The dollar traded on the back foot against most of the other G10 currencies on Monday, with the yen being among the currencies which failed to gain ground even after US President Trump officially announced tariffs on USD 200bn Chinese imports. As for tonight, the BoJ concludes its policy meeting, but we don’t expect the decision to reveal any major changes.

US Imposes 10% Tariffs on USD 200bn Chinese Imports

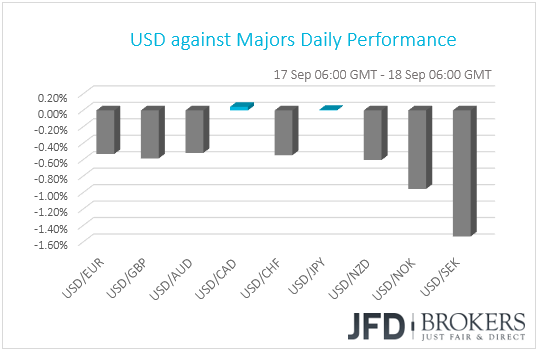

The dollar traded lower yesterday against all but two of the other G10 currencies. It underperformed the most against SEK, NOK and NZD, while it traded virtually unchanged against CAD and JPY.

A few hours after the US close, US President Donald Trump officially announced that he will proceed with the new round of tariffs on USD 200bn worth of Chinese goods at a 10% rate. According to a senior administration official, the duties will go into effect on the 24th of September, but the rate will increase to 25% by the end of the year. What’s more, the US President also noted that if China retaliates against US farmers or industries, he will proceed with more tariffs on approximately USD 267bn Chinese imports.

Last week, the US invited China back to the negotiating table, a move that was welcomed by the world’s second largest economy, as well as by investors, who switched their trading to risk on. That said, things took a 180-degree spin again on Friday, following reports that the US would eventually proceed with the aforementioned tariffs as early as Monday. China replied that it may not participated in trade talks if the US goes ahead with the duties, which took any hopes that the dispute could be resolved through talks back to square one.

Back to the dollar, it may have remained on the back foot because yesterday’s move was already flagged on Friday. After all, the currency strengthened due to safe-haven inflows on Friday’s reports. The yen was among the two currencies that failed to gain against their US counterpart, also suggesting that market participants were not caught off guard. This is evident by the performance of the Asian equity markets too. Both Japan’s Nikkei 225 and China’s Shanghai Composite indices finished their sessions in the green, up 1.44% and 1.82% respectively.

Now the ball is back to China’s court. Last month, the nation unveiled a list of USD 60bn worth of US goods that will be tariffed if Washington proceeds with the levies on the USD 200bn worth of Chinese imports. However, given that China cannot respond with duties on equal amount of goods, it could also restrict exports to US manufacturing supply chains, according to a former Chinese finance minister.

Further escalation in trade tensions between the world’s two largest economies could hurt again market sentiment, prompting investors to abandon risky assets and seek shelter in safe havens. Nevertheless, given that investors have been digesting the idea of a full-blown trade war between China and the US, we believe that moving forward, any new announcements may continue to have diminishing effects. After all, market participants are aware that China wants to retaliate and that the US is planning to hit back with more.

Nikkei 225 – Technical Outlook

After breaking the key resistance of 23050 and rushing higher, the Nikkei 225 corrected itself back down, where it changed that resistance level into a good support, from which the index bounced up again. For now, we remain positive over the near-term outlook on the Nikkei 225.

At the time of the analysis, Nikkei is sitting slightly below its next good area of resistance at 23500, marked by the high of the 1st of February. If the Japanese index makes a run for it and closes above that 23500 level, this could invite more bulls into the action and we could see Nikkei traveling higher to the 23790 zone, which was the peak of the 29th of January. If that zone is not able to withhold the price from rising further, we could see the index moving all the way towards the 24189 area, marked by the high of the 23rd of January.

Looking at our oscillators, the RSI has moved higher from its 50 line and is still pointing to the upside, supporting the upside scenario. The MACD is also in support of some potential higher moves, as it is above both its zero and trigger lines, pointing up as well.

