Most major indices continued sailing north yesterday, boosted once again by news and headlines that the US and China are getting closer into singing a “phase one” deal. In the FX world, a day ahead of the Thanksgiving Day, USD-traders are likely to pay some attention to the yoy core PCE rate, which is the Fed’s favorite inflation gauge. The pound slid yesterday, after opinion polls showed that the Conservative Party’s lead is narrowing.

US-China Optimism Keeps Sentiment Supported, Pound Slips on Polls

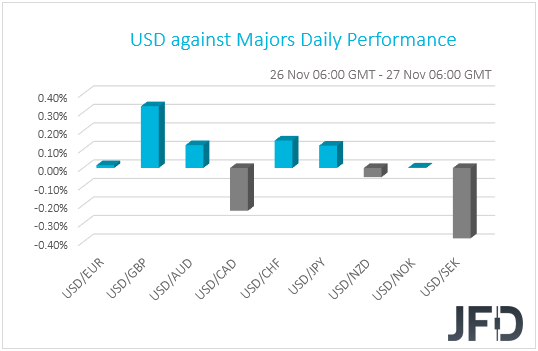

The dollar traded mixed against the other G10 currencies on Tuesday and during the Asian morning Wednesday. It gained versus GBP, CHF, AUD and JPY, while it underperformed versus SEK and CAD. The greenback was found virtually unchanged against EUR, NZD and NOK.

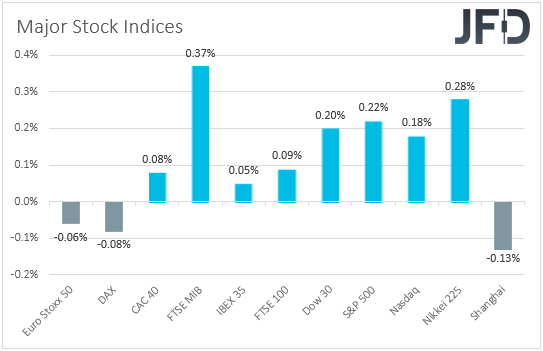

Once again, looking at the performance in the FX sphere, we don’t get a crystal-clear picture with regards to the broader market sentiment. However, the slight weakening of the safe havens CHF and JPY suggests that risk sentiment remained relatively supported. Indeed, looking at the equity market, we see that most EU indices, as well as the US ones, closed again in positive territory. The exceptions were Euro Stoxx 50 and the German DAX, which slid somewhat, 0.06% and 0.08% respectively. The majority of Asian indices also closed in positive territory today. Although China’s Shanghai Composite index slid 0.13%, Japan’s Nikkei 225 rose 0.28%.

What kept investors’ morale relatively supported was once again headlines surrounding the US-China trade saga. Yesterday, China’s Commerce Ministry confirmed that on Monday’s call, trade negotiators discussed remaining issues with regards to a “phase one” trade accord and that they agreed to maintain contact for resolving them. An expert close to the talks said that the topics discussed included tariff removals, agricultural purchases, and arrangements for another round of face-to-face talks. US President Trump added to the optimism as well, saying that the two nations are close to finding consensus on an interim accord.

Having said all that though, some Chinese experts noted that their nation will stick to its guns of demanding removal of existing tariffs, while adding to his comments, Trump underscored support for Hong Kong protesters, which is seen as an obstacle in the road towards consensus between the world’s two largest economies.

All this confirms our view that trying to figure out what could happen next remains a hard task. More upbeat headlines could keep risk appetite supported for a while more, but we will still maintain a cautious approach. We repeat for the umpteenth time that we are reluctant to trust a long-lasting uptrend before we see the trade conflict fully resolved. Even if a “phase one” deal is eventually signed, history has shown that things could still fall apart in the aftermath.

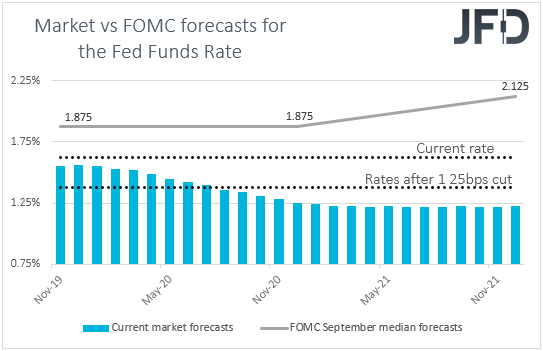

Back to the currencies and the dollar, just a day ahead of the Thanksgiving Day, its traders may pay some attention to the release of the yoy core PCE rate for October, which is the Fed’s favorite inflation gauge. The forecast suggests that the rate remained unchanged at +1.7% yoy, below the Fed’s objective of 2%. At its latest meeting, the FOMC decided to cut rates by another 25bps, but signaled that it is planning to take the sidelines, unless things fall out of orbit. That said, at the press conference, Fed Chair Powell said that a significant inflation rise is needed before they start considering hiking again, and a core PCE rate below 2% is likely to confirm that it will take long before policymakers turn their eyes to the hike button. It could even prompt market participants to bring forth the timing of when they expect the next cut to be delivered. After all, they have remained unconvinced that the Fed has stopped with reducing rates. According to the Fed funds futures, they are pricing in another quarter point cut to be delivered in July next year.

