Equities traded south yesterday and today in Asia, which combined with risking bond yields suggests that market participants are increasing their bets with regards to faster tightening by several major central banks. The yen was the main gainer among the major currencies, but the Swiss franc, which is also considered a safe-haven, was the main loser, perhaps due to the increase in the SNB’s sight deposits. As for today, Fed Chair Powell testifies before the Senate Banking Committee, and it will be interesting to hear his view with regards to the Fed’s future course of action.

Rising Yields Hurt Equities as Investors Await Powell’s Remarks

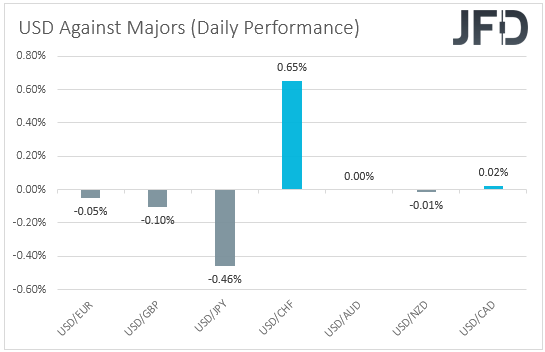

The US dollar traded nearly unchanged against most of the other major currencies on Monday and during the Asian session Tuesday. It gained only against CHF, while it underperformed versus JPY, and slightly against GBP.

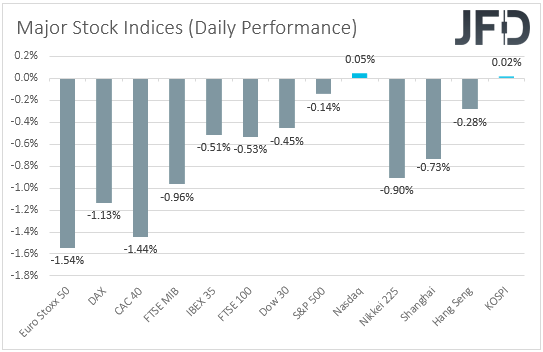

Now, given that both the Japanese yen and the Swiss franc are considered safe-haven currencies, the fact that they moved in opposite directions paints a confusing picture with regards to the broader market sentiment. A strengthening yen could be a sign of a risk-off trading activity, while a weaker franc points otherwise. Shifting attention to the equity world, we see that major EU indices were a sea of red, with the negative appetite rolling into the opening of the US session. Despite Wall Street staging a strong come back later in the day, only Nasdaq managed to poke its nose in positive territory, while today, in Asia, appetite deteriorated again.

With European and US bond yields rising as well, we can only assume that the driver behind those market movements may have been expectations over faster tightening. Yes, some participants may have already increased their tightening bets with regards to the Fed, but now, it seems that they are looking at the ECB as well. Although the Bank has clearly pointed that they are unlikely to touch the hike button this year, last week’s unexpected acceleration in Eurozone inflation may have prompted some investors to add such kind of bets.

Now, as far as the Swiss franc is concerned, the fact that the SNB’s sight deposits increased notably last week, suggests that the central bank has resumed its foreign currency purchases to prevent its own from rising further. With that in mind, and also taking into account the rising expectations over a faster tightening process by the Fed, we would expect the USD/CHF pair to continue drifting north. After all, it seems that the SNB is one of the few banks market participants are anticipating to stay dovish for a long time, and its actions point to that direction. Ok, some risk-off episodes could result in some franc inflows, but we don’t expect them to be game changers. We believe that FX traders looking for a haven shelter may prefer the yen for now.

As for today, Fed Chair Jerome Powell is due to testify before the Senate Banking Committee at a hearing to confirm his nomination to a second term. Fed Governor Lael Brainard is also scheduled to appear before the same committee on Thursday for a confirmation on her nomination as Vice Chair.

On Friday, the US employment report revealed that nonfarm payrolls slowed to 199k in December from 249k in November, missing estimates of an acceleration to 400k. This resulted in a retreat in the US dollar, but it did not change expectations around the Fed’s future course of action. After all, the unemployment rate tumbled to a 22-month low of 3.9%, while wages accelerated unexpectedly in monthly terms.

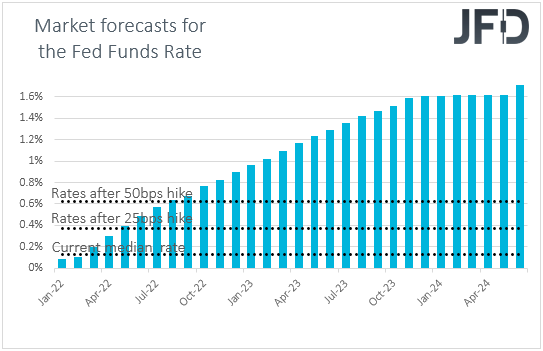

According to the Fed funds futures, market participants are still fully pricing in the first quarter-point rate increase to be delivered in May, with a decent chance of this happening one or even a couple of months earlier. Many believe that this will happen in March. Therefore, it will be interesting to hear what those two officials have to say, especially with the minutes of the latest gathering revealing that officials said that the “very tight” labor market may warrant sooner rate increases. Brainard, who has been considered a dove before her nomination, appeared more hawkish than expected when she was appointed, showing commitment to getting inflation down. In our view, the risks are for both officials to support a faster than previously assumed rate path. After all, Wednesday’s CPI data are expected to reveal that inflation has continued to accelerate in December, with the headline rate hitting 7.0% for the first time since 1982, and the core one rising to 5.4%. Anything suggesting a more cautious approach could come as a surprise and perhaps bring the US dollar under strong selling interest.

