The dollar stayed on the back foot against most of the other G10 currencies yesterday, extending the slide triggered by the dovish comments of Fed Chair Powell on Friday. Equities strengthen on his remarks, accelerating the recovery initiated by the US jobs data. As for today, focus remains on the US-China trade talks for headlines on how close to an accord the two sides are.

Dollar Offered and Equities Supported After Powell’s Remarks

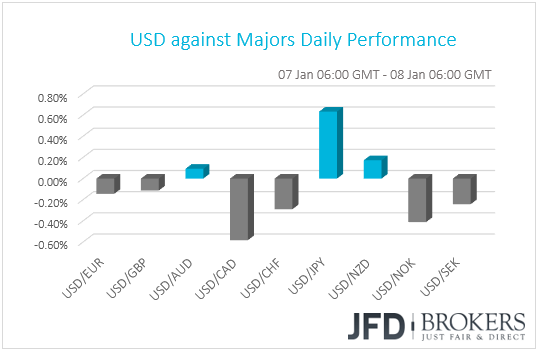

The dollar tumbled against almost all the other G10 currencies on Friday and continued to do so against most of them on Monday. It gained only against JPY, and slightly against NZD, while it traded nearly unchanged against AUD. The greenback lost the most ground against CAD, NOK and CHF.

With no major news to revive the dollar’s appeal, the US currency continued trading lower on Monday, albeit at a slower pace than on Friday. Major EU indices traded somewhat lower, but we would treat that as a corrective setback and not a reversal in the broader market sentiment. After all, US indices closed in the green, while Asian markets finished today’s session positive as well.

On Friday, the highlights were the US jobs data for December and Fed Chair Powell’s remarks in a discussion with former Fed Chairs Janet Yellen and Ben Bernanke at the American Economic Association Meeting in Atlanta. The jobs report showed stellar employment gains and accelerating wages. The unemployment rate increased, but given that the participation rate rose as well, this may have been due to more people entering the labor force. The result was a higher dollar and a rally in equity markets. Remember that on Friday, we noted that bearing concerns over the health of the US economy, market participants may focus more on the NFP print instead of wage growth as was the case a few months ago.

However, the joy for dollar bulls did not last for long. The currency gave back all its NFP-related gains to trade even lower, while equity markets accelerated to the upside following dovish comments by Fed Chair Jerome Powell. Powell said that the Fed would be patient and flexible with regards to future interest rate moves, watching how the economy evolves. He also noted that officials are listening carefully to the messages market participants are sending. Although the employment data encouraged market participants to price out the chance for a rate cut throughout the year, from 40% after the disappointment in the ISM manufacturing PMI to around 15%, Powell’s comments did not leave any room for pricing in any rate hikes.

Having said all these though, even if the dollar continues to slide in the near-term due to expectations that the Fed may pause its tightening cycle this year, we still view the risks surrounding its somewhat longer-term performance as tilted to the upside. With the Fed’s “dot plot” pointing to 2 hikes throughout the year, data suggesting that the economy is not slowing as many are afraid, may prompt investors to start bringing their expectations closer to the Fed’s.

The big question is how equity markets will perform. Will they continue rising on signs that the economy is doing well, or will they slide on fears that the Fed will appear more upbeat and eventually refrain from taking a break this year? After all, Powell did not say that the Fed is done hiking rates. He said that any future policy moves will be more data dependent. Thus, data suggesting that inflation may start picking up steam again could revive such concerns. Let’s not forget that the employment report showed wages accelerating to +3.2% yoy, which could lead to higher inflation in the not-too-distant future.

US-China Trade Talks in the Limelight

For now, we believe that equity markets are likely to be more sensitive to headlines surrounding the US-China trade talks, which began yesterday. Both sides have shown their willingness to reach consensus on the matter recently, with US President Trump sounding optimistic on Sunday and noting that the weakness in the Chinese economy is a reason for the nation to work towards a deal. What’s more, US Commerce Secretary Wilbur Ross said yesterday that there is a good chance for the two nations to reach an accord, while China’s Foreign Ministry noted that China has the “good faith” to work things out.

