Risk appetite was subdued yesterday, perhaps due to the weak GDP data from China. In the FX sphere, the pound was among the main gainers as UK PM Theresa May promised to be “more flexible” with Parliament over Brexit. As for tonight, the BoJ decides on monetary policy, while a few hours earlier, we get New Zealand’s inflation data for Q4.

Risk Appetite Eases, GBP Gains as May Promises Flexibility

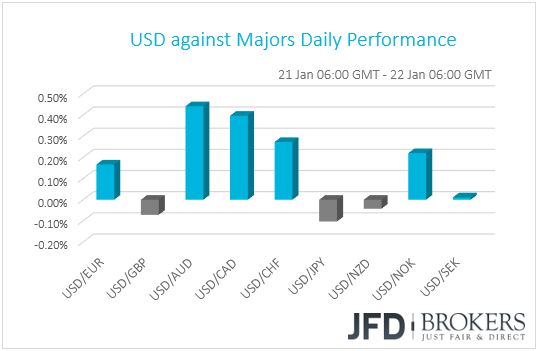

The dollar traded higher against most of the other G10 currencies yesterday. It slightly underperformed against JPY and GBP, while it traded virtually unchanged against NZD and SEK. The main losers were AUD, CAD and CHF.

Although not so clear by the performance in the FX market, equities suggest that risk appetite softened yesterday following Friday’s strong boost. Most EU indices closed their sessions in the red, with the subdued sentiment rolling into the Asian morning Tuesday. Japan’s Nikkei 225 and China’s Shanghai Composite closed 0.47% and 1.18% down respectively. US markets stayed closed yesterday in celebration of the Martin Luther King Jr. Day.

On Friday, investors’ morale was fueled by reports that China is considering raising its annual imports from the US by a combined amount of USD 1 trillion in order to bring its trade surplus to zero by 2024. That said, markets traded on a softer note on Monday, perhaps following headlines that the US Treasury saw little progress made in the US-China talks with regards to intellectual property, as well as China’s GDP data, which showed that in Q4, the world’s second largest economy grew at the slowest pace since the global financial crisis. The downside revision in IMF’s forecasts for global growth did not help either.

Moving forward, focus is likely to turn to the 30th and the 31st of January, when China’s Vice Premier Liu He will travel to the US to hold talks with Treasury Secretary Steven Mnuchin and Trade Representative Robert Lighthizer. As we noted on Friday, any signs of progress may revive hopes with regards to a final accord before the 1st of March, when the 90-day deadline expires, and thereby equities and the risk-linked currencies are likely to gain again. At the same time, safe havens like the yen could come under pressure. On the other hand, anything suggesting that the two sides still have a long way to go before finding common ground, like Monday’s report on intellectual property, may weigh on risk appetite.

Back to the currencies, the pound was the second-best performing currency yesterday, just behind the Japanese yen. The main event for pound traders was May’s presentation of her alternative Brexit plan before the Parliament, which gave us little new information on how the PM intends to move forward. May just proposed to seek further concessions from the EU over the thorny issue of the Irish border and promised to be “more flexible” with MPs in future talks over how the nation will depart from the EU. She did not offer a clear roadmap on how she will deal with the Irish backstop, neither she ruled out a no-deal outcome.

Sterling gained, probably on May’s “more flexible” remarks, but GBP-bulls were reluctant to add to their positions, perhaps as she did not rule out a no-deal Brexit. “No-deal will only be taken off the table by either revoking Article 50, which turns back the results of the referendum - the government will not do that - or by having a deal, and that is what we are trying to work out”, she said.

As for our view, we still see a broadly agreed solution by the end of March as a hard task. Even if May’s flexibility leads to a plan that could gain majority in Parliament, she may not find the EU on the same page. Remember that EU officials have repeatedly noted that they don’t want to deviate much from what was already agreed with May. Thus, the next inline option in order to avoid a disorderly withdrawal maybe extending Article 50.

