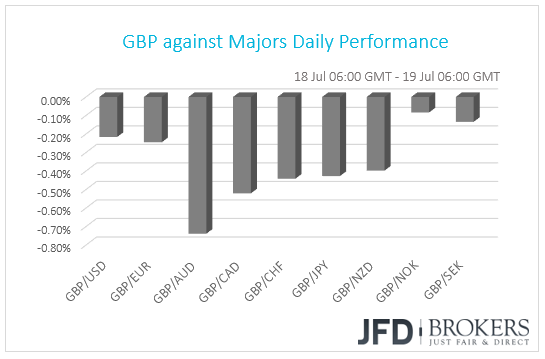

In regards to yesterday’s events, we had another disappointing day from the UK. The inflation numbers that came out missed expectations, which sent the British Pound down against its major counterparts. The YoY core CPI for the month of June came out at +1.9%, which was not only below expectations of +2.2%, but also below the previous +2.1% number. Almost the same happened with headline YoY inflation number for the same period, which came out at +2.4%, the same as the previous, but two tenths of a percent below expectations.

In addition to the CPIs, the UK house price index dropped again. The expectation for the YoY figure to come out at +3.8%, but the actual number was +3.0% only. This also raises concerns over the overall state of the housing market. Even though, the data doesn’t bring a lot of volatility, still it is an important indicator of house prices in UK.

Jerome Powell delivered his second testimony yesterday, followed by a quite positive one on Tuesday. One of the main things to point out that, if on Tuesday, Jerome Powell tried as much as possible to avoid questions regarding trade tensions, in yesterday’s testimony, he was more open to this topic. He warned that protectionism policies could become harmful for the US economy and make it less competitive, and less productive. He also had good things to say about the pace of inflation that was quite good and in line with Fed’s target, and the wage growth was at a “modest to moderate” state.

As for today’s events, we already had the employment figures from Australia that were released during the Asian morning. Generally speaking, the unemployment rate remained the same, the participation rate and the employment change both have increased. The unemployment rate came out as expected at 5.4%, the same as the previous number. The amount of people working or seeking work was at 65.7%, this is just slightly above expectations of 65.5%. The employment change was a huge gainer. When the previous figure was +13.5k and the expectation was +16.7k, the number that came out was +50.9k. All this good news made the Australian currency bounce against its major counterparts.

During the European morning, the UK is due to release their core and headline retail sales figures for the previous month. Even though the headline YoY number is expected to have remained the same as the previous at +3.9%, the core number for the same period is forecast to have declined from +4.4% to +3.7%. The last one is an important measure, as it excludes autos and fuel, due to their more volatile behaviour.

Later on in the day, we will be on the look out for, both initial and continuing jobless claims numbers from the US. The amount of people who started claiming are expected to increase slightly. The figure that measures initial claims is expected to come out at +220k, where the previous was sitting at +214k. But the amount of people that continue claiming income insurance benefits are expected to have fallen a bit, going from the previous +1739k to +1730k expected. Even though, the numbers don’t affect the market that much, still it could be a good gauge of how the US labour market is feeling.