Thus, more headlines pointing to that direction may calm further investors nerves and equities are likely to extend their recent gains. However, we are still skeptical as to whether a final accord can be agreed today. Even though China’s Vice Premier Liu He, who is a top economic advisor, unexpectedly joined the talks yesterday, there are still major issues unresolved. We believe that these negotiations may open the way for more talks, with the next round perhaps taking place at the World Economic Forum in Davos later this month, between US President Trump and China’s Vice President

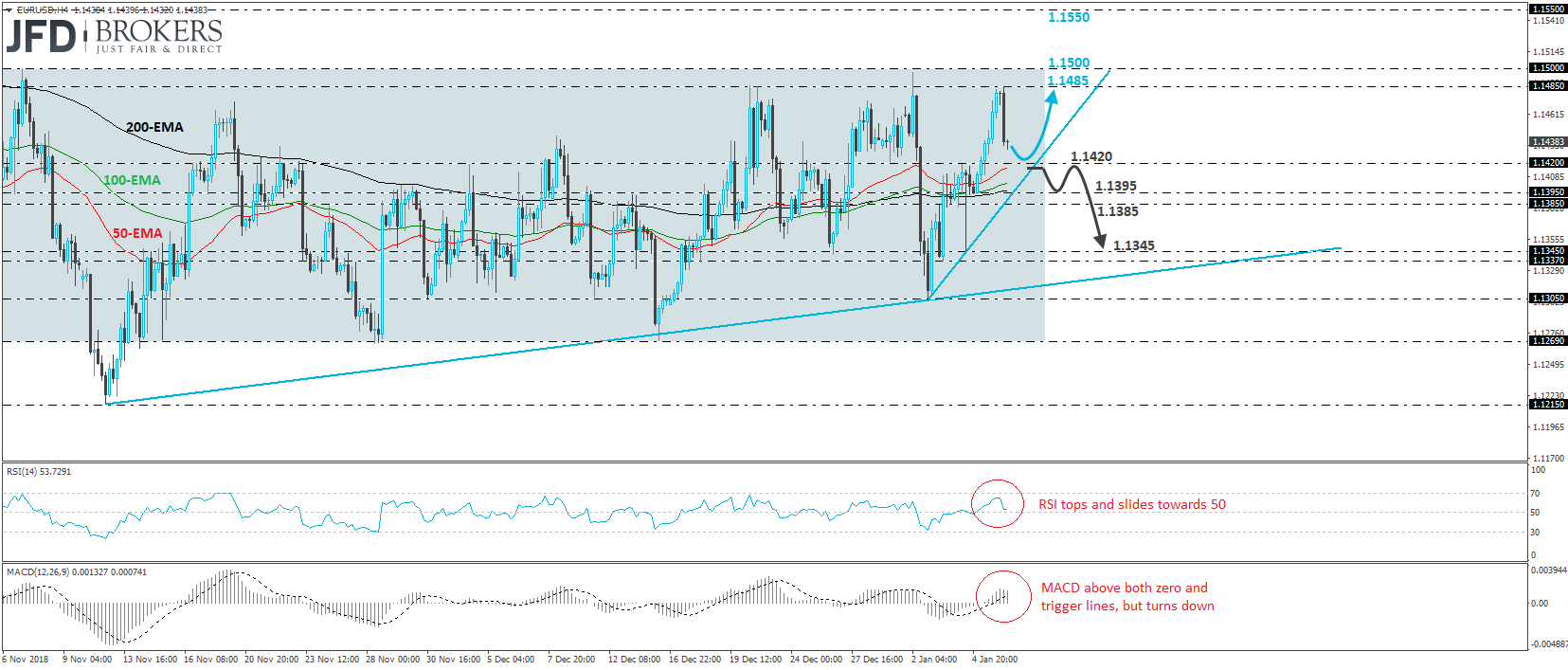

EUR/USD – Technical Outlook

EUR/USD continued trading higher on Monday but hit resistance at 1.1485 during the Asian morning today and retreated. Overall, the pair keeps trading within the sideways range between 1.1270 and 1.1500, which has been containing most of the price action since the 22nd of October and thus, we would consider the medium-term outlook to be neutral. That said, bearing in mind that the rate is trading above a short-term upside support line drawn from the low of the 2nd of January, we see the case for another rebound, at least within the range.

