Following the US midterm elections and several central bank decisions, including the Fed, the calendar appears to be dictated by economic data this week. In the UK, we have employment, inflation and retail sales data. We get inflation figures from the US as well. On the political front, Tuesday is the deadline for Italy to submit its revised budget plan to the EU Commission.

Monday is a relatively light day with no major releases or events on the agenda.

On Tuesday, during the Asian morning, Australia’s NAB survey for October is due to be released, but no forecast is currently available. Usually, this is not a market mover, but bearing in mind the RBA’s emphasis on wage growth, we will take a look at the Labour Costs sub-index. At last week’s meeting, the RBA maintained the view that wage growth has picked up a little, although it remains low. Officials also reiterated that the economy should see some further lift in wages. In the three months to September, the Labour Costs index slowed to +0.9% qoq from +1.3% in the three months to August and thus it would be interesting to see whether wages accelerated again, in line with the RBA’s view, or slowed further.

During the European day, we get the German ZEW survey for November. The current conditions index is forecast to have declined to 65.0 from 70.1, while the expectations index is anticipated to have risen fractionally, to -24.2 from -24.7. The nation's final CPI for October is also coming out and as usual, it is expected to confirm its preliminary estimate.

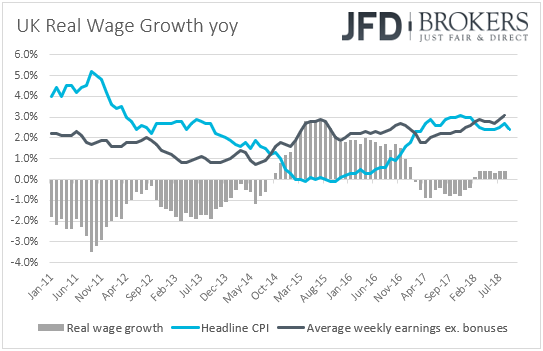

From the UK, we get employment data for September. Expectations are for the unemployment rate to have remained unchanged at its 43-year low of 4.0%, while average weekly earnings including bonuses are forecast to have accelerated to +3.0% yoy from +2.7% in August. The excluding-bonuses wage rate is forecast to have held steady at +3.1% yoy. According to the IHS Markit/REC Report on Jobs for the month, starting salaries for permanent placements rose at the fastest pace since April 2015, while temporary payment accelerated as well. In our view, the strong increases in both permanent and temporary pay suggest that the risks surrounding the ex-bonuses earnings forecast may be tilted to the upside.

With regards to politics, Italy will likely return to the spotlight, as Tuesday is the deadline for submitting its revised budget to the EU Commission. Revealing its own forecasts based on the policies the Italian government wants to put forward, the EU Commission suggested that Italy’s deficit could be in fact 2.9%, instead of 2.4% as Rome is insisting. On Friday, Italy’s finance minister Giovanni Tria said that he has no intention of altering Italy’s 2019 spending plans and thus, it would be interesting to see whether the EU will reject again the revised plan and proceed with imposing sanctions later this month.

On Wednesday, during the Asian morning, we get preliminary GDP data for Q3 from Japan. Expectations are for the Japanese economy to have shrunk 0.3% qoq, after growing 0.7% in Q2. This would drive the yoy rate into negative territory. Specifically, the yearly rate is expected to have fallen to -1.0% from +3.0%. A potential slide in economic activity, combined with the fact that all the nation’s inflation metrics stand well below the BoJ’s objective of 2%, would support our long-standing view that BoJ policymakers have a long way to go before they start considering a step towards normalization.

From Australia, we have the wage price index for Q3. Expectations are for the qoq rate to have remained unchanged at +0.6%, something that could push the yoy rate up to +2.3% from +2.1%. Although the quarterly rate of the NAB Labour Costs index declined to +0.9% in September, from +1.3% in August, it remained above June’s +0.8%. Therefore, we believe that the risks surrounding the quarterly rate of the wage price index are skewed somewhat to the upside.

