Following a week packed with central bank decisions, the torch will be now passed to the RBNZ. When they last met, policymakers of this Bank decided to cut interest rates by 50bps and kept the door open for more reductions. However, we don’t expect them to deliver one this week. As for the data, Eurozone’s preliminary PMIs for September and the US core PCE index for August are due to be released.

Monday is a PMI day! During the European morning, we get the preliminary prints for September from several European nations and the Eurozone as a whole. The bloc’s manufacturing index is expected to have risen somewhat, but to have stayed within the contractionary territory. Specifically, it is expected to have increased to 47.3 from 47.0. The services one is expected to have slid to 53.3 from 53.5. Something like that would keep the composite PMI unchanged at 51.9.

At its previous meeting, the ECB cut its deposit rate by 10bps and decided to restart its QE program, with President Draghi adding that the Governing Council “continues to stand ready to adjust all of its instruments as appropriate to ensure that inflation moves towards its aim in a sustained manner.” However, although the Bank remains ready to ease further if needed, at the press conference, Drahgi stressed the need for governments with fiscal space to act in an effective and timely manner. “Now it’s high time I think for the fiscal policy to take charge,” the President said. Thus, another round of soft PMIs would increase further the need for fiscal support.

We get preliminary Markit PMIs for September from the US as well. The manufacturing index is expected to have held steady at 50.3, while the services one is anticipated to have risen to 51.5 from 50.7. Strangely though, the composite PMI is forecast to have slipped into contractionary territory. Specifically, it is expected to have declined to 49.6 from 50.7. That said, we believe that the market tends to pay more attention to the ISM indices, which are scheduled to be released on October 1st and 3rd.

On Tuesday, the calendar is relatively light. The only releases worth mentioning are the German Ifo survey, and the US Conference Board consumer confidence index, both for September. With regards to the German Ifo survey, the current assessment index is expected to have declined to 97.0 from 97.3, while the business expectations one is forecast to have risen to 91.8 from 91.3. This would drive the business climate index slightly up, to 94.5 from 94.3. The case for a lower current assessment index and higher business expectations is supported by the ZEW indices which moved in a similar fashion. Namely, the current conditions ZEW index slid more than anticipated, while the economic sentiment one rose more than expected. As for the US CB consumer confidence index, it is forecast to have slid to 134.0 from 135.1.

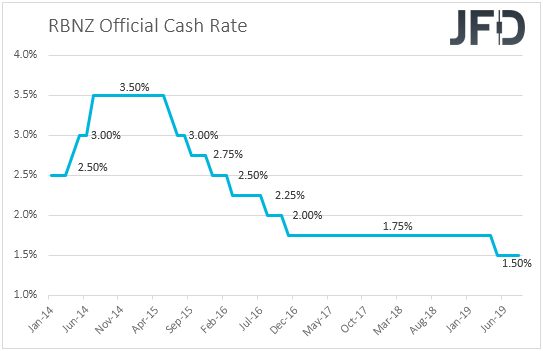

On Wednesday, during the Asian morning, the RBNZ will announced its monetary policy decision. When they last met, policymakers of this Bank decided to cut interest rates by 50bps, to a record low of 1.00%, surprising the financial community which has been positioned for a 25bps decrease. The key takeaway we got from the statement and the minutes was that officials remained willing to ease further if needed, and this was made crystal clear by Governor Adrian Orr at the press conference following the decision.

Last week, data showed that New Zealand’s economy slowed to +0.5% from +0.6%, which was better than the +0.4% forecast, but in line with the Bank’s latest projection for the quarter. In our view, this keeps the door for more easing in the months to come open. That said, we don’t expect officials to rush into cutting again at this meeting. In an interview from the Jackson Hole economic symposium in the end of August, Governor Orr said that the prior “double cut” lowers the chances of having to do more later, which suggests that there is no urgency for delivering another cut for now. Indeed, this appears to be the view held by the financial world as well. According to New Zealand’s OIS (Overnight Index Swaps), the probability for a 25bps cut this week stands at around 26%.

As for Wednesday’s data, apart from the RBNZ policy decision, during the Asian morning, we also get New Zealand’s trade balance for August, with the nation’s deficit expected to have widened. Later in the day, the US new home sales for the same month are forecast to have rebounded 3.9% after tumbling 12.8% in July.

