Risk appetite was boosted yesterday after US President Trump and European Commission President Juncker agreed to work towards zero tariffs. As for today, the main event is likely to be the ECB policy meeting. With no change in policy expected, investors may be looking for more clarification on the Bank’s interest rate guidance.

Trump-Juncker Meeting Boosts Risk Appetite

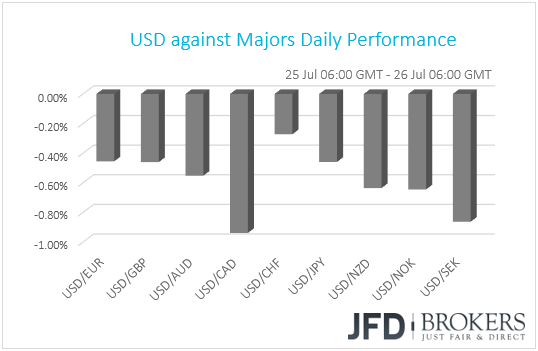

The US dollar traded lower against all the other G10 currencies on Wednesday. It lost the most against CAD, SEK and NOK, while it underperformed the least against the safe-haven CHF.

Yesterday, the main event for the financial community was the Trump-Juncker meeting in Washington. The dollar and the safe-havens CHF and JPY came under selling interest, while riskier assets, like commodity-linked currencies and equities, gained following a report citing a European official saying that President Donald Trump secured concessions from the EU to avoid a trade war. The report was confirmed soon thereafter when Trump and Juncker said they agreed to “work together towards zero tariffs, zero non-tariff barriers, and zero subsidies on non-auto industrial goods”.

Ahead of the meeting, European stock indices closed in the red, perhaps on fears that the meeting may not bear fruit. Euro Stoxx 50, the German DAX, and UK’s FTSE 100 were all down 0.53%, 0.87% and 0.66% respectively. However, the positive outcome boosted market sentiment, with the US indices ending their session in positive territory. The S&P 500 gained 0.91%, the Dow was up 0.68% and Nasdaq 100 closed 1.17% above its opening.

Now back to the dollar, it may have come under selling interest given that during periods of market turbulence and uncertainty, it was sometimes bought as a safe haven. Thus, it may have been sold after the Trump-Juncker meeting proved positive for market sentiment. That said, we don’t see any developments pointing to easing trade tensions as negative for the US currency. On the contrary, easing trade tensions could bring down the chances of retaliatory measures by US’s trading partners and thereby reduce the risks for the US economy to get hurt. This will also give more confidence to the Fed to continue hiking rates in the foreseeable future.

As for the yen, it remained somewhat stronger than the other safe-haven, the Swiss Franc. The reason may have been the rise in the 10-year Japanese Government Bond yields. The yields have been on a surging mode since we had reports that the Bank of Japan is discussing possible changes to its monetary policy. As we noted on Tuesday though, with all the nation’s inflation metrics well below the Bank’s 2% objective, it’s hard for us to imagine the Bank taking a step towards normalization, at least at its upcoming gathering scheduled for next week.

