After Monday’s tumble, the British pound rebounded and managed to outperform all the other major currencies following headlines that the UK and the EU have eventually struck a draft deal over Brexit. The Loonie was yesterday’s biggest loser, tracking the tumble in oil prices. As for today, we get inflation data from both the UK and the US.

Pound Soars as EU and UK Find Common Ground on Brexit

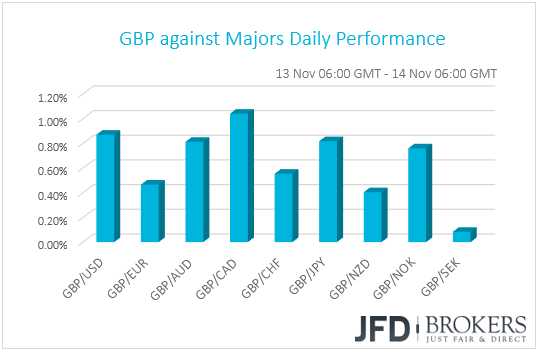

The pound rebounded and managed to outperform all the other G10 currencies. The main losers were CAD, USD and JPY in that order, while the currency that lost the least was SEK.

Once again, it was all about Brexit. After tumbling on Monday, the British currency entered a recovery mode yesterday following headlines that the UK and the EU are close to finding common ground on the divorce terms, and surged even more after the two sides were reported to have eventually struck a draft deal following more than a year of tough negotiations. Prime Minister Theresa May will present the draft text to her Cabinet today, seeking her ministers’ approval, something that could open the door for an EU summit later this month in order to finalize the deal.

This is more-than-welcomed news for GBP-bulls, with the currency having the potential to rise further in case Cabinet agrees on the draft text. That said, we would treat any further recovery in the pound with caution. As we noted yesterday, even if ministers agree on the text and the deal is finalized at an EU summit this month, it would still have to be approved by the Parliament, something that still appears to be a hard task.

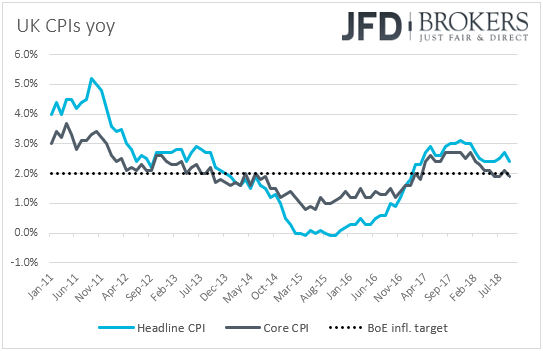

Ahead of the Cabinet meeting, we have the UK inflation data for October. The forecasts suggest that the headline CPI rate accelerated to +2.5% yoy from +2.4%, while the core rate is anticipated to have remained unchanged at +1.9% yoy. Yesterday, the employment data showed that the unemployment rate ticked up to 4.1% from its 43-year low of 4.0%, but average weekly earnings, both including and excluding bonuses, accelerated. Wages including bonuses rose at the fastest pace since Q3 2015, while the ex-bonuses rate was the highest since Q4 2008.

Under normal circumstances, accelerating wages would have encouraged investors to bring further forth their bets with regards to a BoE rate hike. However, judging by the pound’s muted reaction yesterday at the time of the release, this was not the case. Market participants remained on the edge of their seats in anticipation of Brexit developments. With the Cabinet decision over the draft withdrawal deal looming, we believe that this could be the case with the CPIs as well.

