We have a light week ahead of us in terms of scheduled economic releases and events, but we do get a couple of important ones. First of all, we have an RBNZ monetary policy decision on Wednesday, where, following the latest better-than-expected employment data, it would be interesting to see whether officials will sound a bit more optimistic. In the US, we will get to hear from several Fed speakers, while on Friday, the Fed’s favorite inflation metric, the core PCE index is due to be released. Both are likely to set the tone as to whether the Fed should consider to start normalizing policy sooner than previously anticipated, or not.

Monday appears to be a relatively light day in terms of economic data and releases. Stock markets in Germany, Switzerland and Norway will stay closed in celebration of the Pentecost, while Canada will be on holiday as well due to the Victoria Day.

We believe that in the absence of any important data, market attention may fall on comments and remarks by Fed officials. Today, we will get to hear from Atlanta Fed President Raphael Bostic and Fed Board Governor Lael Brainard. Following the surge in both the headline and core inflation rates in the US, as well as the taper talk revealed in the minutes of the latest FOMC gathering, it would be interesting to see what they have to say. Maybe those two members were initially in the camp supporting that it is too early to start discussing policy normalization, but after the surge in inflation, especially the underlying forces, they may have changed their mind. Let’s not forget that just after the CPI data were out, Bostic noted that it’s too soon to judge whether the inflation trend is worrisome, avoiding to say confidently that the surge is due to transitory factors. If we do indeed get more skeptical views on the inflation and taper front, equities may pull back again, while the US dollar could rebound. On the other hand, anything suggesting that officials still see the inflation spike as temporary and that we still have a long way to go before the Committee starts normalizing policy, could have the opposite effect, namely, equities are likely to march north and the US dollar, as well as other safe havens may slide.

On Tuesday, during the Asian morning, we get the BoJ’s core CPI for April, but as it is always the case, no forecast is available. Later in the day, we get Germany’s final GDP for Q1, which is expected to confirm its preliminary estimate of a 1.7% qoq contraction. The nation’s ZEW survey for May is coming out as well. The current assessment index is forecast to have risen to 95.5 from 94.1, while the business expectations one is anticipated to have inched up to 101.0 from 99.5. This is likely to take the business climate index up to 98.1 from 96.8, thereby confirming that Eurozone’s growth engine continues to recover from the coronavirus-related damages at a decent pace. European shares and the euro may climb higher, but we doubt that this could raise speculation that the ECB will start withdrawing monetary policy anytime soon. After all, last Tuesday, President Lagarde confirmed that clearly, saying that it is “essential that monetary and fiscal support are not withdrawn too soon”.

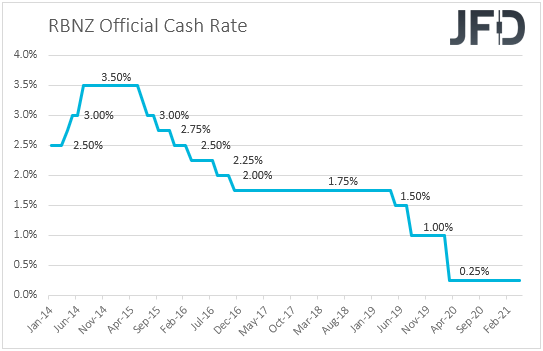

On Wednesday, the highlight on the agenda may be the RBNZ decision, scheduled during the Asian trading. At its latest gathering, this Bank kept its policy settings untouched, with policymakers maintaining the position that they are prepared to lower the OCR further if required, and adding that a prolonged period of time is most likely to pass before their objectives are met. Since then, New Zealand’s CPI ticked up to +1.5% yoy from +1.4%, but, although this is a move in the desired direction, it is still below the midpoint of the Bank’s 1-3% range. However, the employment report for Q1 came in better than expected, which may have lessened the likelihood for further interest-rate reductions. Thus, even if policymakers keep the door open for such an action, we believe that they may sound a bit more optimistic than previously, giving the impression that this is not something that will happen in the months to come if the economy continues to improve. A more optimistic language may help the Kiwi recover some of its recently lost ground.

On Thursday, the only items worth mentioning are the second estimate of the US GDP for Q1, which is expected reveal a small upside revision, to +6.5% qoq SAAR from +6.4%, as well as the durable goods orders for April. Both headline and core sales are expected to have slowed to +0.7% mom, from +1.0% and +2.3% respectively.

Finally, on Friday, Asian time, the Tokyo CPIs for May are due to be released, alongside Japan’s employment report for April. No forecast is available for the headline rate, while the core one is anticipated to have stayed unchanged at -0.2% yoy. The unemployment rate is expected to have ticked up to 2.7% from 2.6%, while the jobs-to-applications ratio is forecast to have held steady at 1.10.

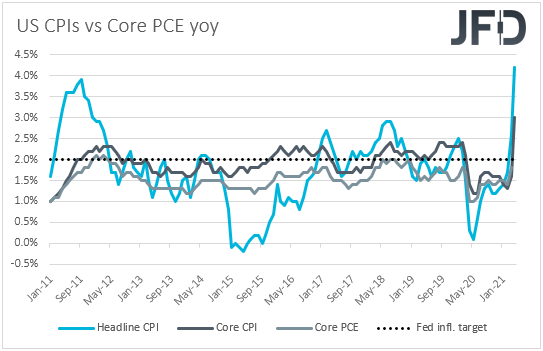

Later in the day, we get the US personal income and spending data for April, alongside the yoy core PCE rate for the month. Personal income is expected to have declined 14.8% mom after surging 21.1% in March, while spending is forecast to have slowed to +0.5% mom from +4.2%. The yoy core PCE rate, which is the Fed’s favorite inflation metric, is anticipated to have surged to +3.0% yoy from +1.8%, adding to fears that the latest spike in inflation may not be due to transitory factors. This may increase speculation that the Fed will need to start considering policy normalization sooner than previously thought and may have a negative impact on equities and other risk-linked assets. At the same time, the US dollar and other safe havens may strengthen.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75.05% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2021 JFD Group Ltd.