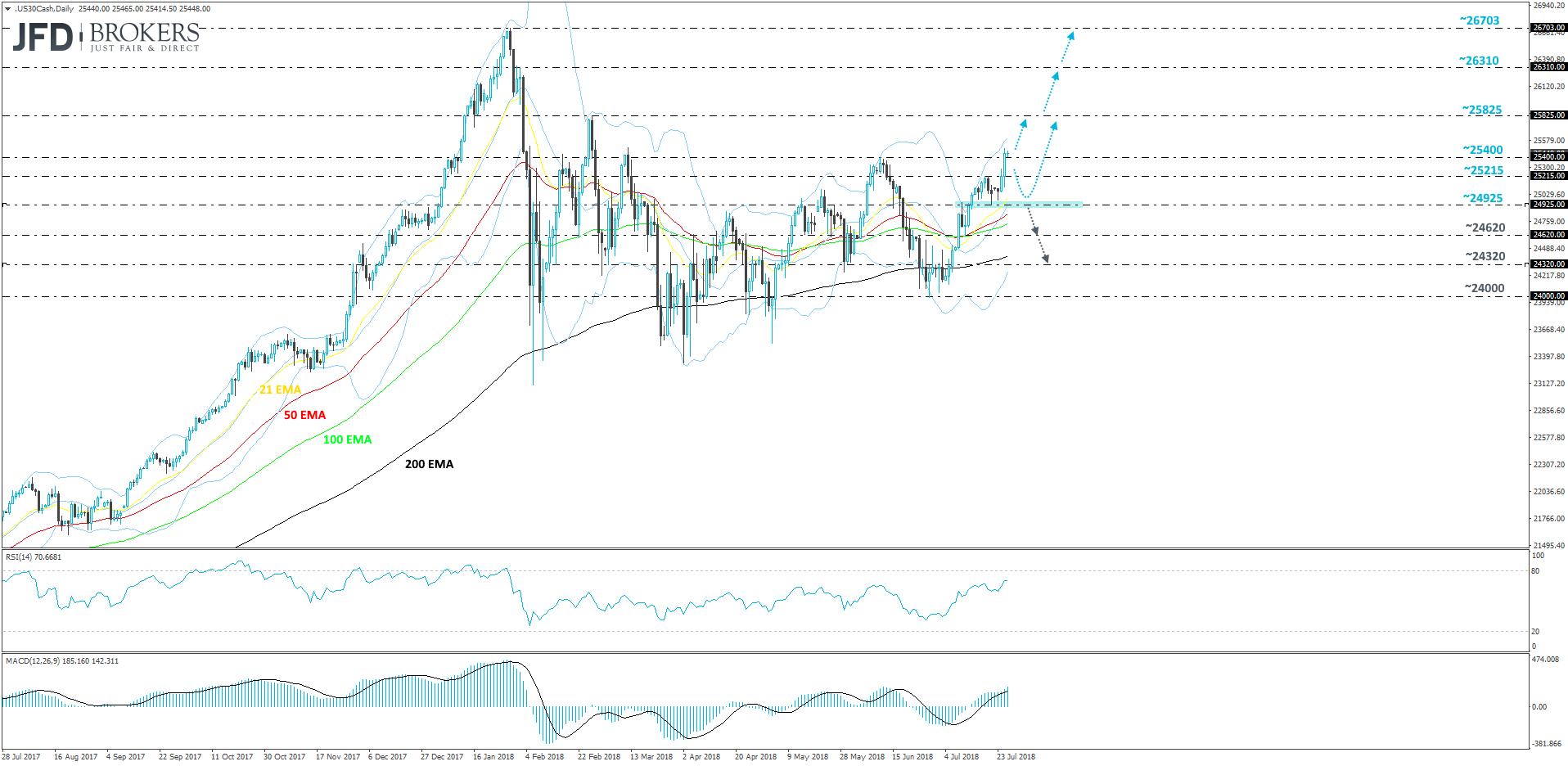

DJIA – Technical Outlook

The Dow has recently shown some good performance, as it moved back up again from the lows seen during the first week of July. At one point there, the index hit the 24000 hurdle, from which it reversed to the upside and still continues to move in that direction. For now, we remain positive on the near-term outlook and we could see the Dow climbing higher.

Yesterday, the index broke one of its key resistance levels, the 25400 barrier, which was last seen on the 11th of June. This move potentially opens the path to higher areas of resistance like the 25825 one, marked by the peak of the 26th of February. If this area is not able to withhold, the DJIA could then try and make its way towards the 26310 zone, or even back up to its all-time high at the 26703 level.

Certainly, there is a possibility for the index to move a bit lower, in order to find a good bouncing ground, where the bulls could jump in again and drive it to the previously mentioned levels. Good potential areas of support to keep an eye on could be the 25215 or the 24925 areas.

The RSI and the MACD are currently both in support of the upside scenario. The RSI, even though it flattened slightly, is still above 50 and seems to be trying to push a bit more to the upside. The MACD is above its zero line and also above the trigger line, which also adds a positive twist on the overall outlook.

For us to become comfortable with the downside scenario, we would need to see a move and a close below the 24925 area. This is where more bears could see this as an opportunity to jump in and drive the index lower towards the next potential area of support around the 24620 level, marked by the low of the 10th of July. If that area is not able to prevent the Dow from falling further, then this could open the door towards the next potential support zone near the 24320, which was the inside swing area seen around the end of June and the beginning of July.

EUR-Traders Lock Gaze on ECB Policy Decision

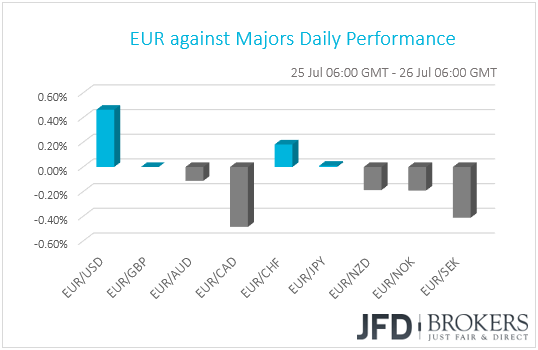

The euro traded lower against the majority of its G10 counterparts. It underperformed the most against CAD, while it gained only against USD and CHF. The common currency traded virtually unchanged against GBP and JPY.

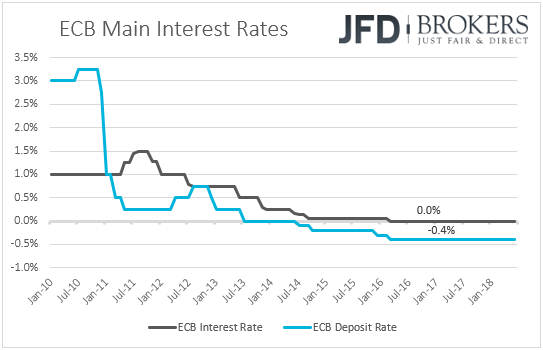

Today, euro traders are likely to be sitting on the edge of their seats in anticipation of the ECB monetary policy decision. When they last met, ECB officials signaled a QE-tapering after September and a clear end to the program in December, but the decision was subject to incoming data. What’s more, the Bank noted that interest rates are expected to stay untouched “at least through the summer of 2019 and in any case for as long as necessary”, which came as a disappointment to those expecting a hike in mid-2019, and thus the euro sold off.

