Equity markets and the commodity-linked currencies continued to slide on Wednesday, while the safe-haven yen stayed on the front foot, as risk sentiment continued to deteriorate. The Bank of Canada kept interest rates unchanged as was widely anticipated but delivered a dovish statement. As for today, focus is likely to shift to the OPEC+ meeting in Vienna.

Markets Continue in ‘Risk off’ Mode, BoC Turns Dovish

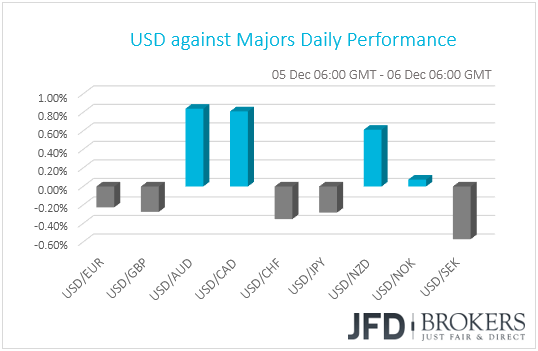

The dollar traded mixed against the other G10 currencies on Wednesday. It continued to gain against the commodity-linked currencies AUD, CAD and NZD, while it underperformed against SEK, CHF, JPY, GBP and EUR, with SEK gaining the most after Sweden’s industrial production for October accelerated notably in both monthly and yearly terms. The greenback traded virtually unchanged against NOK.

The strengthening of the safe-haven JPY and the weakening of the commodity-linked currencies suggest that market sentiment continued to deteriorate. Indeed, major EU equity indices were a sea of red yesterday, with the negative mood rolling into the Asian session Wednesday. US market remained closed to mark the day of mourning for former President George H.W. Bush. US data that were scheduled for yesterday will be released today. In our view, the catalyst behind this risk-off environment remains the combination of doubts around the US-China trade saga and fears of recession due to the inversion of the 2yr/5yr and 3yr/5yr parts of the US Treasury yield curve.

As we noted in our previous reports, the lack of clarity in the statements of the US and China after the Trump-Jinping meeting suggests that the two nations still have a long way to go before they seal a final accord. The arrest of Huawei’s CFO in Canada at the request of US authorities may have also added to fears of a revival in tensions between world’s two largest economies.

Apart from the “risk off” environment, the miss in Australia’s trade balance overnight may have also weighed on the Aussie, which was the main loser. Expectations were for the nation’s trade surplus to have increased to AUD 3.1bn in October from AUD 2.94bn in September. Instead, the figure showed a decline to AUD 2.3bn.

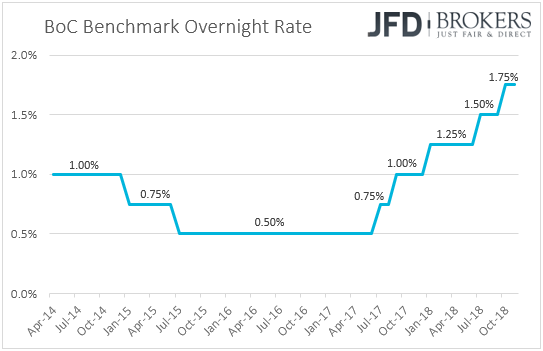

The next main loser was the Canadian dollar, which felt the heat of the BoC rate decision. As was widely expected the Bank kept interest rate unchanged at +1.75%, but the accompanying statement had a dovish flavor compared to the hawkish one we got last time.

Officials noted that that the economy grew in line with their expectations in Q3, but data suggest less momentum going into Q4. Most importantly, they said that “historical revisions by Statistics Canada to GDP, together with recent macroeconomic developments, indicate there may be additional room for non-inflationary growth”. Policy makers also noted that oil prices have fallen sharply, which will result in a materially weaker-than-expected activity in the energy sector. With regards to global trade, we believe that they appeared somewhat more concerned than previously, noting that trade conflicts are weighting more heavily on global demand.

In our view, the key takeaway from this meeting is that the economy is not as close to its potential as previously thought and this could mean slower rate increases moving forward. Following the disappointing GDP data last week, the dovish statement by the Bank of Canada may have prompted market participants to take more January-hike bets off the table. As for today, given that Canada is among the 10 largest oil producing nations in the world, CAD-traders are now likely to join oil investors in the waiting room for the outcome of the OPEC+ meeting, which begins today in Vienna (see below).