China’s retail sales, industrial production, and fixed asset investment, all for October, are also due to be released. The retail sales and industrial production yearly rates are expected to have remained unchanged at +9.2% and +5.8% respectively, while fixed asset investment is forecast to have accelerated to +5.5% yoy from +5.4%.

During the European day, Sweden’s CPIs for October are coming out. Expectations are for the CPI rate to have ticked up to +2.4% yoy from +2.3%, while the CPIF rate is anticipated to have remained unchanged at +2.5% yoy. That said, we will pay more attention to the core CPIF metric, which excludes energy. In September, the core CPIF rate surged to +1.6% yoy from +1.2%, but at its latest meeting, the world’s oldest central bank repeated that interest rates will be raised either in December or February, which may have come as a disappointment to those who raised bets that the Bank will dismiss the February option.

It would be interesting to see whether the core CPIF will accelerate further, something that could revive hopes that December could be the most likely candidate for the Bank to act, or whether it will retreat again, pushing expectations to February. In any case, the Bank’s upcoming gathering is scheduled for the 20th of December, and up until then we will get another set of inflation data. Therefore, we prefer to wait for the next numbers before we start examining when the Bank will most likely hit the hiking button.

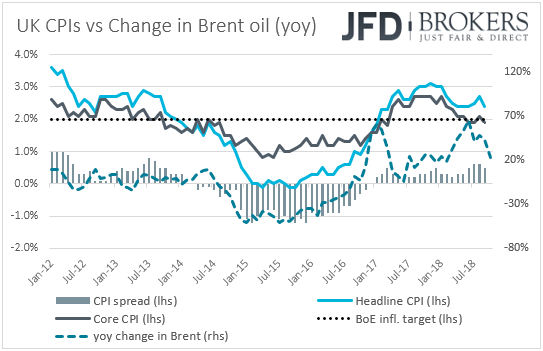

We get October inflation data from the UK as well. The forecasts suggest that the headline CPI rate accelerated to +2.5% yoy from +2.4%, while the core rate is anticipated to have remained unchanged at +1.9% yoy. At its latest policy meeting, the BoE kept interest rates unchanged and repeated that an ongoing tightening would be appropriate, with any further rate increases likely to be at a gradual pace and to a limited extent. That said, at the press conference, Governor Carney said that rates could go up even in case of a no-deal Brexit.

In our view, the meeting had a somewhat hawkish flavor, which may have encouraged market participants to bring forth their expectations with regards to the next BoE rate increase. According to the forward curve of the UK OIS (overnight index swaps), the market is fully pricing in a hike for December 2019. Ahead of the BoE meeting, a hike was fully priced in for May 2020. Therefore, conditional upon accelerating wages on Tuesday, accelerating inflation could prompt investors to bring further forth their bets. However, we stick to our guns that any move by the BoE is likely to occur after the official Brexit date, which is the 29th of March 2019.

In the Eurozone, Germany’s preliminary GDP for Q3, as well as the 2nd estimate of the bloc’s growth rate are coming out. Germany’s numbers are expected to show that Eurozone’s largest economy contracted 0.3% in the three months to September, after growing 0.5% the previous quarter. This will drive the yoy rate down to +1.2% from +2.3%. As for the Eurozone as a whole, the 2nd estimate is expected to confirm the preliminary figure, namely that the Euro-area has slowed to 0.2% qoq from +0.4%. Eurozone’s employment change for Q3 and industrial production for September are also due to be released. The employment change is forecast to have slowed in both quarterly and yearly terms, while industrial production for September is anticipated to have declined 0.4% mom after rising 1.0% in August.

At the latest ECB policy meeting, President Draghi maintained his fairly optimistic stance with regards to Euro area’s economic outlook, but the data keeps amplifying concerns over the bloc’s economic performance. The next ECB meeting is scheduled of the 13th of December, and if data continues coming on the soft side, it would be interesting to see whether Draghi would still consider the risks surrounding the Euro-area growth outlook as broadly balanced.

