Most global equity indices traded in the green yesterday and today in Asia, despite the US CPIs unexpectedly accelerating. That said, with market participants bringing forth their expectations with regards to a Fed rate increase, we remain reluctant to conclude that we are back in uptrend mode. We believe that the fundamental background for the markets has not change yet, something that could keep any further recovery short lived.

Equities Rebound Despite US Accelerating and Cementing a November Fed Taper

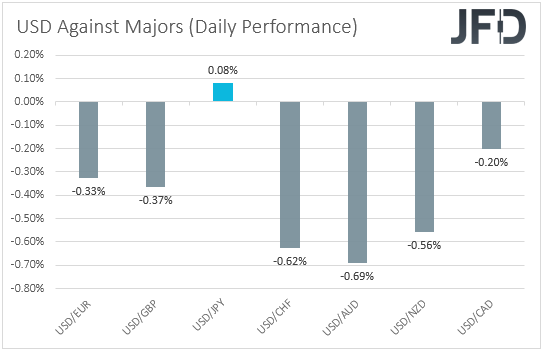

The US dollar traded lower against all but one of the other major currencies on Wednesday and during the Asian session today. It eked out some gains only against JPY, while it underperformed the most against AUD, CHF, and NZD in that order.

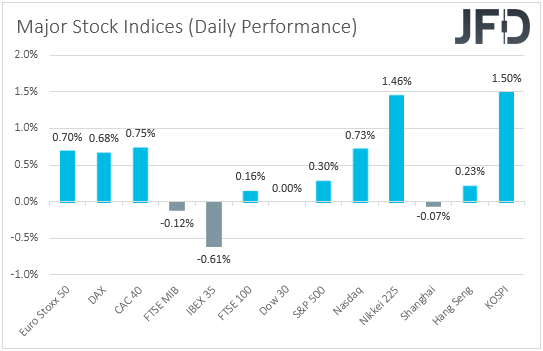

The strengthening of the risk-linked Aussie and Kiwi, and the weakening of the dollar and the yen suggest that trading turned to risk-on yesterday and today in Asia. The only reaction that doesn’t fit the equation is the strengthening of the Swiss franc. Looking at the performance in the equity world, we see that, indeed, most major EU indices traded in the green, with the relative optimism rolling into the US session as well. The only exceptions were Italy’s FTSE MIB and Spain’s IBEX 35, which slid, as well as Wall Street’s Dow Jones, which finished virtually unchanged. Investors’ appetite remained supported during the Asian session today as well.

European stocks rose perhaps due to the bloc’s most valuable tech company SAP raising its full-year outlook for a third time, and as French luxury goods maker LVMH revealed that sales at its fashion and leather goods division rose strongly during the third quarter. What may have also helped investors’ morale may have been China’s trade data, with exports surprisingly accelerating in September. Wall Street and Asian markets remained somewhat supported as well, despite the US CPI data revealing that headline inflation unexpectedly ticked up, and even after the minutes of the latest FOMC gathering revealed that policymakers continued to judge that the risks around the inflation projections were tilted to the upside.

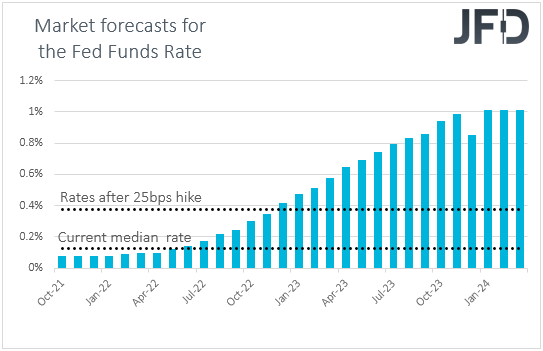

In our view, yesterday’s market action may have been another short-covering activity, or in the absence of any fresh negative headlines, investors may have indeed become confident to add more stocks to their portfolios. However, we are reluctant to conclude that the downside is over and that we are back in uptrend mode. After all, the fundamental outlook has not change yet. Oil prices, despite pausing their rally, remain elevated, meaning that inflation could still accelerate further, thereby resulting in faster tightening by central banks. Indeed, following yesterday’s US CPIs and the Fed minutes, market participants brought even forth their expectations of when the Committee may hit the hike button for the first time since the pandemic outbreak. According to the Fed funds futures, a 25bps rate increase is now nearly fully priced in for November 2022.

Today, we get the US PPIs for September, with both the headline and core yoy rates expected to have risen further, something that could intensify concerns over more acceleration in consumer prices in the months to come. That’s why we believe that any additional recovery in equity markets could stay short-lived, and another setback could be possible. As for the US dollar, we expect it to rebound soon and resume its prevailing uptrend.

DAX – Technical Outlook

The German DAX cash index traded higher yesterday, and today, during the Asian morning, it managed to break above the high of October 3rd, at 15295. This suggests that some further recovery may be in the works, but as long as the index remains below the downside line taken from the high of August 31st, we would expect it to stay short lived.

If the bears take charge from near that downside line, or the 15477 barrier, marked by the high of September 30th, we could see a slide back below 15295. This could initially target the inside swing high of October 12th, at 15180, the break of which could see scope for declines towards the 14990 zone. With the exception of October 6th, that territory has been acting as a decent support since September 20th.

On order to start examining whether the outlook has turned positive, we would like to see the recovery extending above 15630, the high of September 28th. The index will already be above the aforementioned downside resistance line and may target the high of September 27th, at 15720, or the peak of September 17th, at 15795. If neither hurdle is able to stop the bulls, then we could see advances towards the 15960 area, defined as a resistance by the high of September 6th.

EUR/USD – Technical Outlook

EUR/USD also edged north yesterday, breaking above the downside resistance line taken from the high of September 14th, as ell as above the 1.1587 zone, marked by the highs of October 8th and 11th. However, the pair remains below another downside line, drawn from the high of September 3rd, which suggests that any further recovery may stay limited.

We believe that the bears may jump back into the action from near the crossroads of that line and the 1.1640 barrier, marked by the high of October 4th. This could result in a slide back near the 1.1587 zone, the break of which may open the path towards the 1.1524 area, defined by the low of October 12th.

In our view, the bulls may gain full control upon a break above the 1.1690 territory, marked by the high of September 29th. This may cement the break above the downside line taken from the high of September 3rd, and could allow advances towards the 1.1749 level, defined by the high of September 17th. Another break, above 1.1749, could carry extensions towards the high of September 15th, at 1.1837.

As for the Rest of Today’s Events

During the Asian session today, we got Australia’s employment report for September. The economy lost more jobs than anticipated, while the unemployment rate slid, but due to more people being discouraged to apply for unemployment benefits. This may have been a reality check for those who have recently started to place bets that the RBA might hike rates late next year, despite the Bank itself keep stating that any such move is unlikely before 2024. The Aussie pulled back at the time of the release, and yet, it still was the main gainer among the major currencies.

Later in the day, at the same time with the US PPIs, we get the nation’s initial jobless claims for last week, with expectations pointing to a small decline. The EIA report on crude oil inventories for last week is also coming out and the forecast suggests a 0.702mn barrels inventory build, after a 2.346mn rise the week before.

As for the speakers, we have five on today’s agenda and those are: ECB Executive Board member Frank Elderson, BoE MPC member Silvana Tenreyro, Atlanta Fed President Raphael Bostic, Richmond Fed President Thomas Barkin, and New York Fed President John Williams.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 73.90% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2021 JFD Group Ltd.