Equity markets were hit again yesterday, with the S&P 500 and Dow Jones erasing their yearly gains as they closed below their 2018 opening levels. CAD gained as the BoC delivered a hawkish hike, while SEK was the main loser after the Riksbank kept the February-hike option on the table. As for today, the central bank torch will be passed to the ECB and the Norges Bank.

Equity Markets Slump Again, BoC Delivers a 'Hawkish Hike'

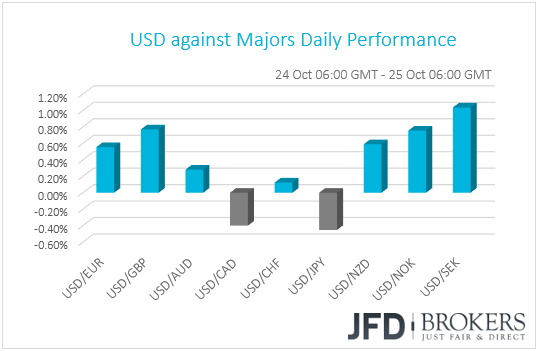

The dollar traded higher against most of the other G10 currencies on Wednesday. It lost ground only against JPY and CAD, while it traded virtually unchanged versus CHF. The greenback gained the most against SEK, GBP and NOK in that order.

Risk appetite deteriorated against yesterday, with the safe havens gaining traction and major equity indices tumbling further. The exception was UK’s FTSE 100, which closed 0.11% up. S&P, Dow and Nasdaq ended the US session 2.41%, 3.09% and 4.43% down respectively, with the former two erasing all the gains achieved during the year as they closed below their 2018 opening levels. Uncertainty around Italy and Brexit, fears of slowing global growth, the US-China trade saga, concerns over faster Fed hikes, and the recent disappointing corporate earnings in the US, all constitute a risk blend that it’s hard to overlook.

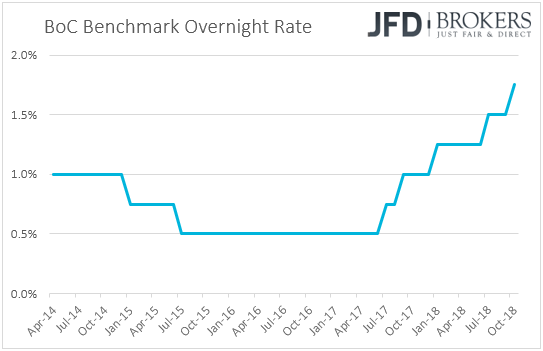

The Canadian dollar managed to gain against its neighboring greenback after the BoC raised interest rates by 25bps and removed the part saying that officials will “take a gradual approach” with regards to future rate increases. Instead, they simply noted that “In determining the appropriate pace of rate increases, Governing Council will continue to take into account how the economy is adjusting to higher interest rates”. They also noted that interest rates will need to rise to a neutral stance in order to achieve the inflation target. In our view, the removal of the “gradual approach” means that interest rates can now rise faster than previously anticipated if data suggest so, which may have come as a surprise to investors waiting for a more cautious stance after last week’s disappointing inflation data.

The biggest loser was the Swedish krona, which came under selling interest following the Riksbank interest rate decision. The world’s oldest central bank kept interest rates unchanged as was expected, and repeated that the repo rate will be raised by 25bps either in December or February, which may have come as a disappointment to those who raised bets that the Bank will dismiss the February option following the better-than-expected inflation prints for September, and especially the strong acceleration in the core CPIF metric.

DJIA – Technical Outlook

Yesterday, the equity markets got hit heavily again and the Dow Jones Industrial Average, together with the S&P 500, closed below their yearly opening prices. At first, it looked like the DJIA was finding it hard to move away from the 25000 level, but as the US session was getting closer to the closing bell, the indices started selling off. Certainly, we could see a bit of correction happening back to the upside, but as long as the price remains below the short-term downside resistance line drawn from the high of the 10th of October, we will remain bearish for now.

