US Treasury yields continued to surge yesterday, while global equity indices were a sea of red, perhaps on fears that the Fed may accelerate the pace of its future rate hikes. As for today, investors are likely to fix their gaze on the US employment report and especially the earnings print. Canada’s jobs data are also due to be released, with a decent report having the potential to further bolster expectations with regards to a BoC rate increase later this month.

Market Participants Turn Attention to US Wage Growth

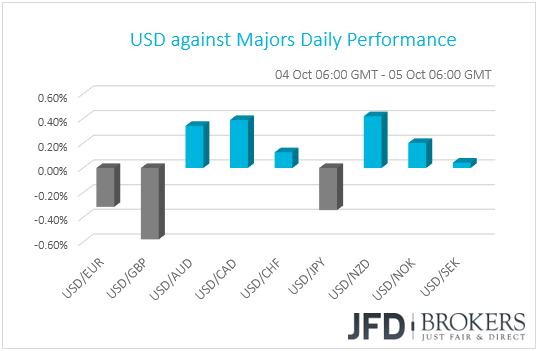

The dollar traded mixed against of its G10 counterparts yesterday. It gained against NZD, CAD, AUD and CHF in that order, while it underperformed versus GBP, JPY and EUR. The greenback traded virtually unchanged against SEK.

US Treasury yields continued to surge yesterday, with the 10-year yield hitting 3.232%, its highest level since May 2011, before retreating somewhat later in the day. The dollar index (DXY) traded flat as a result. Following Wednesday’s upbeat US data and the hawkish remarks by Fed Chair Jerome Powell, it seems that investors remained concerned over the prospect of too aggressive rate increases by the Fed. This was evident by the performance of the equity market as well. Major EU and US indices were a sea of red yesterday, while Japan’s Nikkei closed the Asian session Friday 0.58% down.

As we noted yesterday, higher interest rates mean higher borrowing costs for companies, which could hurt their profitability. Thus, more comments or data suggesting faster Fed hikes may prompt more investors to abandon the equity market and thereby, stock indices could continue correcting lower.

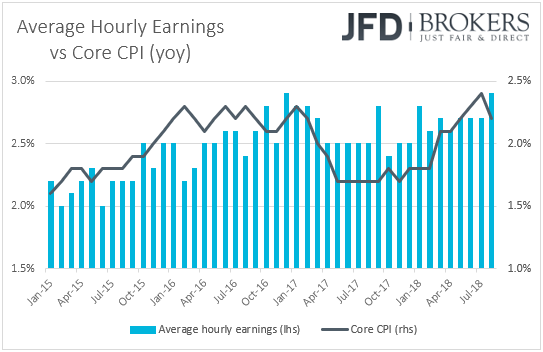

Having said all that, we believe that today, the financial community is likely to fix its gaze on the official US employment data for September. Expectations are for non-farm payrolls to have increased 185k after rising 201k in August. The unemployment rate is expected to have ticked back down to its 18-year low of 3.8%, while average hourly earnings are anticipated to have slowed somewhat on a monthly basis, to +0.3% mom from +0.4%. Barring any revisions to the prior monthly prints, this could drive the yoy rate down to +2.8% from +2.9%, as the September 2017 monthly rate that will drop out of the yearly calculation was +0.5%.

Once again, we believe that most of the attention will fall on the earnings print. That said, even if wages slow somewhat as the forecast suggests, we doubt that this would prove enough to alter market expectations with regards to the Fed’s future plans. According to the Fed funds futures, the market assigns a near 80% chance for a December hike, while it fully prices in 2 more for next year at a time when the Fed’s 2019 median dot points to 3. We believe that a more severe slowdown is needed for market participants to scale back their expectations. In such a case, the dollar and US Treasury yields are likely to slide, while equity indices could rebound.

On the other hand, an upside surprise could raise bets of accelerating inflation in the near future and thereby, prompt investors to bring their rate-path expectations closer to the Fed’s projections. The dollar and Treasury yields could resume their uptrends, while stock indices are likely to continue correcting lower.

EUR/USD – Technical Outlook

Since the reversal on the 26th of September, EUR/USD continued to decline until it found, what it could be, a good potential area of support near the 1.1465 level. Yesterday, we saw the pair retracing strongly back to the upside and placing itself back above the 1.1500 hurdle, which means the there is still some life left in EUR/USD. Even though the pair has been on a downslope recently, our momentum studies indicate that we could see a bit of more correction to upside, before the EUR/USD could slide again, hence we will take a cautiously-bullish stance for now.

A break above the 1.1525 area could open the path for EUR/USD to travel back to territories that were seen in the beginning of this week. The 1.1570 obstacle, marked by Tuesday’s high, could be a short-term stopping point for the bulls to refuel before heading a bit higher. We will keep a close eye on the 1.1595 zone, which was the highest point of this week. Now, if that zone doesn’t hold, this could be a near-term gamechanger for EUR/USD, as more bulls could see this as a good opportunity to step in and lift the pair higher.

As mentioned before, our momentum indicators, the RSI and the MACD, are also somewhat supporting the correction to the upside. The RSI is trying to shift higher, away from its lows near the 25 area, but is currently stuck near 40. The MACD, on the other hand, after showing signs of bottoming, looks quite promising as it has now pushed itself above the trigger line and continues to point higher.