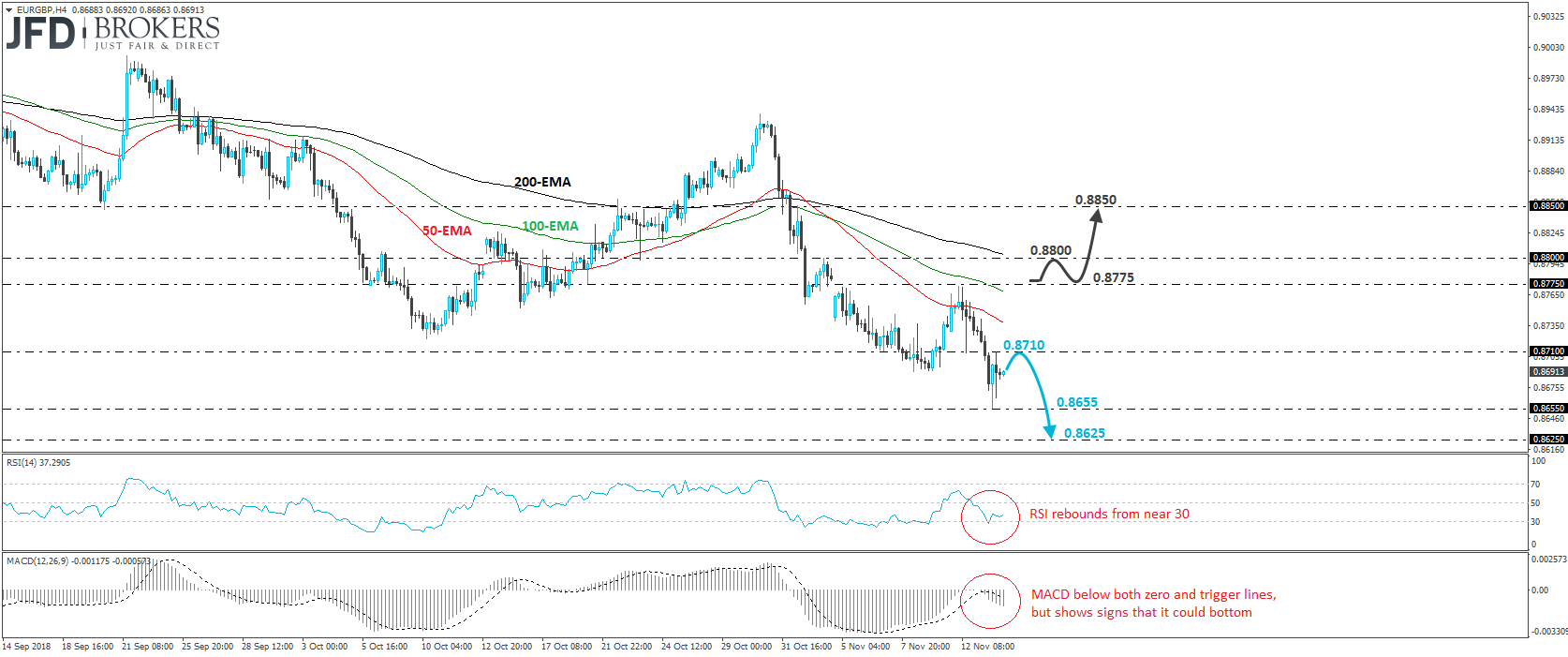

EUR/GBP – Technical Outlook

EUR/GBP slid yesterday to hit support near the 0.8655 zone, before rebounding to find resistance at 0.8710. The price structure on the 4-hour chart remains of lower peaks and lower troughs below all three of our moving averages, and thus, we would consider the near-term outlook to be cautiously negative.

If the bears are willing to take charge again soon, then we may see them driving the rate down for another test near the 0.8655 barrier. A clear dip below that level would confirm a forthcoming lower low and could pave the way for our next support zone of 0.8625, which held the pair from dropping lower from the 13th until the 17th of April.

Shifting attention to our short-term momentum studies, we see that the RSI rebounded from near its 30 line, while the MACD, although below both its zero and trigger lines, shows signs that it could start bottoming. These indicators suggest that the pair may recover a bit more before the bears decide to take the reins again, perhaps for another test near the 0.8710 line.

Now, if the 0.8710 barrier fails to stop any potential recovery, then we will take the sidelines. We would like to see a clear break above 0.8775 before we start assuming that the bulls have gained the upper hand, at least in the short run. Such a break may initially target the 0.8800 zone, defined by the high of the 2nd of November, the break of which could carry more upside extensions, perhaps towards 0.8850, marked by an intraday peak formed on the 1st of the month.

USD-Traders Fix Gaze on US Inflation Data

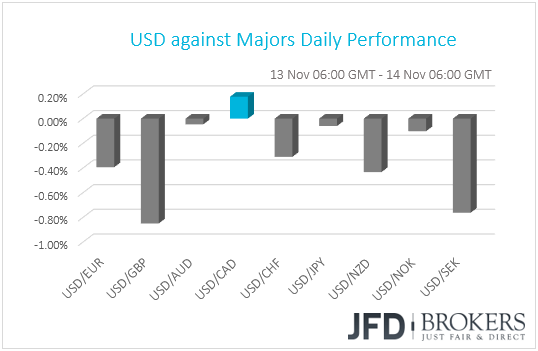

The dollar traded lower against most of the other G10 currencies on Tuesday. It underperformed the most against GBP, SEK, and NZD in that order, while it traded virtually unchanged versus AUD and JPY. The greenback managed to gain only against CAD.

The Loonie was yesterday’s main loser, perhaps tracking the tumble in oil prices. The slide in oil prices accelerated yesterday, with WTI futures suffering their biggest losing day in more than three years. With no clear catalyst behind the tumble, many say that this was an extension of Monday’s slide, which was triggered by Trump’s tweet that Saudi Arabia and OPEC should not cut oil production, with the surge in output and concerns over a global economic slowdown being the main driving force behind the latest downtrend.

