Risk Sentiment remained supported during the last day of the year, boosted by Trump’s remarks over the weekend. However, markets started 2019 on a defensive note after China’s Caixin manufacturing PMI for December slipped into contractionary territory for the first time since May 2017, reviving fears over a slowdown in the world’s second largest economy.

Markets Up on New Year's Eve, But Start 2019 on the Back Foot

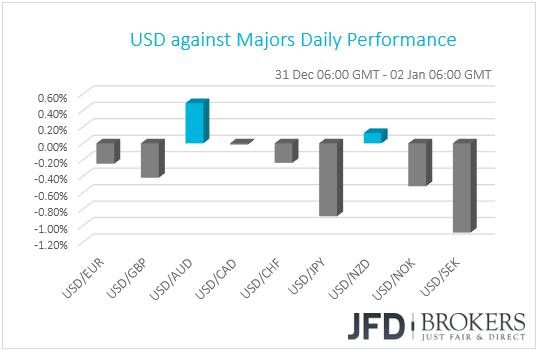

With markets closed on the New Year’s Day, the dollar traded lower against most of the other G10 currencies on Monday and during the Asian session Wednesday. It gained only against AUD and NZD, while it underperformed versus SEK, JPY and NOK in that order.

Although the weakening of the commodity-linked currencies and the strengthening of the safe-haven JPY suggest a risk-off environment, that was not the case on Monday. Market sentiment remained supported during the last day of the year, with most of the EU bourses that were open and all three US indices ending their sessions in positive territory.

Equity markets around the globe staged a comeback the day after Christmas, with Dow recording its biggest point-gain in history. Even though there was no clear catalyst behind that recovery, US President Trump’s remarks over the weekend may have further boosted investors appetite to end the year on a positive note. On Saturday, the US President said that he held a “very good call” with his Chinese counterpart over trade and added that “big progress” was being made.

However, the first trading day of 2019 shows that investors remain nervous, despite their upbeat mood during the last days of the year. Asian markets were a sea of red today, with China’s Shanghai Composite closing 1.15% down. Futures tracking Wall Street indices are in the red as well. The trigger behind the switch in market sentiment could have been the overnight slide in China’s Caixin manufacturing PMI for December into contractionary territory for the first time since May 2017. The slide may have revived fears of a slowdown in the world’s second largest economy, which still feels the heat of the trade frictions with the US.

In our view, even if new positive headlines surrounding the US-China trade saga help the financial community to switch back to a risk-on mode, the fundamentals that weighed on market sentiment during 2018 have not disappeared yet. Uncertainty surrounding the US-China sequel remains on the table, we believe, as the deadline for the two nations to seal an accord is drawing closer. Remember that a month ago, Trump and Jinping agreed to put tariffs on hold and solve their differences within 90 days, which means that the deadline expires on the 1st of March. With major issues still unresolved, whether the two nations could reach consensus by then still remains a mystery.

Signs over a broader scale global economic slowdown, the Fed’s future plans, and Brexit are also themes that could well spread anxiety. The partial shutdown of the US government, if continues, could also leave its mark. Therefore, we believe that is too early to start assuming that the global equity bloodbath is over and that the rebound during the last days of 2018 could lead to a full-scale recovery of the losses stock indices saw in the last quarter of the year.

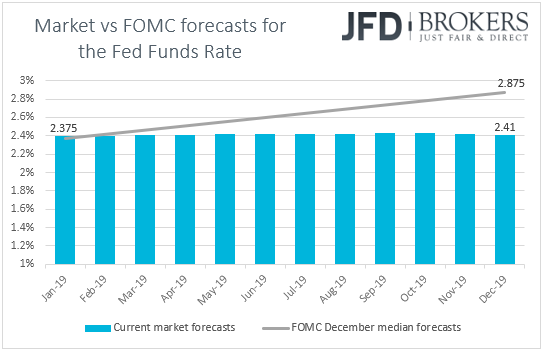

Speaking about the Fed, according to the Fed fund futures, market participants continued to push back their expectations with regards to the Committee’s future plans. They now see only a 15% chance for a quarter-point hike through 2019, which comes in huge contrast with policymakers’ projections of two increases next year.

