The current trading week features a dense set of macroeconomic releases that will help shape market expectations for 2026. Following several Federal Reserve rate cuts, the debate has shifted away from whether policy will ease further toward how much room remains for additional accommodation.

US Inflation: CPI and PPI as Directional Signals

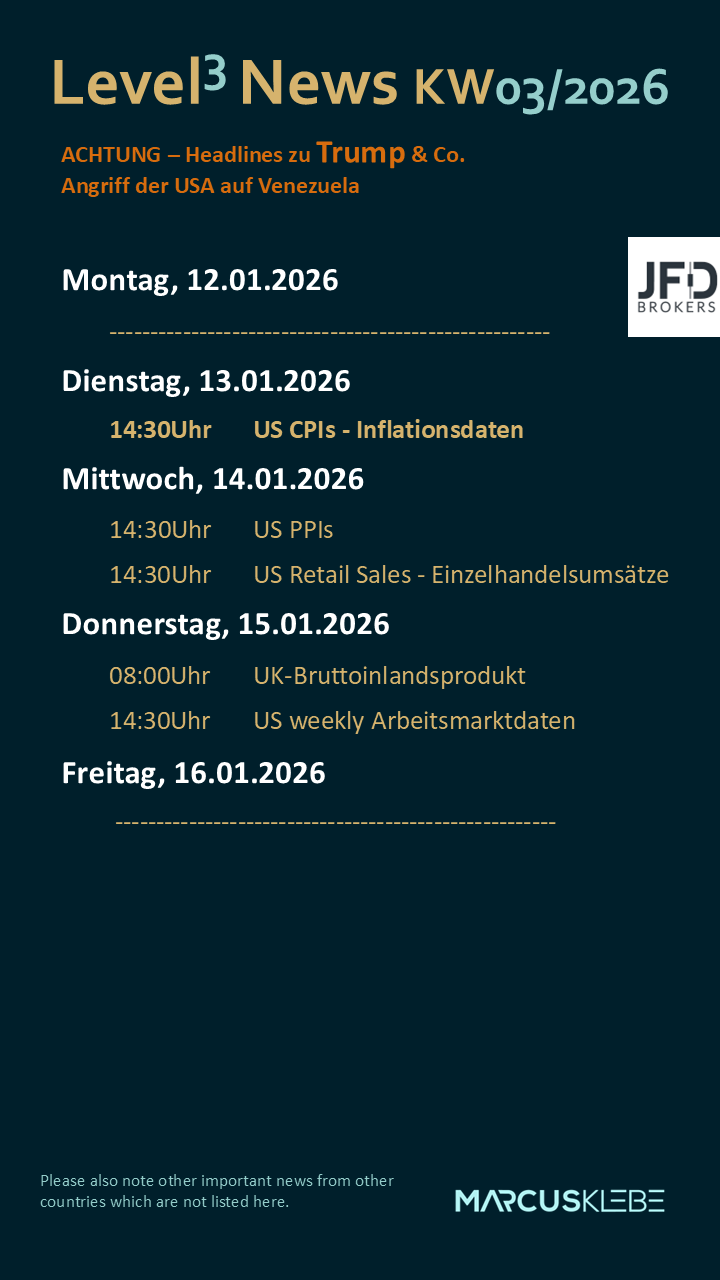

US consumer price data (CPI) remain the primary reference point for markets. The recent disinflationary trend has largely held, and the key question now is whether this trend continues or begins to stabilize—particularly in core inflation and services.

Producer prices (PPI) provide an important complementary signal, offering insight into cost pressures at the corporate level. Muted PPI readings would reinforce the view that inflation risks in 2026 remain contained.

Retail Sales: Testing the Resilience of US Consumers

US retail sales will offer a timely snapshot of consumer strength in an environment where financing conditions remain relatively tight. Solid figures support near-term growth but could temper expectations for further Fed easing. Weaker data, by contrast, would strengthen the case for additional rate cuts, albeit at the cost of renewed growth concerns.

Labor Market: Monitoring the Margins

Weekly initial jobless claims continue to serve as a high-frequency gauge of labor market momentum. After a clear cooling toward the end of last year, markets are now watching for confirmation that this trend is either stabilizing or extending. For the Fed, sustained labor market softening remains an important factor in keeping inflation pressures in check.

UK GDP: A Barometer for Developed-Market Growth

UK GDP data provide a useful external reference for growth dynamics outside the US. The UK economy tends to react more quickly to tighter monetary conditions. Weak GDP figures would increase pressure on the Bank of England and could amplify global growth concerns, with potential spillovers into risk assets and FX markets.

Market Takeaway

This week is less about any single data point and more about the broader narrative:

-

Easing inflation alongside moderate consumption supports further policy accommodation

-

Unexpectedly strong data could push back easing expectations

-

Weak UK growth data would reinforce global slowdown concerns

Bottom Line

The upcoming releases will help determine whether the current market environment—defined by ongoing rate cuts but rising growth uncertainty—remains intact. For markets, context and consistency matter more than individual headlines.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

There are risks involved with trading of cash equities. Past performance is not indicative of future results. You should consider whether you can tolerate such losses before trading. Please read the full Risk Disclosure (https://www.jfdbrokers.com/en/legal/risk-disclosure).

Copyright 2024 JFD Group Ltd.