Equities traded mixed yesterday, but China’s and Hong Kong’s markets took a beating today, perhaps on worries over government regulations in the education, property, and tech sectors. Although some EU and US stocks traded in the green, investors still appear careful ahead of tomorrow’s FOMC decision. Ahead of the decision, during the Asian session Wednesday, Aussie traders may pay attention to Australia’s CPIs for Q2, as they try to paint a clearer picture with regards to the RBA’s potential plans.

Equities Trade Mixed Ahead of the FOMC Decision, AU CPIs on the Agenda

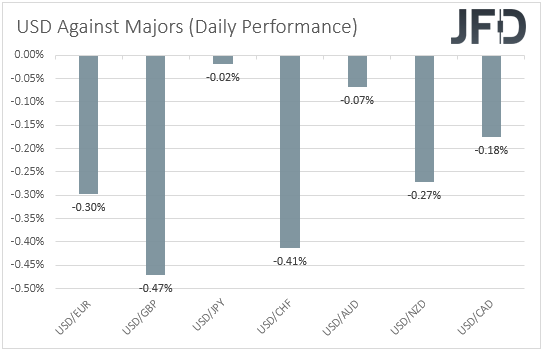

The US dollar traded lower on Monday and during the Asian session Tuesday, losing the most ground against GBP, CHF, and EUR. The greenback slid the least against JPY and AUD.

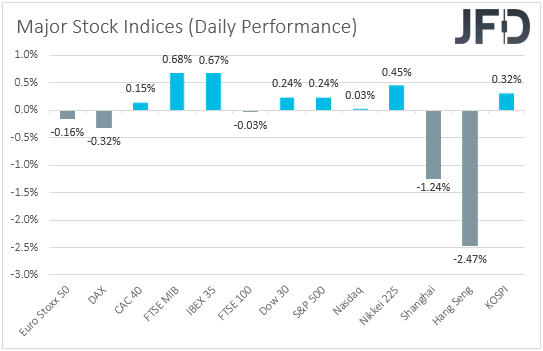

The strengthening of the Swiss franc, combined with the relative weakness in the Aussie, suggests that markets traded in a risk-off fashion yesterday and today in Asia. However, the underperforming greenback and yen point otherwise. Thus, in order to get a clearer picture with regards to the boarder market sentiment, we prefer to turn our gaze to the equity world. There, EU indices were mixed with DAX and Euro Stoxx 50 falling somewhat, perhaps after the German Ifo survey missed its own estimates, suggesting that Eurozone’s growth engine may have started to slow. However, other indices, like Italy’s FTSE MIB and Spain’s IBEX 35, traded well in the green, perhaps de to strong earnings reports and last week’s dovish message from the ECB.

In the US, investors were also cautious ahead of tomorrow’s FOMC decision. All three of Wall Street’s main indices hit fresh records, but they were quick to pull back, erasing some of their early gains. This may have not only been due to being careful ahead of the Fed decision, but it could also be due to the fact that this week is packed with earnings from big giants, like Facebook, Alphabet, Apple, Amazon and Microsoft. Tesla released its results yesterday, after the closing bell. The numbers were better than anticipated, with record-setting deliveries for the June quarter helping propel the company's results. Its share price gained more than 2.5% in after-hours trading, which means that the stock could open with a positive gap today. In Asia, China’s Shanghai Composite and Hong Kong’s Hang Seng took a beating on worries over Chinese government regulations in the education, property, and tech sectors.

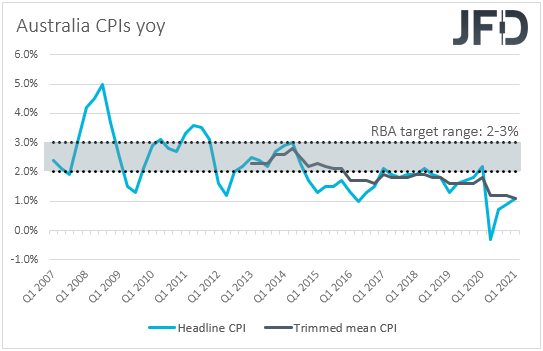

With no major events scheduled for today, investors may maintain their cautious stance ahead of tomorrow’s FOMC outcome. However, well ahead of that, tonight, during the Asian session Wednesday, Aussie-traders may pay attention to Australia’s CPIs for Q2. The headline rate is forecast to jump to +3.8% yoy from +1.1%, above the upper end of the RBA’s 2-3% target range. However, the trimmed mean rate, although also expected to rise, is forecast to have stayed below the lower bound of that range. Specifically, the trimmed mean rate is anticipated to have risen to +1.7% yoy from +1.3%. Therefore, with underlying inflation staying below the RBA’s objective, we doubt that Aussie-traders will start betting on earlier tightening by this Bank. At this month’s gathering, officials announced that they will proceed with more bond purchases, beyond September, and also said that they are planning to keep rates at current levels until 2024. With that in mind, even if market sentiment continues to improve, we believe that the Aussie is likely to perform poorer than its other risk-linked counterparts, especially the Kiwi, the central bank of which is expected to push the hike button very soon, perhaps as early as next month.

Hang Seng – Technical Outlook

Hong Kong’s Hang Seng tumbled overnight, with the cash index falling below yesterday’s low of 26100. Overall, the index continues to print lower lows and lower highs below the downside resistance line drawn from the high of June 28th, and thus, we would still see a negative short-term outlook.