On Thursday, the final US GDP for Q2 is due to be released and it is expected to confirm its second estimate, namely that the economy slowed to +2.0% qoq SAAR from +3.1% in Q1. Having said that, we expect the release to pass largely unnoticed. We are running the final days of Q3 and there are models already pointing to how the economy may have performed during this quarter. The Atlanta Fed GDPNow model estimates that growth in Q3 is +1.9% qoq SAAR, while the New York Nowcast points to a 2.24% qoq SAAR growth rate. Pending home sales for August are also coming out and the forecast suggests a 1.0% mom rebound after a 2.5% slide in July.

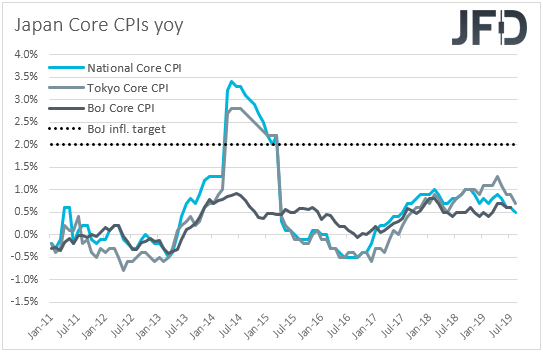

Finally, on Friday, during the Asian morning, Japan’s Tokyo CPIs for September are due to be released. The headline rate is forecast to have increased to +0.8% from +0.6%, while the core one is anticipated to have ticked down to +0.6% yoy from +0.7%. This could raise speculation that the National rates for the month may move in a similar fashion.

At last week’s gathering, the BoJ decided to keep its ultra-loose policy and forward guidance unchanged, disappointing those who expected some form of easing, or at least a more dovish language. That said, the Bank added that it would pay closer attention to the possibility of losing its momentum towards hitting its inflation aim, and that they will reexamine developments at their next meeting. Thus, with inflation staying stubbornly well below the Bank’s objective of 2%, the probability for additional easing soon is likely to increase.

Later in the day, from the US, we get durable goods orders, personal income and spending, as well as the core PCE index, all for August. With regards to durable goods orders, the headline rate is expected to have slid to -1.2% mom from +2.0% in July, but the core one is expected to have risen to +0.2% mom from -0.4%. Personal income is expected to have accelerated to +0.4% mom from +0.1%, which is somewhat supported by the uptick in the earnings mom rate for the month, while spending is expected to have slowed to +0.3% mom from +0.6%. The case for a slowdown in spending is supported by the slowdown in retail sales.

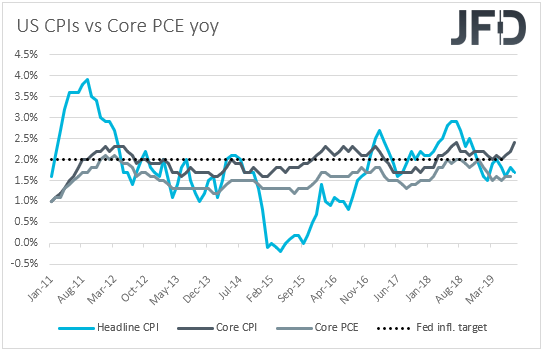

Now, as far as the core PCE index is concerned, the Fed’s favorite inflation gauge, it is expected to have accelerated to +1.8% yoy from +1.6%, something supported by the core CPI rate for the month, which rose to +2.4% from +2.2%. Last week, the Fed decided to lower interest rates by 25bps, but the new “dot plot” pointed to no more cuts this year and the next, one hike in 2021 and another one in 2022. That said, despite the 2019 median dot suggesting that there are no more rate reductions on the table, the Committee was largely divided, with only 5 members supporting that view. Seven still believed that another quarter-point reduction may be appropriate, while the remaining 5 argued that last week’s cut was not needed.

Having all this in mind, a rising core PCE rate could add to the case that no more cuts are needed this year, but in our view, a lot on that front will depend on how the US-China trade sequel unfolds. Despite not providing clear signals with regards to further rate reductions last week, the Fed may be forced to cut again in the months to come if tensions between the world’s two largest economies escalate again.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

75% of the retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.