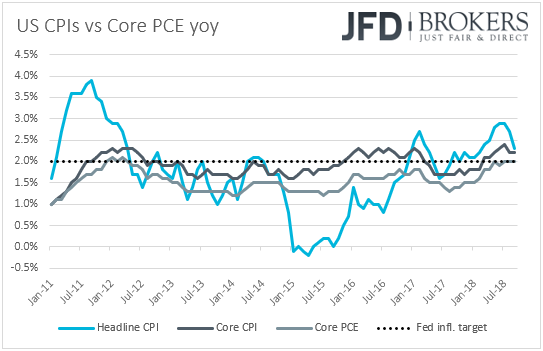

Later in the day, we have the US inflation data for October. Expectations are for the headline CPI to have accelerated to +2.5% yoy from +2.3% in September, while the core rate is forecast to have remained unchanged at +2.2% yoy. On Friday, data showed that the headline PPI for the month accelerated to +2.9% yoy from +2.6%, while the core PPI rate rose to +2.6% yoy from +2.5%. The PPIs support the case for an acceleration in the headline CPI and suggest that the risks surrounding the core forecast may be tilted to the upside.

At last week’s gathering, the Fed decided to keep interest rates unchanged within the 2.00-2.25% range as was widely expected, while officials made almost no changes in the accompanying statement, which kept the door wide open for a December hike. According to the Fed funds futures, the market assigns a 76% probability for a December hike, while it expects around 2 more through 2019, at a time when the Fed anticipates 3. In our view, this suggests that there is still room for the market to bring its forecasts closer to the Fed’s, and this could be the case if indeed the CPIs accelerate.

On Thursday, Asian time, Australia’s employment data for October are scheduled to be released. The unemployment rate is forecast to have ticked up to 5.1% from 5.0%, but the net change in employment is expected to show that the economy gained 20.3k jobs, more than September’s 5.6k.

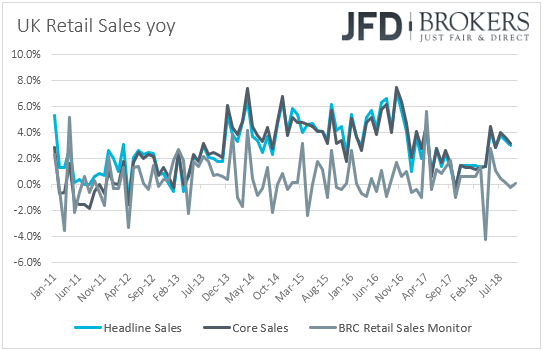

During the European day, we have the UK retail sales for October. Both headline and core sales are expected to have rebounded 0.1% mom and 0.2% mom respectively, after both fell 0.8% in the previous month. Even though this is likely to bring the headline yoy rate down to +2.8% from +3.0%, the core yearly rate is anticipated to have ticked up to +3.3% from +3.2%, something supported by the rebound in the yearly rate of the BRC retail sales monitor for the month. Eurozone’s trade balance for September is also due out, but no forecast is currently available.

Later, we get retail sales data for October from the US as well. Both headline and core sales are anticipated to have accelerated to +0.6% mom and +0.4% mom respectively, from 0.1% in September. The Conference Board consumer confidence index for the month increased, but the UoM consumer sentiment index declined fractionally. So, it’s hard to say to which direction the risks of the retail sales forecasts are tilted to.

Apart from the data, Fed Chairman Jerome Powell is scheduled to speak at an event hosted by the Dallas Fed. Given that there were almost no changes to the statement accompanying last week’s FOMC decision, investors may be eager to find out whether the message they took from the decision was correct. In other words, market participants may look for confirmations that the Committee is indeed planning to hike in December and continue with more rate increases in 2019.

Finally, on Friday, Eurozone’s final CPIs for October are due to be released, but as usual, they are expected to confirm the preliminary estimates.

In the US, industrial and manufacturing production for October are coming out. Industrial production is forecast to have slowed somewhat, to +0.2% mom from +0.3%, but manufacturing output is expected to have accelerated to +0.3% mom from +0.2%.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.