CAD/JPY – Technical Outlook

CAD/JPY tumbled yesterday, falling below the medium-term upside support line drawn from the low of the 19th of March, and then, below the key support zone of 84.65, defined by the low of the 20th of November. That said, the slide stopped near the 84.05 level, marked by the low of the 10th of September. In our view, the break below the aforementioned upside line and especially the dip below 84.65 may have turned the near-term outlook to negative. However, at this point, we have to note that a lot of this pair’s forthcoming directional wave may depend on the OPEC+ outcome.

If the bears are willing to stay in charge and drive the battle below the 84.05 level, then we may see them targeting the low of the 6th of September, at around 83.75. Another dip below 83.75 could extend the slide towards the 83.40 zone, marked by an intraday low on the 29th of June.

Shifting attention to our momentum studies, we see that the RSI entered its below-30 zone and continued drifting lower, while the MACD lies below both its zero and trigger lines, pointing down. These indicators detect strong downside speed and corroborate our view for this pair to keep trading south for a while more.

On the upside, we would like to see a clear break above 85.15 before we abandon the bearish case. Such a break could signal the rate’s return above the upside support line drawn from the low of the 19th of March and could open the path for the 85.65 zone. Another break above 85.65 could aim for the downside resistance line taken from the high of the 8th of November.

OPEC+ Group Meets in Vienna to Discuss Output

As we already mentioned, today, major OPEC and non-OPEC oil producers – known as the OPEC+ group – gather in Vienna to discuss output policy in a two-day meeting. Since the beginning of October, oil prices have been in a falling mode due to a blend of surging US production, a risk-off environment, as well as demand concerns due to slowing global growth. The fact that the US granted waivers to eight countries, letting them to continue importing Iranian oil even after it sanctioned the nation, did not help oil prices either.

Reacting to the tumble, a few weeks ago, producers signaled their willingness to reduce production in 2019, with their analysis suggesting the need for a 1mn bpd supply reduction from October levels. A couple of days later, a report citing sources familiar with the matter noted that producers were discussing the case for a 1.4mn bpd cut. As for our view, following Russia’s willingness to continue cooperating with the group, OPEC and its allies are more likely (than not) to proceed with cutting production, despite US President Trump’s warnings not to do so.

However, the market’s reaction is likely to depend on the amount producers will decide to return to the market. Currently, the information investors have in hand is a range of 1-1.4mn bpd. Therefore, anything near, or even above, the upper bound could enoucrage oil-bulls to jump back into the action and lift prices up. On the other hand, a cut near, or below, the lower end of the aforementioned range could disappoint investors and the “black gold” may resume its latest downtrend. The outcome that could work for both the group and President Trump may be near the middle of the range, as something like that could just stabilize prices somewhat. The surprise would be no cuts at all. This is where oil prices could fall sharply.

