibits the duplication or publication without explicit approval.

76% of the retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2019 JFD Group Ltd.