Yesterday a few major economies delivered on their preliminary manufacturing and services PMIs for the month of March. Also, the stock market traded in a “risk-on” fashion, with the Dow Jones Industrial Average leading the way, gaining just a bit more than 11% in one day. A deal is reached between Republicans and Democrats.

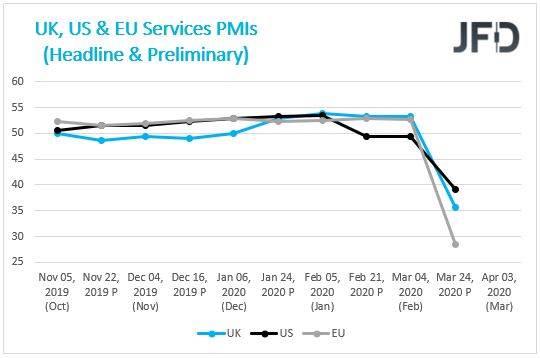

The Service Sector Gets A Hard Hit

Yesterday a few major economies delivered on their preliminary manufacturing and services PMIs for the month of March. The US, the UK, the eurozone and some individual European states were among those, which took the spotlight. All of those regions showed a decline in their March numbers, where some even dropped to their record lows. For instance, the EU’s preliminary services PMI were forecast to come out 39.0, which was already well below the previous 52.6. However, the actual number was even below that, at 28.4. The US and the UK actual services PMIs were also much lower than their forecasts. That said, the manufacturing PMIs from all of the three above-mentioned regions came out slightly less damaging than the services ones.

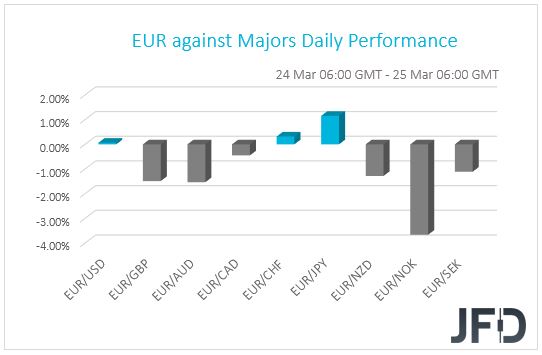

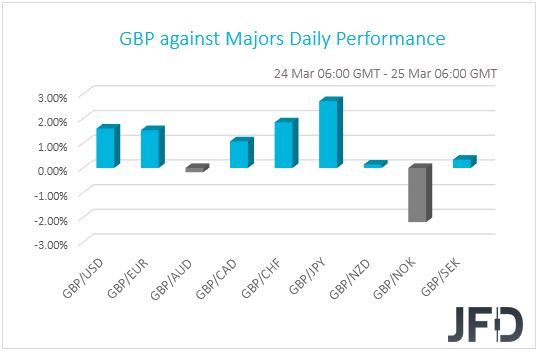

The pound showed good results yesterday, gaining against most of its major counterparts, apart from the commodity-linked AUD and NZD. Given the sharp rise in the prices of precious metals, like platinum, silver and gold, it was hard for other currencies to beat the Australian and New Zealand dollars. If the buying interest in precious metals stays for a bit longer and the equity markets go for some more recovery, we could see AUD and NZD gaining again.

GBP/CHF – Technical Outlook

GBP/CHF is at a very interesting spot right now, where it once again managed to get closer to its short-term downside resistance line taken from the high of February 26th. If that downside line stays intact, we could see another round of selling. For now, we will take a cautiously-bearish approach.

If the pair continues to get held by the aforementioned downside line and then falls below the 1.1500 hurdle, this could attract more bears into the field and allow them to send the rate even further south. That’s when we will aim for the 1.1360 hurdle, a break of which could clear the path to the 1.1244 zone, marked by the current low of this week. GBP/CHF might stall there for a bit, or even correct a bit higher. That said, if the bearish pressure remains, the pair could slide once again, potentially falling below the 1.1244 obstacle, where the next support area could be seen near the 1.1100 level, which is the current lowest point of March.

On the other hand, if the previously-mentioned downside line breaks and the rate rises above the 1.1713 barrier, marked by the high of March 20th, this may spook the bears from the field and allow more buyers join in. The pair might then drift to the 1.1830 obstacle, a break of which could send GBP/CHF to the 1.1934 hurdle, which is the high of March 13th. If the buying doesn’t stop there, a further push north may bring the rate closer to the 1.2055 level, marked near an intraday swing low of March 11th. Around there, the pair may find additional resistance from its 200 EMA on the 4-hour chart.

![]()

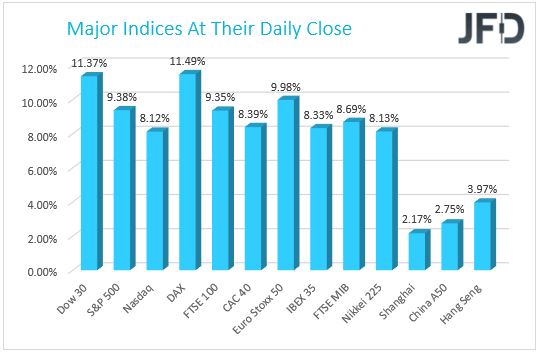

Markets Rally Before The Deal Is Even Reached

Yesterday the stock market traded in a “risk-on” fashion, with the Dow Jones Industrial Average leading the way, gaining just a bit more than 11% in one day. This has been the biggest gain since 1933. Other US indices followed the same direction, with the S&P 500 and the Nasdaq 100 gaining 9.38% and 8.12% respectively. The US markets rushed to the upside, after the news broke out that US lawmakers were close to reaching a deal for a 2 trillion-dollar bailout package to help stimulate the economy, which has been shaken by the coronavirus pandemic. But the US futures were already on a decent uprise during the European session, as the FTSE 100, Euro Stoxx 50 and DAX were leading the way. Other European bourses were also a sea of green. It looked like the markets took a break from all the negative headlines surrounding the COVID-19.