GBP/USD – Technical Outlook

GBP/USD continues to trade above its steep upside support line drawn from the low of the 2nd of January, which still puts a positive spin on the short-term outlook. But because the pair is trading a bit further away from that line, before another push higher, GBP/USD could retrace back down to test that short-term upside support line. That said, given that on a four-hour timeframe the pair has created a lower high, we will take somewhat a cautiously-bullish approach for now.

A drop below the 1.2850 obstacle, could lead GBP/USD towards a re-test of the aforementioned upside line. If the bears fail to drive the rate below it, then we may see the pair rebounding, as the bulls might re-enter the field. We will then target the 1.2850 obstacle again, this time from underneath, a break of which could push the rate further up. The next potential area of resistance may be seen near the 1.2912 hurdle, marked by yesterday’s high. If that level fails to keep the pair down, its break could open the door to the psychological 1.3000 zone, where GBP/USD got held last week.

Alternatively, a break of the aforementioned upside line and a drop below the 1.2805 level, could lead GBP/USD towards the next good area of support, around the 1.2775 level. But that level may only be seen as a temporary pit-stop for the bears to refuel and drive the pair further down. If the rate does move below that level, then we could start looking at the 1.2705 barrier as the other good support zone, where the rate may get a hold up.

![]()

BoJ Takes the Central Bank Torch, New Zealand CPIs in Focus as Well

Tonight, during the Asian morning Wednesday, the BoJ decides on interest rates for the first time in 2019. At their last meeting for 2018, Japanese policymakers kept their ultra-loose policy unchanged as was broadly anticipated, and despite the disappointing GDP data for Q3, the Bank reiterated that Japan’s economy is expanding moderately and that it will continue to do so.

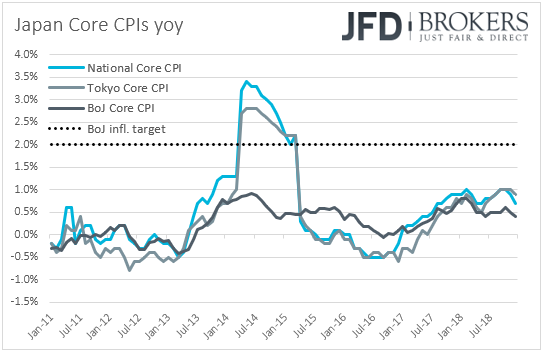

Latest inflation data showed that consumer prices slowed in both headline and core terms, with the headline rate tumbling to +0.3% yoy in December, and the core one sliding to +0.7% yoy from +0.9%.

For this meeting, we expect them to maintain short-term interest rates at -0.1% and the target of 10-year JGB yields around 0%. Thus, the attention is likely to fall to the accompanying statement, the updated economic projections, and the press conference held by Governor Kuroda thereafter. We believe that officials may reiterate that the economy is expanding moderately, but taking into account the latest CPI prints, we see the case for another downside revision to the inflation forecasts.

As for the yen, it could weaken somewhat in case the Bank decides to revise down its inflation projections, but we expect its reaction to be limited and short-lived. We believe that the Japanese currency is likely to remain more sensitive to developments surrounding the broader risk sentiment, and especially headlines regarding the US-China trade sequel.

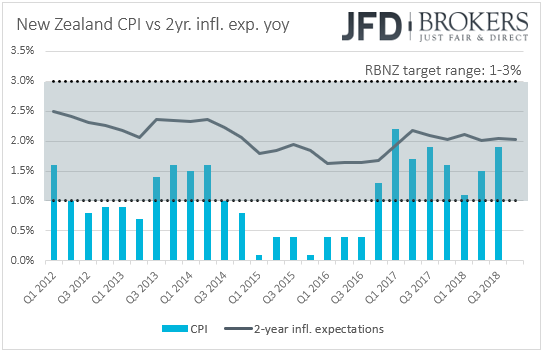

A few hours ahead of the BoJ decision, we have inflation data for Q4 from New Zealand. Expectations are for a slowdown to +0.7% qoq from +0.9%. However, this could still drive the yoy rate up as the quarterly print of Q4 2017 that will drop out of the yearly calculation was +0.1% qoq.