Alternatively, a break below the 1.1505 line, could place us into the “stand by” zone, which means we will have to monitor the pair carefully now. A further decline and a move below this week’s low near the 1.1465 barrier, could trigger some more selling and this could lead EUR/USD towards August levels. Slightly below that breaking point of 1.1465, lies a good potential area of support at 1.1445, marked by the peak of the 17th of August. If the area is not able to withhold the selling pressure, a break below could set the stage for EUR/USD to go and test the 1.1395 level, which held the rate from dropping lower on the 20th of August.

![]()

GBP up on Brexit Optimism, Yen Gains on JGB Yields, CAD Eyes Jobs Data

As for the other currencies, the pound was the main gainer among the G10s following a Reuters report, citing an EU source saying that the UK government’s proposal on the Irish border was “a step in the right direction”. This may have increased hopes that the UK and the EU could eventually find common ground later this year. We stick to our guns that the upcoming summit scheduled for the 18th of October could be the “moment of truth” as EU Chief Negotiator Michel Barnier and the President of the EU Council Donald Tusk recently noted. Even if a deal is not struck at the summit, a notable progress could increase the likelihood for an accord to be finalized in November. On the other hand, the lack of any material steps could revive fears of a disorderly Brexit and thereby, weigh on the British currency.

The yen was also among the gainers, as global stock indices slid and the surge in US Treasury yields caused yields elsewhere to rise as well, with the 10-year yield of JGBs reaching 0.16%, the highest level since the Bank introduced negative interest rates in January 2016. The BoJ refrained from intervening on Thursday to prevent yields from rising more, while an overnight report noted that the Bank will tolerate further increases in long-term yields as long as this does not push 10-year yields well above its 0% target.

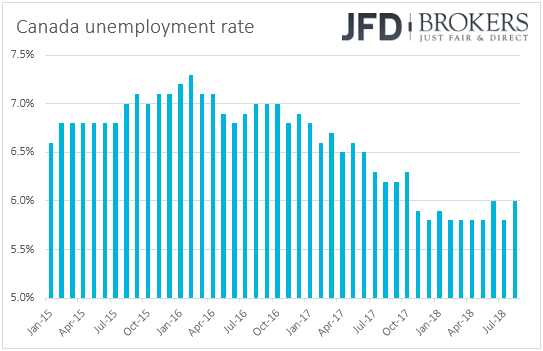

The Loonie underperformed against its neighboring greenback ahead of Canada’s employment report for September, due out today, perhaps driven by the pullback in oil prices. The forecasts have changed and now suggest that Canada’s unemployment rate ticked down to 5.9% from 6.0% in August, while the net change in employment is anticipated to show that the economy gained 25.0k jobs after losing 51.6k the previous month.

Recent data out from Canada showed that the headline CPI rate declined to +2.8% yoy from 3.0%, but the core rate ticked up to +1.7% yoy from +1.6%. Headline retail sales rebounded less than anticipated, but core sales accelerated by more than the forecast suggested. What’s more, last Friday, monthly GDP data showed that the economy grew 0.2% mom in July after stagnating in June. All these keep the door wide open for a rate increase at the BoC’s upcoming gathering, scheduled for the 24th of October, and a decent employment report could further increase that likelihood, especially following the accord between Canada and the US over NAFTA.

CAD/JPY – Technical Outlook

Even though overall, CAD/JPY is trading above the short-term upside support line taken from the low of the 6th of September, still, the pair is showing signs of weakness. Yesterday, CAD/JPY broke through the lower side of the short-term range that it was trading in since the 30th of September and headed south. The pair could continue traveling lower for a bit more until hitting the abovementioned upside line, which could be the area for the bulls to jump in again and take advantage of the lower rate.

A break below the 87.95 level, could send CAD/JPY down towards the 87.45 hurdle, marked by the peak of the 21st of September. Slightly below it, the pair could test the aforementioned short-term upside support line and bounce back off of it. If that’s the case, we could target again the 87.95 obstacle, or even the 88.45 line, which was the lower bound of the aforementioned broken range.

A move back above the 88.45 level would bring the rate back inside the previously talked-about range. The bulls could see this as a good opportunity to increase their exposure and lift CAD/JPY higher, towards the 88.90 obstacle and then potentially to the upper bound of the range.

The RSI and the MACD are showing signs of slowing momentum, which supports the idea of a short-term pullback in CAD/JPY. The RSI is on a downslope and below 50. The MACD doesn’t look like the strongest as well, as it is also on a downslope and below its trigger line.

Alternatively, a break of the aforementioned upside support line and then a close below the 87.55 support line, could lead to a deeper dive down for CAD/JPY, where levels like 86.90 and 86.20 could be met. The later one was marked by the low of the 27th of September.

![]()

As for the Rest of Today’s Events

During the European morning, we get Germany’s factory orders for August and Switzerland’s CPIs for September. Germany’s factory orders are expected to have increased 0.3% mom after declining 0.9% in July, while Switzerland’s CPI rate is anticipated to have ticked down to +1.1% yoy from +1.2%.

Later in the day, apart from the US and Canadian jobs reports, we bet the nations’ trade data for August. The US trade deficit is anticipated to have widened to USD 53.4bn from USD 50.1bn in July. Canada’s deficit is also expected to have widened, to CAD 0.50bn from CAD 0.11bn.

As for the speakers, we have one on today’s agenda: Atlanta Fed President Raphael Bostic.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.