If the bulls are strong enough to take the reins again soon, then we may see them aiming for another test near the 1.1485 zone, the break of which could target the upper bound of the aforementioned range, which is the psychological barrier of 1.1500. That said, we would like to see a decisive move above that key hurdle before we get confident on larger extensions. Such a break may allow the bulls to put the 1.1550 zone on their radars, a resistance marked by the high of the 22nd of October.

Shifting attention to our short-term momentum indicators, we see that the RSI topped slightly below 70, while the MACD, although above both its zero and trigger lines, has topped as well. Therefore, we would stay cautious that some further retreat may be on the cards before the bulls decide to shoot again, perhaps for the rate to test the 1.1420 zone as a support this time.

On the downside, we would like to see the rate breaking below 1.1420, as well as below the aforementioned short-term upside line before we start looking for lower levels within the broader range. Something like that could open the way for the 1.1395 or the 1.1385 zones, with the break of the latter having the potential to trigger declines towards Friday’s low of around 1.1345.

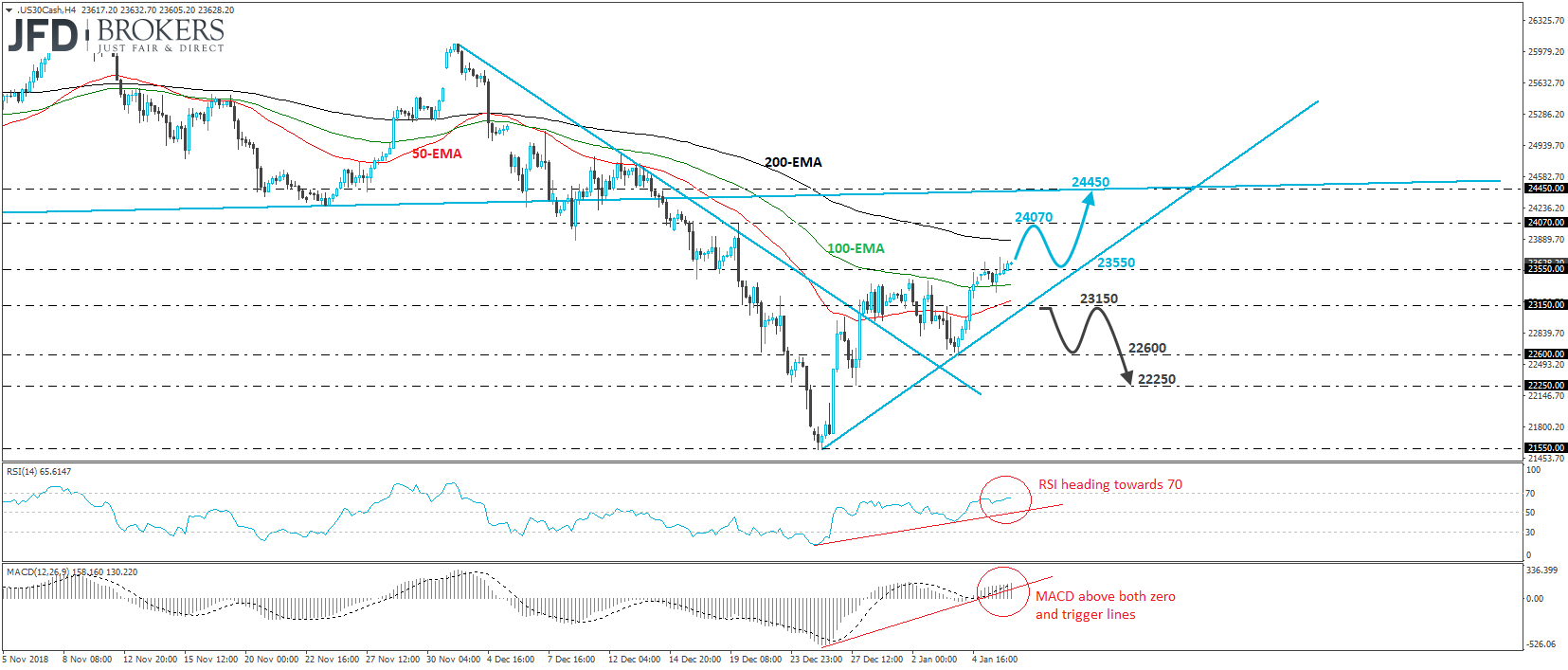

DJIA – Technical Outlook

The Dow Jones Industrial Average cash index traded somewhat higher yesterday, breaking slightly above the 23550 resistance hurdle. With the index trading above the short-term upside support line taken from the low of the 26th of December, as well as above the prior downside resistance line drawn from the peak of the 3rd of December, we believe that there is room for some further recovery. That said, bearing in mind that the index remains below the prior longer-term upside support line taken from the low of the 6th of February 2018, any further advances may stay limited.

We believe that the move above 23550 may have opened the path for our next resistance hurdle, at around 24070, defined by the peak of the 19th of December. Another break above that barrier could allow the bulls to drive the battle even higher and perhaps aim for the aforementioned prior longer-term upside support line, or the 24450 zone, defined by the inside swing low o f the 13th of December.

Taking a look at our short-term oscillators, we see that the RSI remains above its upside support line and looks to be heading towards its 70 line. The MACD also stands above its respective upside support line, as well as above both its zero and trigger lines. These indicators detect upside momentum and corroborate our view for some further short-term advances.