Although Governor Orr removed from the previous statement the part saying that the next move could be up or down, at the press conference he said that he would still consider a cut if GDP falls short of the Bank’s projections. Since then, GDP data showed that the economy slowed to +0.3% qoq in Q3 from +1.0% in Q2, which dragged the yoy rate down to 2.6% from 3.2%. Officials may not be tempted to cut rates when they meet next, as they may prefer to wait for more evidence as to whether this slowdown was temporary or not, but we don’t expect a possible rise in the inflation rate to encourage a hawkish shift either.

NZD/JPY – Technical Outlook

NZD/JPY is now retracing slightly back down, but one should remain cautious, as the pair still remains above its short-term upside support line taken from the low of the 8th of January. If that line continues to provide strong support for the rate, we may see the bulls coming back into the action and pushing the rate back up again. That said, later on, the upside could be limited, due to the short-term tentative downside resistance line drawn from the highest point of December 2018.

As mentioned above, a re-test of and a rejection from the aforementioned short-term upside support line could spark some hope in the eyes of the bulls, as it could give them a chance to drive NZD/JPY back up towards the 73.85 obstacle, marked by yesterday’s high. If that obstacle fails to hold the rate down, then a break of it could lead the pair further up to the 74.35 hurdle, which is Friday’s high.

On the other hand, a break of the short-term upside support line and a drop below the 73.17 hurdle could push NZD/JPY further down, where the pair may test the 72.85 support zone, marked by the low of the 8th of January. The rate could stall near that area until the bulls and the bears figure it out who takes control from there onwards. If the sellers remain in power, a drop below that zone could lead to the 72.15 level, which is the low of the 4th of January.

![]()

As for Today’s Events

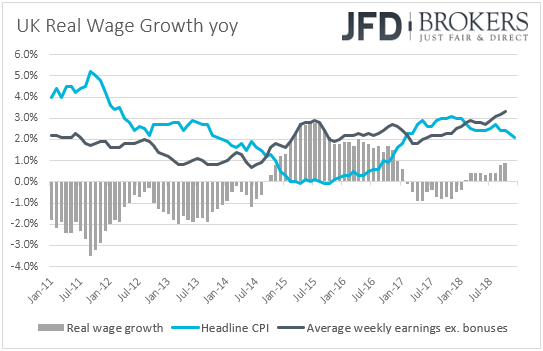

During the European day, the UK employment data for November is set to be released. The unemployment is forecast to have held steady at 4.1%, while the average weekly earnings, both including and excluding bonuses, are anticipated to have grown +3.3% yoy, the same pace as in October, and the fastest in a decade. According to the IHS Markit/KPMG & REC Report on Jobs for the month, wages for temporary staff increased at the fastest pace since July 2007, while starting salaries for permanent placements rose at one of the sharpest rates seen in the past 3.5 years. In our view, this supports the case for another set of strong wage growth rates.

From Germany, we get the ZEW survey for January. Expectations are for the current conditions index to have declined for the 4th consecutive month, to 43.0 from 45.3, while the economic sentiment index is forecast to have slid to -18.3 from -17.5, which will mark the 10th negative print in a row. Although this survey is usually not a major market mover, it comes after data showed that Germany’s annual growth rate hit a five-year low in 2018, and thus, another deterioration in analysts’ morale with regards to Eurozone’s economic powerhouse could increase speculation for a dovish shift by the ECB on Thursday.

Later in the day, we get the US existing home sales for December and Canada’s manufacturing sales for November. US home sales are forecast to have declined 1.0% mom after rising 1.9% in November, while Canada’s manufacturing sales are expected to have shrunk at a faster pace than previously. Specifically, expectations are for a 0.6% mom fall following a 0.1% slide in October.

Besides the economic releases, in Davos, Switzerland, the 49th Annual meeting of the World Economic Forum begins, and it will last until Friday. Last week we noted that we would look for any headlines surrounding the US-China trade standoff but given that President Trump has canceled the whole US delegation, we believe that the likelihood for any major market moving news coming out from the event has lessened.

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Group, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Group analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD Group prohibits the duplication or publication without explicit approval.

68% of the retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.