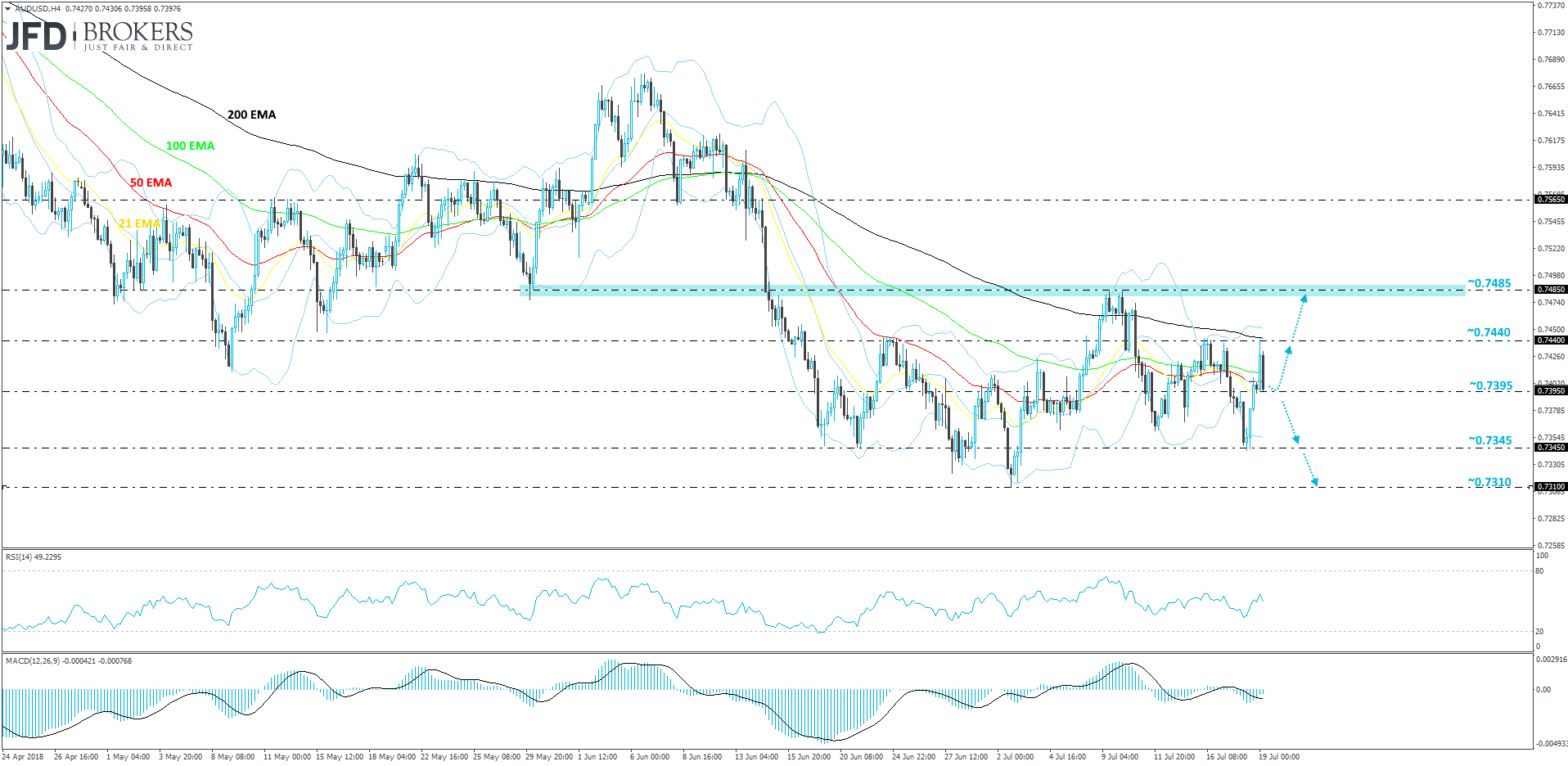

AUD/USD – Technical Outlook

At the moment, we are seeing mixed activity from AUD/USD, where it cannot decide on a longer-term direction. At one point it looks like that the pair is ready to make a run higher, but then it gets held by one of the key resistance levels and reverse back down. It works similarly in the opposite way as well. AUD/USD is stuck between two important levels, 0.7310 and 0.7485. Until the pair continues to trade between them, it could be difficult to understand, which way it wants to move over the longer period of time. For now, we remain neutral, but will seek opportunities between the two levels.

Yesterday, the bears tried to create a sell-off pulled AUD/USD down towards the 0.7345 zone, but the bulls picked up the pace quickly and drove the rate back and closed the day in the green. This morning, when the Australian data came out positive, this gave a boost for the AUD/USD and we saw it hitting the important resistance at 0.7440, from which it retraced back down quickly, wiping out the morning gains. The pair find support around the 0.7395 level. If the move lower continues and we see a break of that level, then we could aim for a test of the 0.7345 zone, marked by yesterday’s low. If that’s not enough to withhold the rate from dropping further, then a test of the 0.7310 level, marked by the 2nd of July low, could be possible.

Alternatively, another push towards the 0.7440 area and eventually a break of it, could interest the bulls in taking AUD/USD towards the key level of resistance at 0.7485, where the rate could stall for a bit, until the bulls and the bears decide on who will take the driver’s seat.

GBP/CAD – Technical Outlook

Finally, the range, that GBP/CAD was sat in since the last days of June, has been broken and the pair moved lower. This creates a more negative atmosphere around the near-term future of GBP/CAD, where we could see further declines lower.

For now, we will remain bearish on the near-term outlook for GBP/CAD. A break below the recently-found support at 1.7200, could initiate another wave of selling and the rate could drop to the next potential area of support at 1.7165. If that level is not able to withhold, this could open the path towards the 1.7085 hurdle. Slightly below that lies the 1.7055 barrier, marked by the lowest point of May.

Certainly, there is a possibility for the pair to correct itself back up a bit, maybe test the 1.7255 level, and then find its way back down again.

On the upside, for us to become slightly bullish, we would need to see a move back above the lower side of the aforementioned range, which is the 1.7300 mark. This way, we could start examining the upside scenario again, where we could initially aim for the 1.7345 zone, and after that for the 1.7445 area, which is around the upper side of the previously mentioned range.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

FX and CFDs are leveraged products. They are not suitable for every investor, as they carry high risk of losing your capital. You should be aware of all the risks associated with trading on margin. Please read the full Risk Disclosure.

Copyright 2018 JFD Brokers Ltd.