On the downside, we would like to see a decisive dip back below 23150 before we start examining whether the bulls have abandoned the battlefield, at least in the near term. Such a dip could also confirm the break below the short-term upside support line drawn from the low of the 26th of December and may pave the way towards the low of the 4th of January, at around 22600. Another break below that obstacle could extend the slide towards the 22250 zone, near the low of the 27th of December.

As for Today’s Events

Apart from any headlines surrounding the US-China sequel, we will also be watching carefully for any news surrounding the Brexit front as the Parliamentary debate over May’s deal is scheduled for this week, with the vote set to take place next week. Meanwhile, with fears that a deal is unlikely to be approved by the official divorce date, which is on the 29th of March, UK and EU officials are discussing the possibility of an extension, according to the Daily Telegraph.

In terms of data releases, we get trade data for November from the US and Canada. The US trade deficit is expected to have narrowed to USD 54.00bn from USD 55.50bn, while the Canadian deficit is forecast to have widened to CAD 1.95bn from CAD 1.17bn. We also get the US JOLTs Job Openings for November, which are expected to have risen to 7.170mn from 7.079mn in October.

With regards to the energy market we have the API (American Petroleum Institute) weekly report on crude oil inventories, but as it is always the case, no forecast is available.

As for tonight, during the Asian morning Wednesday, Australia’s building approvals and Japan’s average cash earnings are scheduled to be released. Australia’s building approvals are expected to have slid in November, but at a slower pace than in October, while Japan’s earnings are expected to have slowed to +1.3% yoy from +1.5% yoy, which could increase concerns over whether Japan’s inflation can eventually pick up some steam soon. With all Japanese inflation metrics well below the BoJ’s objective of 2%, we stick to our longstanding view that BoJ officials have still a long way to go before they start considering a meaningful step towards normalization, especially following the latest appreciation of the yen.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Group, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Group analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD Group prohibits the duplication or publication without explicit approval.

68% of the retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2019 JFD Group Ltd.