Alternatively, a strong reversal back below the 23050 support level could interest the bears to jump in again and drive Nikkei towards the 22850 obstacle, marked near the high of the 3rd of September. If that area is not able to stop the bears, they could then easily drive the Japanese index lower, to the 22620 level, which held the price from dropping lower on the 13th of September. If the bears still remain in the driver’s seat, then a drop below 22620 could set the stage for a test of the upwards moving trendline taken from the low of the 23rd of March. That line could stop the fall for a while.

![]()

Bank of Japan Decides on Monetary Policy

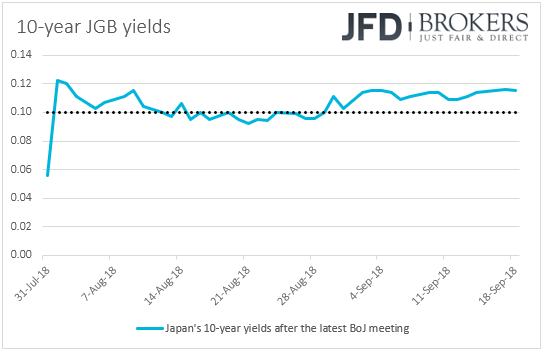

Tonight, during the Asian morning Wednesday, the Bank of Japan concludes its two-day policy meeting. When they last met, back in July, Japanese policymakers kept their short-term policy rate unchanged at -0.1% and repeated that they will purchase Japanese government bonds (JGBs) so that 10-year yields will remain at around 0%. However, they announced some minor tweaks including more flexibility in bond operations, as well as the introduction of forward guidance for policy rates. What’s more, at the press conference following the decision, Governor Kuroda announced that the Bank will allow yields to fluctuate within a ±0.2% range.

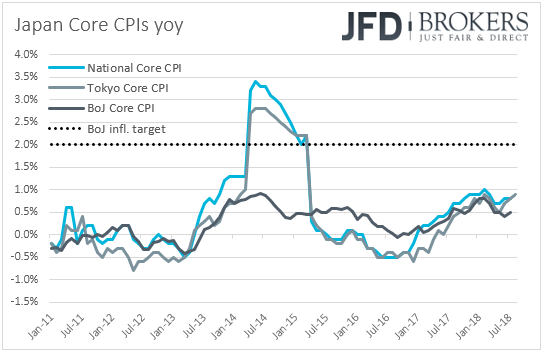

Since then, Japan’s 10-year yields failed to move well above the 0.1% mark, and thus investors may be on the lookout for any clues whether the Bank could act again soon to boost trading. That said, with many officials attributing this to the summer-holiday season, we don’t expect any remarks on that front. We think that officials may prefer to wait for longer before evaluating the impact of their tweaks. What’s more, with all Japanese inflation metrics well below the Bank’s objective of 2%, we see it hard for policymakers proceeding with further changes so soon.

USD/JPY - Technical Outlook

Overall, USD/JPY continues slowly to grind higher, perhaps aiming for the levels seen in July. Yesterday’s bearish move did not spook the bulls, as they saw it as a good opportunity to jump in and lift USD/JPY back up. From the very short-term perspective, the pair is now trading within a 50-pip tight range, between the 111.65 and 112.15 levels. However, the price structure has been higher peaks and higher troughs since the 7th of September and thus, for now, we will remain somewhat bullish and aim for higher levels.

A break through the 112.15 resistance could open a new horizon of levels for USD/JPY. The first good potential area of resistance could be seen near the 112.65 line, which was not far from the peak of the 20th of July and also an intraday inside swing low during the 19th of the month. Initially, this is where the rate could stall for a bit, but if the bulls remain in the driver’s seat, then further acceleration of USD/JPY could open the path towards the 113.15 zone, marked near the highest point of July this year.

On the other hand, in order to start examining the downside potential, we would need to get a close below the 111.65 hurdle, which could invite more bears to the table and lead the pair down to the 111.35 barrier, marked by the low of the 13th of September. If the yen-buying continues, we could then see a further slide towards the 111.10 level, which acted as a good bouncing ground for the pair on the 12th of September.

![]()

As for Today’s Events

Today, the calendar appears relatively light. The only economic indicators worth mentioning are Canada’s manufacturing sales for July and New Zealand’s Global Dairy Trade Price Index.

As for the speakers, we have one on today’s agenda: ECB President Mario Draghi.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.