Looking at the DJIA cash index, we can see that, yesterday, it found good support near the 24528 zone. Since then, the index has retraced slightly back to upside, but still remains below the year’s opening price, marked by the thick black line. If Dow decides to move back down and drops below the 24528 mark, this is where we could brace ourselves for another set of selling activity, which could lead to a test of the 24330 area, marked near the high of the 1st of July. If that area is not able to withhold the bear-pressure, a further decline towards the 24050 hurdle, which was the low of the 2nd of July, could be possible.

The RSI seems to have stopped near 25 but doesn’t look like it wants to move away from there for now. The MACD is below its zero and trigger lines and continues to look for opportunities lower, as it is still pointing to the downside. Both indicators support the bearish case for now.

For us to get comfortable with the upside again, we would need to see, not only a break above the aforementioned downside resistance line, but also a close above the 25120 area, which acted as good support on the 15th of October. Only then we could start looking at next possible resistance levels like 25600, or even the 25860 barrier, marked by the high of the 17th of October.

![]()

ECB and Norges Bank Take the Central Bank Torch

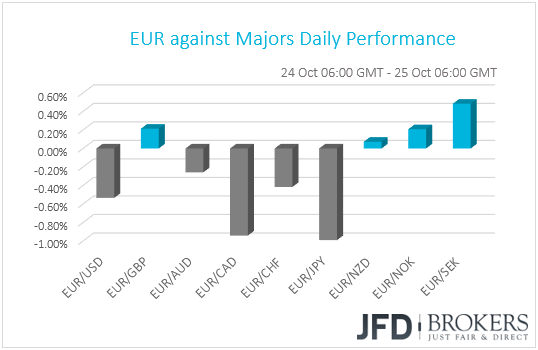

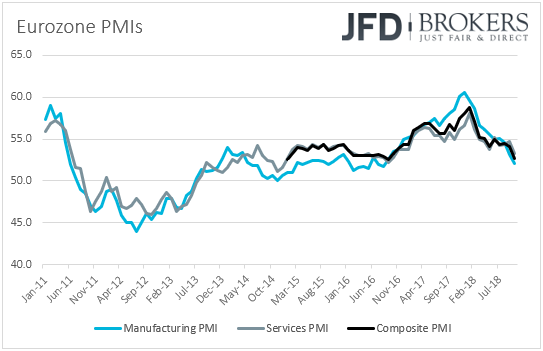

The euro traded lower against the majority of the other G10 currencies following the more-than-anticipated slide in Eurozone’s preliminary PMIs for October (see below). It outperformed only SEK, GBP and NOK, while it traded virtually unchanged against NZD. It lost the most ground against JPY, CAD and USD.

Today, EUR-traders are likely to be sitting on the edge of their seats in anticipation of the outcome from the ECB monetary policy meeting. No change in policy is expected, so all the attention is likely to fall on the accompanying statement and President Draghi’s press conference after the decision.

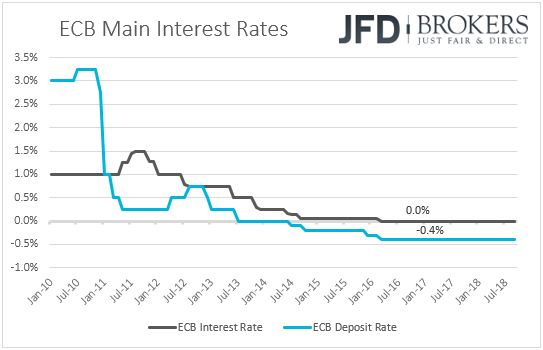

At its latest meeting, the Bank downgraded its growth projections, but at the conference, President Draghi appeared fairly optimistic, noting that the balance of risks surrounding growth has not changed. What’s more, speaking at the Economic and Monetary Affairs of the European Parliament hearing, Draghi said that he sees a “relatively vigorous” pickup in underlying inflation as the tightening labor market is resulting accelerating wage growth.

Since then, inflation data showed that the headline CPI rate ticked up to +2.1% yoy in September from 2.0% in August, but underlying inflation slowed to +0.9% yoy from +1.0%. What’s more, yesterday’s preliminary PMI surveys for October revealed that manufacturing activity slowed for the 10th consecutive month, while the services index, although it showed some stability signs in the second half of the year, slid to a two-year low. This dragged the composite index down to 52.7 from 54.1, its lowest since September 2016.