From Monday’s main gainer, the pound was Tuesday’s main loser, coming under selling interest after opinion polls showed that the Conservative Party’s lead is narrowing heading into next month’s election. As we noted yesterday, the pound’s faith heading onto the ballots is likely to continue being headlines surrounding the election, as well as incoming polls. There is more polling scheduled for today, something that may keep pound-traders cautious beforehand. Anything pointing to a clear Tory victory could be supportive for the currency, as it would increase the chances of the Brexit riddle being resolved before the new deadline expires. On the other hand, further narrowing of the Conservative’s lead could work against sterling as it could spark fears of a hung parliament and thereby, more months of deadlock.

USD/JPY – Technical Outlook

After breaking its short-term tentative downside line taken from the high of November 8th, USD/JPY continues to slowly grind higher, while trading above its short-term tentative upside support line drawn from the low of October 3rd. The pair managed to overcome last week’s high, at 109.07 and seems to be holding its course north, for now. The RSI and the MACD are both pointing higher, which suggests that there might still be some upside left. This is why we will take somewhat of a bullish approach and aim for slightly higher areas, at least in the short-run.

A push above the 109.07 hurdle has given the opportunity for the buyers to drive the rate towards its next potential resistance zone, at 109.49, which is the current highest point of November. The bulls might take a short break near that area, potentially causing a small decline. If the pair stays above the 109.07 zone, the small decline could be considered as temporary correction before another leg of buying. If so, USD/JPY might travel back to the 109.49 barrier, a break of which may set the stage for a further push higher towards the 109.93 level, marked by the high of May 30th.

Alternatively, a break of the aforementioned upside line and a rate-drop below the 108.47 hurdle, which is the low of November 22nd, could attract more bears into the field and the pair might drift to the 108.25 support area. That area is marked near the lows of November 14th and 21st, but if it’s just seen as a temporary pit-stop for the sellers, a break of it could send USD/JPY to the 107.88 zone, marked by the lowest point of November.

![]()

GBP/USD – Technical Outlook

Overall, GBP/USD is still trading above a short-term tentative upside support line drawn from the low of September 3rd. But from around the end of October, the pair is struggling to form a higher high and it is finding it difficult to get out of a range, which is roughly between the 1.2768 and 1.2985 levels. For now, we will stay neutral and wait for the rate to exit that range, before we examine a further directional move.

Given that the rate is currently closer to the lower side of the aforementioned range, at 1.2768, there is a chance we can see drop below it, which would confirm a lower low and the pair could end up traveling to the 1.2656 zone, marked by low of October 16th. If the selling doesn’t stop there, a break of that zone may lead GBP/USD to the 1.2606 level, which is the low of October 15th.

In order to examine higher areas, a break of the upper bound of the range, at 1.2985, would be required. Only then we will aim for the 1.3047 obstacle, or the 1.3080 hurdle, which are marked by the highs of May 10th and 8th respectively. If the rate gets a hold-up near those levels, it may correct back down a bit. But as long as it stays above the previously-mentioned upper side of the range, we will stay somewhat positive and aim higher. If GBP/USD gets another push from the bulls and gets lifted above the 1.3080 barrier, this could send the pair to the 1.3131 area, marked by the high of May 7th.

![]()

As for the Rest of Today’s Events

Alongside the core PCE index, we will get personal income and spending data for October. Personal income is expected to have risen +0.3% mom, the same pace as in September, while spending is expected to have accelerated somewhat to +0.3% mom from +0.2%. That said, given that the monthly earnings rate for the month declined to +0.2% from+0.4%, we see the risks surrounding the income forecast as tilted to the downside. With regards to spending, the forecast for improvement is supported by the month’s retail sales, which rebounded.

We also get the second estimate of the US GDP for Q3, which is expected to confirm its preliminary estimate, namely that US economic growth slowed to +1.9% qoq SAAR from +2.0% qoq in Q2. That said, even if we get a small deviation from the forecast, we don’t expect this release to attract much attention as we already have models suggesting how the economy has been performing during the current quarter. Both the Atlanta Fed and New York Nowcast models estimate a strong slowdown, to 0.4% and 0.7% respectively. However, given that we still have a lot of information to get with regards to November and December, this percentages may be subject to decent revisions.

Pending home sales and durable goods orders for October are coming out as well. Pending home sales are forecast to have slowed to +0.9% mom from +1.5%, while durable goods orders are expected to have declined 0.7% mom after tumbling 1.2% in September. The core rate is expected to have rebounded to +0.2% mom from -0.4%.

With regards to the energy market, we have the EIA (Energy Information Administration) report on crude oil inventories for last week. The forecast suggests a 0.418mn barrels slide, after the 1.379mn rise the week before. However, bearing in mind that yesterday, the API report revealed a 3.639mn inventory build, we see the risks surrounding the EIA forecast as tilted to the upside.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 78% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2019 JFD Group Ltd.