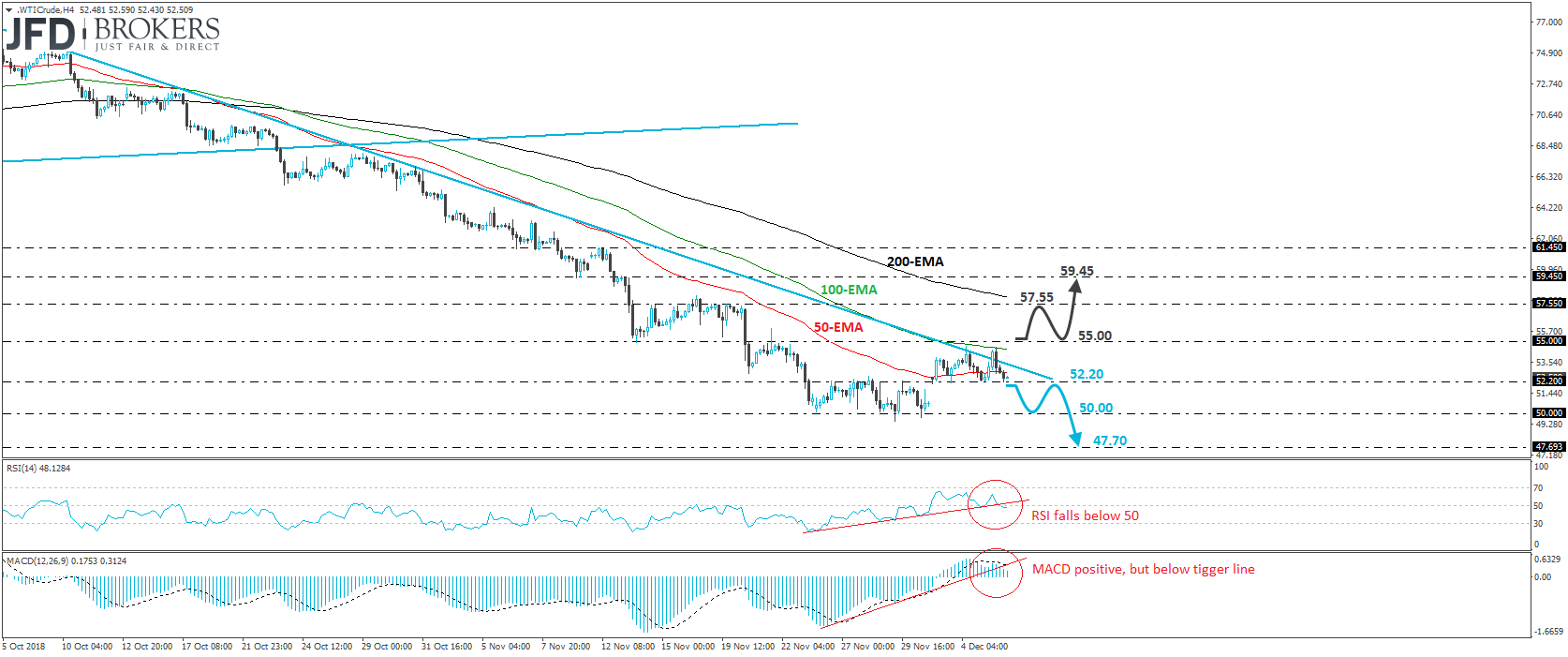

WTI – Technical Outlook

WTI moved higher yesterday, breaking briefly above the downtrend line taken from the peak of the 10th of October. However, the rebound was short-lived, with the price pulling back below the trend line. From a technical standpoint, this keeps the near-term outlook negative. However, bearing in mind that the price may stall near the line waiting for the outcome of the OPEC+ meeting, we prefer to adopt a flat stance for now.

A lower-than-expected production cut could encourage the bears to hit the trend-resumption button. WTI could fall below the 52.20 support, targeting once again the psychological zone of 50.00. Another dip below 50.00 could trigger extensions towards the 47.70 zone, defined by the lows of the 8th and 11th of September 2017. Now, in case of no cuts at all, the black liquid could tumble well below those levels.

Alternatively, if we get a larger-than-expected cut by the OPEC+ group, the bulls may get excited and drive the battle above 55.00. Something like that may confirm the upside break of the previously-mentioned downtrend line and could carry extensions towards 57.55. Another move above 57.55 may open the path for the 59.45 zone, marked by the high of the 13th of November, and the inside swing low of the 9th of that month.

As for the Rest of Today’s Events

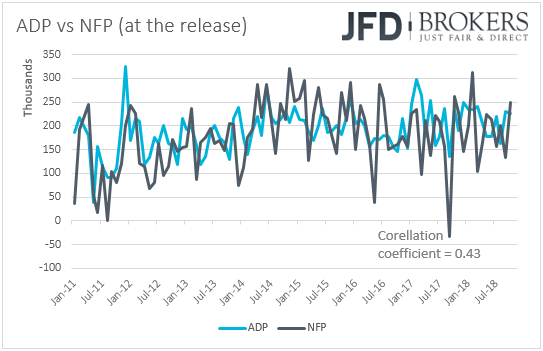

In the US, we get the ADP employment report for November. Expectations are for the private sector to have gained 196k jobs, less than the 227k in October. This could raise speculation that the NFP number, due out on Friday may also come below October’s print of 250k. Indeed, currently the NFP forecast is at 200k. However, we repeat to the umpteenth time that, even though the ADP is the only major gauge we have for the non-farm payrolls, the correlation between the two time-series at the time of the release (no revisions are taken into account) has been very low in recent years. Taking into account data from January 2011, this correlation stands at 0.43. The final Markit services and composite PMIs for November, the ISM non-manufacturing index for the month, as well as the nation’s trade data for October, are also due to be released.

We get October trade data from Canada as well, and expectations are for the country’s trade deficit to have widened. Canada’s Ivey PMI for November is also coming out and is expected to have declined to 60.3 from 61.8.

As for the speakers, we have two on the agenda: BoC Governor Poloz and Atlanta Fed President Raphael Bostic.

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.