Yesterday, in its monthly report, OPEC revised down its forecasts of world oil demand for next year and noted that it expects widening excess supply in 2019. In our view, this amplifies further the need for a production cut by the cartel and its allies. As for today, we get the International Energy Agency (IEA) monthly oil report, as well as the American Petroleum Institute (API) weekly crude oil inventories.

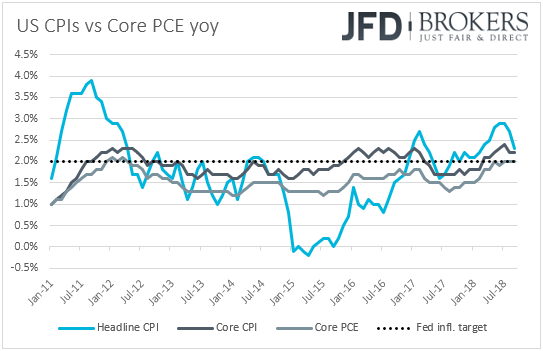

Back to the US dollar, today its traders likely to lock their gaze on the US CPI data for October. Expectations are for the headline CPI to have accelerated to +2.5% yoy from +2.3% in September, while the core rate is forecast to have remained unchanged at +2.2% yoy. On Friday, data showed that the headline PPI for the month accelerated to +2.9% yoy from +2.6%, while the core PPI rate rose to +2.6% yoy from +2.5%. The PPIs support the case for an acceleration in the headline CPI and suggest that the risks surrounding the core forecast may be tilted to the upside.

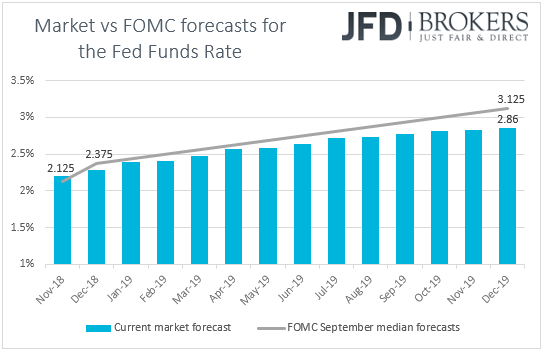

At last week’s gathering, the Fed decided to keep interest rates unchanged within the 2.00-2.25% range as was widely expected, while officials made almost no changes in the accompanying statement, which kept the door wide open for a December hike. According to the Fed funds futures, the market assigns a 78% probability for a rate increase next month, while it expects around 2 more through 2019, at a time when the Fed anticipates 3. In our view, this suggests that there is still room for the market to bring its forecasts closer to the Fed’s, and this could be the case if indeed the CPIs accelerate.