If the bears are willing to stay behind the steering wheel, we could soon see them targeting the 25570 area, marked by the low of November 6th, the break of which could extend the fall towards the inside swing high of November 3rd, at 25165. Another break, below 25165, could allow a test near the low of that day, at around 24640.

Now, in order to abandon the bearish case and start examining a bullish reversal, we would like to see a recovery above the 27770 barrier, marked by the high of July 22nd. This will also confirm the break above the downside resistance line drawn from the high of June 28th and may encourage the bulls to climb towards the 28225 zone, marked by the peak of July 16th, the break of which may see scope for larger upside extensions, perhaps towards the peak of 28895, which is the high of July 2nd, or the peak of June 28th, at 29350.

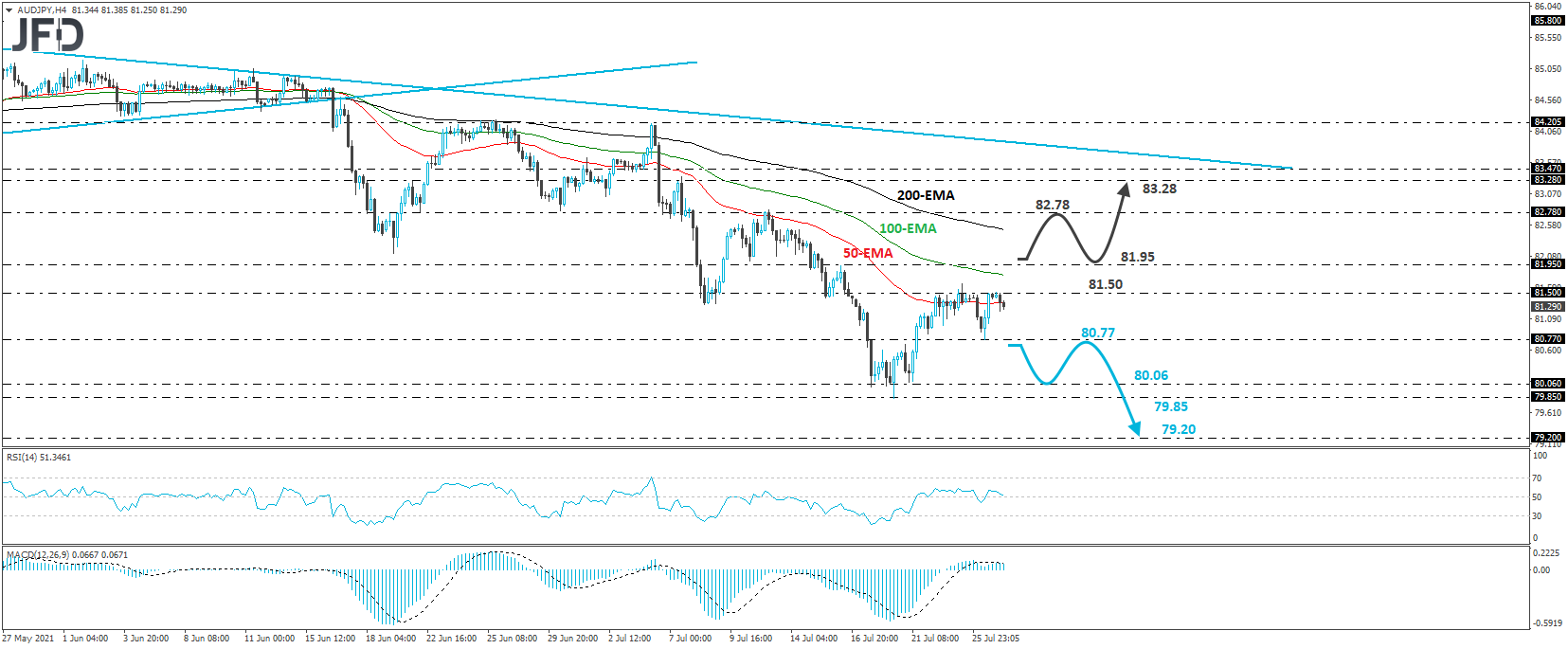

AUD/JPY – Technical Outlook

AUD/JPY traded slightly higher yesterday, after hitting support at 80.77. However, the recovery stayed limited near the 81.50 zone. Overall, the pair continues to trade well below the downside resistance line drawn from the high of May 10th, which paints a negative near- to medium-term picture.

We would expect the bears to take charge again at some point soon, but in order to get more confident on that front, we would like to see a dip below 80.77. Such a move could open the path towards the 80.06 or 79.85 levels, which acted as strong supports between July 19th and 21st. If the bears are not willing to stop there, then a break lower would confirm a forthcoming lower low and may set the stage for declines towards the 79.20 area, defined as a support by the low of January 28th.

Alternatively, a break above 81.95 could signal that there is scope for a larger correction to the upside. The bulls may temporarily gain control and drive the action up to the 82.78 hurdle, near the high of July 13th, the break of which could invide more bulls into the action and help the pair climb to the 83.28 or 83.47 levels, near the downside resistance line taken from the high of May 10th.

As for Today’s Events

As we already noted, there are no top-tier indicators on today’s agenda. We only get the US durable goods orders for June and the Conference Board consumer confidence index for July. Headline orders are forecast to slow to +2.1% mom from +2.3%, but the core rate is anticipated to have increased to +0.8% mom from +0.3%. The CB index is anticipated to have declined somewhat, to 124.1 from 127.3.

With regards to the energy market, we have the API (American Petroleum Institute) report on crude oil inventories for last week, but as it is always the case, no forecast is available.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75.05% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2021 JFD Group Ltd.