A few hours after the close of the US markets, reports started coming in that the deal has been reached between Republicans and Democrats. A few points from that bill: $130 billion will be allocated to hospitals, $150 billion to go to the state and local governments. Also, there will be a strict oversight of loans, which will go directly to companies, in order to support their operations during these difficult times. However, our concern here is how effective the new stimulus package will be? For now, it may support the market and we could see equities gaining in the near term. That said, given that the global economy has already been shaken and countries across the globe are expected to deliver their Q1 with Q2 numbers on the lower side, the temporary rise might be a good opportunity for market participants to short again. Even if the governments manage to control the number of infections and deaths from the coronavirus, the negative effects of it could last even longer.

S&P 500 – Technical Outlook

The S&P 500 rallied yesterday, moving further north, away from its March low, at 2182. Although we may see a bit more upside in the near term, let’s not forget that the index is still trading below its short-term tentative downside resistance line taken from the high of February 20th. As long as that downside line stays intact, we will remain bearish overall.

As mentioned above, we may see a bit more upside in the near term, especially if the price travels above the 2510 hurdle, marked by the high of March 20th. The index could continue drifting a bit further and break another possible resistance area, at 2563, which is the high of March 16th. However, if the S&P 500 struggles to break the aforementioned downside line, this might lead to another round of selling, possibly bringing the price all the way back to the 2395 zone, marked by the high of March 23rd and near today’s low. If the sellers are still feeling confident, a further drop could send the US index to the 2252 hurdle, or even the 2182 level, marked by the current lowest point of March.

Alternatively, if the previously mentioned downside line breaks and the price climbs above the 2709 barrier, marked by the high of March 13th, this may help more buyers to join in. We will then aim for the resistance are between the 2848 and 2888 levels, a break of which could open the door for a further uprise towards the 3038 territory, marked by the high of March 6th.

![]()

The Coronavirus Remains A Big Issue

In regards to the ongoing coronavirus pandemic, yesterday we crossed over the 400000 mark of infected people. Certainly, let’s not forget that it is the official figure, as we must take into account the fact the number is most likely higher. Looking at the available statistics, Italy is rapidly getting closer to the Chinese number of infected people, which currently stands roughly at around 81600. Although, Italy is still below that figure, the Apennine peninsula has already beaten the Chinese official death toll twice. Spain is also rapidly approaching the Chinese death number, which currently stands at around 3300. But there are worries that despite Europe’s fast rise in the number of people dying from the virus, the US could catch up very quickly on that front. The US is already in third place in the global rankings of total infected people, however the death toll is only about a sixth of the Chinese figure in the same category. That said, let’s not forget that this number might grow very quickly if the US will not take any stronger measures to safeguard its population. There are already reports stating that the US is having a huge shortage of medical supplies, like ventilators, which help support the lives of badly infected patients. In addition to that, respiratory mask are also in huge deficit. While China is sending such masks and other medical supplies to Europe, the US started asking its allies for the same supplies. Donald Trump offered his colleague, South Korea’s president, to allow Korean companies to gain US government approval for an easier operation within the US market. Moon Jae-in replied, saying that they will help and send medical supplies to the US, if South Korea will have any spare left.

If the situation in the United States worsens and the numbers of infected people and deaths from the virus continue to rise rapidly, all the recent market gains might get wiped out soon. This is because investors may start losing faith that the new US stimulus package, could bring any good. Investors already understand that not only that Q1 will show terrible results, Q2 numbers won’t be very satisfying as well. This means that we could be closer to a proper recession, as the US indices have already managed to wipe out around 35% from their peaks in February this year.

As For The Rest Of Today’s Events

This morning, the United Kingdom delivered various data figures, a few from which were the core and headline inflation numbers for the month of February. Both core and headline MoM figures came out not only better than their previous readings, but also better than the expectations. The core MoM rose to +0.6% from the previous -0.6%. The headline MoM went from -0.3% to +0.4%. The YoY core and headline readings were slightly mixed. The core figure wend from +1.6% to +1.7%, but the headline one fell from +1.8% to +1.7%.

Later on today, Germany will deliver its Ifo Business Climate number, which is currently forecasted to have declined from 96.0 to 87.7. If the number comes out even below the forecast, the euro could once again feel some downside pressure and slide against some of its major counterparts.

In the US, durable goods orders for February are due to be released. Both the headline and core rates are expected to have slid to -0.8% mom and -0.3% mom respectively, from -0.2% and +0.8%. The case for lower durable goods rates is supported by the New Orders sub-index of the ISM manufacturing PMI for the month, which slid to 49.8 from 52.0.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 76% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2020 JFD Group Ltd.