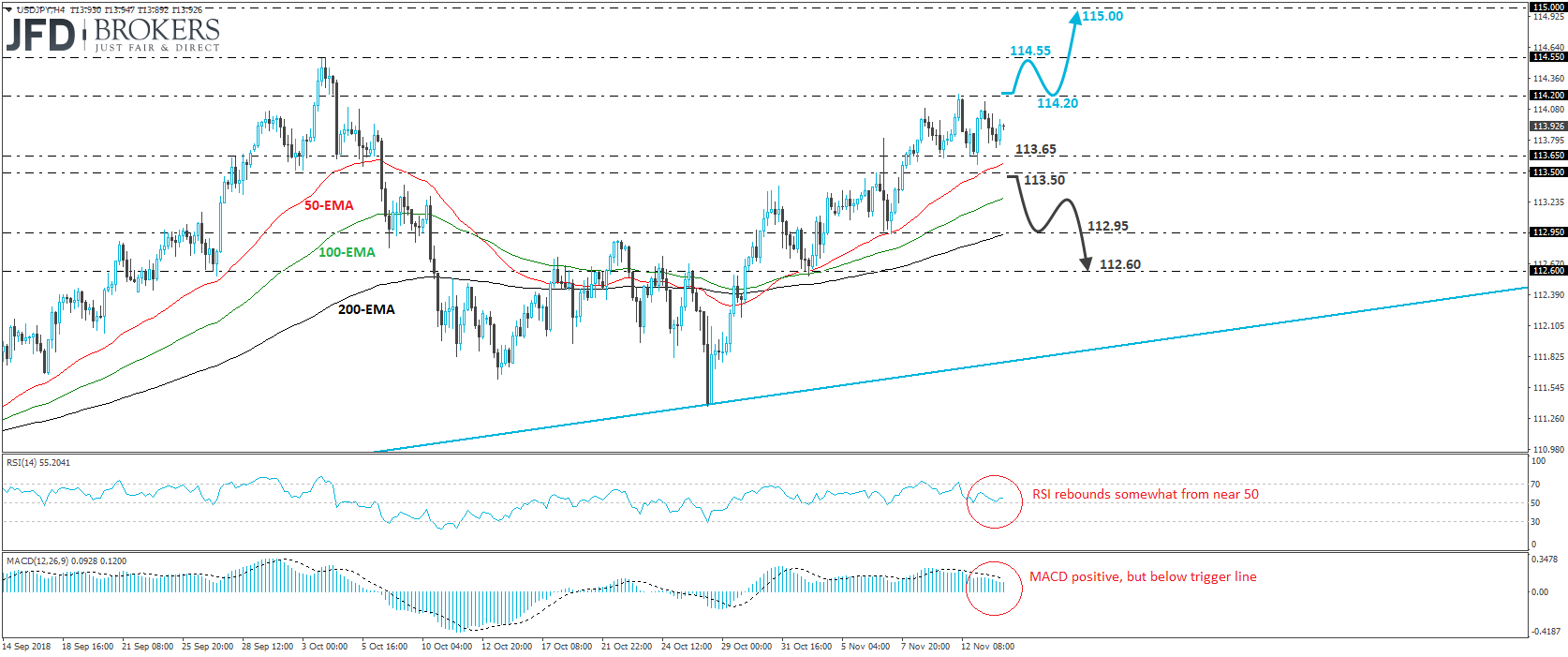

USD/JPY – Technical Outlook

USD/JPY has been trading in a consolidative manner, between 113.65 and 114.20, for almost a week now. That said, the prevailing short-term path appears to be positive, while from a longer-term perspective, the rate continues to trade above the upside support line drawn from the low of the 29th of May. Thus, although we will stay sidelined in the short run and wait for a break out of the aforementioned range, we still see a positive bigger picture.

On the upside, a decisive break above 114.20 would confirm a forthcoming higher high on the 4-hour chart and could signal the continuation of the prevailing short-term uptrend that started on the 26th of October. Such a move could open the path for the peaks of the 3rd and 4th of October, at around 114.55, where another break may see scope for extensions towards the psychological zone of 115.00.

Alternatively, if the bears manage to gain the upper hand and drive the battle below 113.50, this could be seen as a short-term reversal signal. Such a dip could set the stage for the 112.95 barrier, marked by the low of the 7th of November, the break of which may allow the rate to slide towards our next support of 112.60.

The RSI rebounded somewhat from its 50 line, but the MACD although positive, remains below its trigger line and points down. These conflicting momentum signs confirm our choice to stand pat for now and wait for the rate to exit it latest range.

As for the Rest of Today’s Events

During the European day, Sweden’s CPIs for October are coming out. Expectations are for the CPI rate to have ticked up to +2.4% yoy from +2.3%, while the CPIF rate is anticipated to have remained unchanged at +2.5% yoy. That said, we will pay more attention to the core CPIF metric, which excludes energy. In September, the core CPIF rate surged to +1.6% yoy from +1.2%, but at its latest meeting, the world’s oldest central bank repeated that interest rates will be raised either in December or February, which may have come as a disappointment to those who raised bets that the Bank will dismiss the February option. Thus, it would be interesting to see whether the core CPIF will accelerate further, something that could revive hopes that December could be the most likely candidate for the Bank to act, or whether it will retreat again, pushing expectations to February.

In the Eurozone, Germany’s preliminary GDP for Q3, as well as the 2nd estimate of the bloc’s growth rate are coming out. Germany’s numbers are expected to show that the economy contracted 0.3% after growing 0.5% the previous quarter, while the 2nd estimate of the Eurozone as a whole is expected to confirm the preliminary figure, namely that the Euro-area has slowed to 0.2% qoq from +0.4%. Eurozone’s employment change for Q3 and industrial production for September are also due to be released. The employment change is forecast to have slowed in both quarterly and yearly terms, while industrial production for September is anticipated to have declined 0.4% mom after rising 1.0% in August.

At the latest ECB policy meeting, President Draghi maintained his fairly optimistic stance with regards to Euro area’s economic outlook, but the data keeps amplifying concerns over the bloc’s economic performance. The next ECB meeting is scheduled of the 13th of December, and if data continues coming on the soft side, it would be interesting to see whether Draghi would still consider the risks surrounding the Euro-area growth outlook as broadly balanced.

As for tonight, during the Asian morning Thursday, Australia’s employment data for October are scheduled to be released. The unemployment rate is forecast to have ticked up to 5.1% from 5.0%, but the net change in employment is expected to show that the economy gained 20.3k jobs, more than September’s 5.6k.

We also have four speakers on the agenda: During the US session, Fed Board Governor Randal Quarles steps up to the rostrum, while tonight, during the Asian day, we will get to hear from Fed Chair Jerome Powell, San Francisco Fed President Mary Daly, and RBA Assistant Governor Guy Debelle.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.