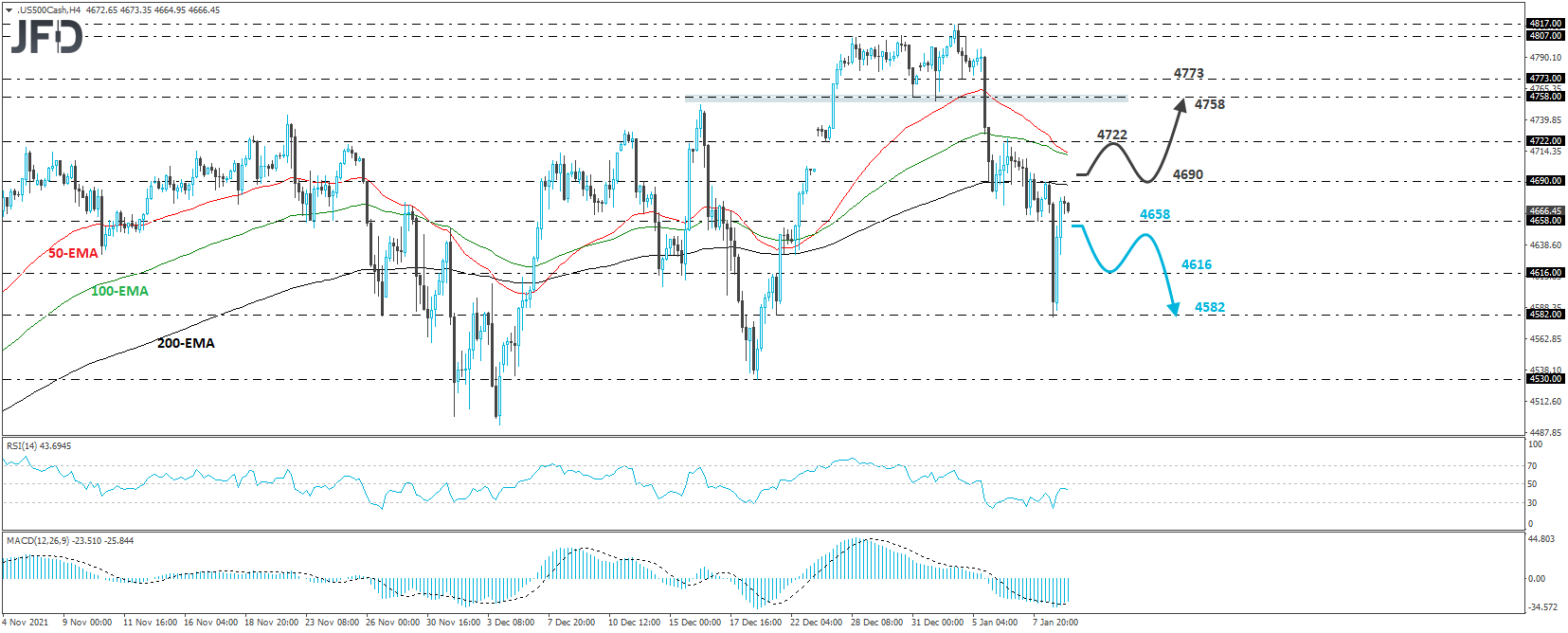

S&P 500 – Technical Outlook

The S&P 500 cash index fell sharply yesterday, but hit support near the 4582 barrier, marked by an intraday low formed on December 21st, and then it rebounded strongly. However, the price structure on the 4-hour chart remains of lower higher and lower lows and thus, we would still see a somewhat a negative short-term picture.

A dip back below Friday’s low of 4658 may confirm that the bears are back in control and could initially pave the way towards the 4616 zone, marked as a support by an intraday swing high formed on December 21st. If they are not willing to stop there, then a break lower could see scope for more declines and perhaps another test near the 4582 zone.

On the upside, a break above 4690 could signal the continuation of yesterday’s late recovery. The first stop after that could be the peak of Thursday, at 4722, the break of which could extend the recovery towards the key zone of 4758, which provided support on December 31st and January 3rd.

USD/CHF – Technical Outlook

USD/CHF traded sharply higher yesterday, to hit resistance at 0.9275. Then, it pulled somewhat back. Overall though, the pair remains above the prior downside resistance line taken from the high of November 24th, as well as above the upside support line drawn from the low of December 31st. Therefore, even if the rate corrects a bit lower, we would stay positive with regards to the short-term picture.

The bulls may decide to stop the current setback near the aforementioned short-term upside line and perhaps shoot for another test at the 0.9275 barrier, the break of which would confirm a forthcoming higher high and perhaps target the peak of December 15th, at around 0.9295. Another break, above 0.9295 could carry extensions towards the inside swing low of November 25th, at 0.9325.

On the downside, a dip below 0.9219 could signal the break below the short-term upside line and may first target the 0.9200 area, which provided decent resistance between December 27th and January 6th. If the bears are not willing to stop there, we could see them aiming for the low of January 7th, at 0.9182, the break of which could carry extensions towards the low of January 4th, at 0.9135.

As for the Rest of Today’s Events

Besides Fed Chair Powell, we will also get to hear from ECB President Christine Lagarde and ECB Governing Council member Jens Weidmann. It will be interesting to see what they have to say after last week’s inflation data, and how the market may respond to their remarks.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68.02% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2022 JFD Group Ltd.