So, having all these in mind, although we still expect policymakers to stick to their guns and repeat that asset purchases are likely to end in December, we don’t expect them to confirm it. We expect them to reiterate that the decision would stay subject to incoming data. If this is the case, the lack of any major changes in the statement would turn the spotlight to Draghi’s conference. Market participants may be eager to hear whether he remains as optimistic as in September or whether recent data have changed his mind.

Judging by the euro’s reaction to yesterday’s PMIs, investors may have already positioned themselves for a more cautious approach. Thus, if Draghi sticks to his guns and reiterates that the risks the risks surrounding the economic outlook are still broadly balanced and that the underlying strength of the economy continues to support the Council’s confidence on the convergence of inflation to the target, then the euro is likely to rally. On the other hand, if he adopts a more cautious stance, for example saying that the risks have now tilted to the downside, this may encourage the bears to shoot again and push the currency towards lower levels.

Having said all these though, even if the euro rallies in case Draghi appears upbeat, we see the case for any gains to stay capped. Uncertainty surrounding the Italian budget has been the main catalyst behind the euro’s latest downfall and the matter is far from resolved. As we noted yesterday, we need to see handshake between EU and Italian officials before we consider that risk to be out of the way.

Ahead of the ECB, we have another Bank deciding on interest rates: the Norges Bank. However, we expect this Bank to attract less attention than usual. At their previous meeting, Norwegian policymakers decided to increase rates to +0.75% from +0.50% as was widely anticipated, but lowered their projected rate path, disappointing those expecting more hawkish approach. They also noted that the next rate increase will most likely come in Q1 2019. Since that meeting, data showed that both the headline and core inflation rates remained unchanged at +3.4% yoy and +1.9% yoy respectively, something suggesting that the statement is unlikely to contain any major changes. Having also in mind that we will not get updated economic projections, we don’t expect any major market reaction from NOK.

EUR/USD – Technical Outlook

The common currency continues to weaken against the US dollar and yesterday was a good example to that, as we saw EUR/USD tumbling almost 100 pips. The pair broke through its key support at 1.1430, which kept holding the rate from dropping lower throughout this month. Even if EUR/USD gets back above 1.1430, we will still remain bearish, as the pair is still below its short-term downside resistance line drawn from the peak of the 26th of September. EUR/USD continues to build lower lows and lower highs; thus, we will continue aiming to the downside.

EUR/USD found good support near the 1.1380 level, which now becomes an important area to monitor. Since establishing that new support, the pair has corrected slightly to the upside, but still remains below the previously mentioned 1.1430 hurdle, which now could be seen as strong resistance. A move below the 1.1380 support line, could open the path for test of the 1.1345 obstacle, a break of which could set the stage for a further decline towards the 1.1300 zone, marked by the lowest point of August.

Alliteratively, a break above the aforementioned downside resistance line could put a somewhat positive spin on the near-term outlook of EUR/USD. But for a better confirmation of the potential upside, we would need to see the pair breaking the 1.1550 barrier, marked by the high of the 22nd of October. This way, we could start examining the possibility for the pair to move higher towards the 1.1595 zone, or even the 1.1625 area, marked near the peak of the 16th of October.

![]()

As for the Rest of Today’s Events

During the European morning, we have the German Ifo survey for October. Both the current assessment and expectations indices are anticipated to have declined to 106.0 and 100.3 from 106.4 and 101.0 respectively, something that could bring the business climate index down to 103.2 from 13.7.

In the US, we get durable goods orders for September. Headline orders are forecast to have fallen 1.1% mom after rising 4.4% in August, but the core rate is anticipated to have risen to +0.5% mom from +0.1%. Pending home sales for the same month and initial jobless claims for the week ended on the 19th of October are also coming out.

As for tonight, during the Asian morning Friday, Japan’s Tokyo CPIs for October are set to be released. No forecast is available for the headline rate, while the core one is expected to have remained unchanged at +1.0% yoy.

We also have two speakers on the agenda: Fed Vice Chair Richard Clarida and Cleveland Fed President Loretta Mester.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.