In our view, this poses a downside risk for equities and an upside risk for the US dollar, which ended the year on the back foot, perhaps due to safe-haven outflows. With little left to price out in terms of Fed hikes, potentially upbeat US economic data, and especially on the inflation front, may prompt investors to reexamine their bets, and bring their estimates closer to the Fed’s.

S&P500 – Technical Outlook

Looking at the daily chart of our S&P500 cash index, the index is already having a rough start of the new year. After finding good resistance at around the 2522 barrier, near the 21 EMA, the price has dropped slightly. That said, bearing in mind the strong recovery in the last days of 2018, we believe that there is still a good chance for some more upside. However, we would still class any further recovery as a correction. The reason for that is that the price is still trading below a medium-term downside resistance line taken from the all-time high achieved in the beginning of October. Overall, in the bigger picture, this is not adding much confidence in the long-term upside potential. For now, we remain cautiously-positive, but only from the near-term perspective, and aim a bit higher. But if one of the key support areas get broken, we will straight away turn our views to more bearish and start examining the resumption of the latest downtrend.

If the S&P 500 travels a bit lower, but fails to break below the 2433 hurdle, marked by the inside swing high of the 24th of December, the bulls could step in again and drive the index back up. This is when we will target the strong resistance barrier at 2522, a break of which could open the way towards the 2552 level, which was the lowest point of April 2018. But that level could be just a small pit-stop for the S&P 500, as slightly above lies another good potential area of resistance at 2590, marked by the lows of the 16th of December and the 3rd of May 2018.

On the downside, a drop below the 2396 support zone, marked by the low of the 27th of December, could interest the bears again, which might put the index back under pressure. This is when we will target the December low near the 2323 barrier, a break of which could send the price lower to test the 2283 zone, marked by the low of the 8th of February and the high of the 6th of January 2017.

![]()

USD/JPY – Technical Outlook

USD/JPY continues to feel the heat, as the pair keeps selling off. The rate is currently trading below its short-term downside resistance line taken from the peak of the 17th of December. The pair is still weak, but looking at our oscillators, from the short-term perspective, USD/JPY looks a bit oversold, so it could recover some of its losses at some point soon. But as long as the pair remains below the above-mentioned downside resistance line, we will continue aiming lower in the near term.

USD/JPY could continue traveling further down to test the 109.00 hurdle, marked by the inside swing high of the 31st of May 2018. The area could provide support for the rate to move back up slightly. If USD/JPY is not able to overcome the 109.77 obstacle, or even the aforementioned downside line, the bears could step in again with another leg of selling. Another push lower and eventually a break of the 109.00 barrier, may clear the way to the 108.40 level, which is near the low of the 31st of May 2018.

Alternatively, a break above the previously-mentioned downside resistance line might place the bears on hold, and if the rate rises above the 110.20 hurdle, this might really spook the sellers for a while. USD/JPY could then move towards the 110.70 obstacle, a break of which may push the pair to re-test the 111.40 barrier, marked by the high of the 26th of December last year.

![]()

As for the Rest of Today’s Events

During the European morning, we get the final manufacturing PMIs for December from several European nations and the Eurozone as a whole. The bloc’s final print is once again expected to confirm its preliminary estimate, namely that the index fell for the fifth consecutive month to hit 51.4, the lowest since February 2016.

In the UK, the manufacturing PMI for the month is expected to have slid from 53.1 to 52.6, which would be the lowest since July 2016. Under normal circumstances, the market tends to pay more attention to the services index, which is scheduled for Friday, but given that the UK political scene has overshadowed economic data recently, once again, we don’t expect the PMIs to prove game changers with regards to the pound’s forthcoming direction. With the clock ticking towards the 29th of March, the official date the UK departs from the EU, and also the Parliament vote on PM May’s deal still looming, we believe that the British currency is likely to stay anchored to headlines surrounding the Brexit landscape.

We get the final Markit manufacturing PMI for December from the US as well, which is also expected to confirm its preliminary print.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Group, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Group analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD Group prohibits the duplication or publication without explicit approval.

68% of the retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2019 JFD Group Ltd.