In our view, the interest rate guidance meant that rates are likely to start rising in September 2019 the earliest. However, following that meeting, a report citing sources familiar with ECB discussion noted that officials are split over when they may hike rates. According to the report, some said that July should not be ruled out, while others suggested that they should wait until autumn. So, having that in mind, although the Bank is unlikely to proceed with any further changes so early, investors will be hanging from President Draghi’s words at the press conference for further clarification on the interest rate guidance.

As for our opinion, we don’t expect the President to provide any clearer hints. At the latest conference, he noted that “Through the summer is intentionally not precise”. “There is a desire to maintain optionality in each and every part of this decision”, the President added. What’s more, the minutes of that meeting showed that policymakers were unanimous to support the policy proposals, which came in contrast with the aforementioned reports over a split Governing Council. We believe that Draghi will refrain from commenting on specific months as the Bank would prefer to maintain flexibility on its future decisions, in case things fall out of orbit.

Another topic investors are likely to pay attention to is trade. In his introductory statement following the previous meeting, Draghi noted that the risks surrounding Eurozone’s economic outlook remain broadly balanced, but uncertainties related to global factors, including the threat of increased protectionism, have become more prominent. Although the composite PMI declined somewhat in June, we believe that Draghi’s view may be that very little changed since the June meeting. When asked at the prior conference, he said that it is important to know that the Bank’s projections only contain the effects on trade measures that have been implemented already and not of those that have not yet. Following the aluminum and steel tariffs in May, the US did not proceed with new measures against the EU. It only threatened on auto tariffs. This, combined with the positive outcome of the Trump-Juncker meeting, could give ample room for the President to strike a balanced tone once again.

As for the euro, we don’t expect a massive reaction. It could come under selling interest if Draghi disappoints those who wait for clues as to whether July 2019 is a possible candidate for a rate increase, but such loses are likely to remain limited if he continues to see the risks around the Euro area growth outlook as broadly balanced.

EUR/USD – Technical Outlook

EUR/USD continues to trade within a wider range between the 1.1510 and 1.1840 levels. Until we see a clear move out of the range, we will remain neutral with regards to the near-term outlook. Today’s ECB meeting, and especially Mario Draghi’s press conference, could prove a source for volatility in the common currency, but unless we get an exit of the range, we will stick to our guns that the near-term picture is flat for now.

EUR/USD s currently sitting below a resistance line of 1.1745, which held the pair from moving higher on the 17th and 23rd of July. But if we see a break of it, then we could see the pair moving a bit higher towards its next area of resistance at the 1.1790 level. A break above could clear the path to 1.1840, which is acting as the upper bound of the aforementioned range. If EUR/USD finally decides to break that area, then this could be a signal for more bulls to join the buying action and drive the pair higher. The potential resistance zone to watch there could be the psychological 1.2000 barrier, marked by the high of the 14th of May.

On the other hand, if EUR/USD decides to move lower and breaks the 1.1655 hurdle, then it could eventually travel down to the 1.1575 area, or even to test the lower bound of the previously mentioned range, at 1.1510. But, if the lower side of that range gets finally broken, this could open the path towards lower levels like the 1.1435, or even the 1.1370, marked by the low of the 13th of July.

As for the Rest of Today’s Events

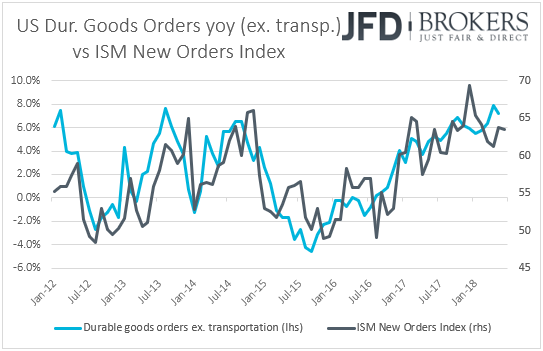

In the US, we get durable goods orders for June. Expectations are for headline orders to have risen 3.0% mom after falling 0.4% in May. However, something like that is likely to drive the yoy headline rate lower as the June 2017 monthly print that will drop out of the yearly calculation was 6.4%. As for orders excluding transportation, they are expected to have risen 0.5% mom after stagnating the previous month, which would drive the yoy up. Having said that though, bearing in mind that the New Orders sub-index of the ISM manufacturing PMI for June slid fractionally, to 63.5 from 63.7, we view the risks surrounding the core forecast as tilted somewhat to the downside.

Initial jobless claims for the week ended on the 20th of July are also coming out and expectations are for an increase to 215k from 207k the previous week, something that will push the 4-wk moving average a tick down to 220.4k from 220.5k.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

FX and CFDs are leveraged products. They are not suitable for every investor, as they carry high risk of losing your capital. You should be aware of all the risks associated with trading on margin. Please read the full Risk Disclosure.