This week, we have three central banks deciding on interest rates: the RBA, the Riksbank and the BoC. All three Banks are anticipated to keep their rates unchanged, so attention is likely to fall on the accompanying statements for clues on their future plans. On Friday, the US and Canadian employment reports are due to be released.

On Monday, markets in the US and Canada will be closed in celebration of the Labor Day.

During the European morning, we get the final manufacturing PMIs for August from several European countries, as well as the Eurozone as a whole. As usual, the final prints are expected to confirm their preliminary estimate.

We get manufacturing PMI data for August from the UK as well and expectations are for a tick down to 53.9 from 54.0. Usually the market pays more attention to the services index, due out Wednesday, given that the service sector accounts for around 80% of the UK GDP. That said, with any BoE hike expectations well pushed into next year, we expect this round of PMIs to attract less attention than usual.

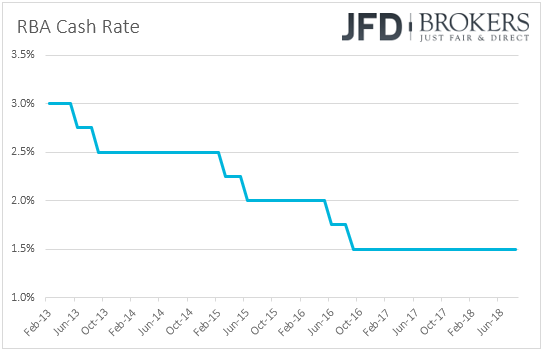

On Tuesday, during the Asian morning, the RBA decides on interest rates, but once again on fireworks are expected. The RBA has kept interest rates unchanged since August 2016, and it is expected to do so at this gathering as well. Actually, according to the Bank’s latest quarterly Statement on Monetary Policy, financial market prices imply that the cash rate is expected to increase around the end of next year. What’s more, on Wednesday, Westpac decided to increase its standard variable rate by 14bps, effective on the 19th of September, something that represents a tightening in financial conditions and could delay the RBA from hiking even further. Australia’s current account balance for Q2 is also coming out.

During the European morning, we get Switzerland’s CPI for August. Expectations are for the Swiss inflation rate to have remained unchanged at +1.2%. Although this is above the SNB’s inflation projections for Q3, it is still distant of the Bank’s 2% objective. According to their latest projections, SNB policymakers, expect inflation to exceed their target in Q1 2021, conditional upon interest rates staying at current levels over the entire forecast horizon. Thus, even if inflation accelerates somewhat, we don’t expect this to alter expectations around the SNB’s thinking, especially if we take into account the latest strength of the Swiss franc.

In the UK, BoE Governor Mark Carney and several other MPC members will testify on the August Inflation Report before the Parliament’s Treasury Committee. As for the UK indicators, we get the construction PMI for August, which is forecast to have declined to 54.9 from 55.8.

In the US, the final Markit manufacturing PMI for August, as well as the ISM manufacturing index for the month are coming out. The final markit print is forecast to confirm its preliminary estimate, while the ISM index is anticipated to have declined to 57.6 from 58.1.

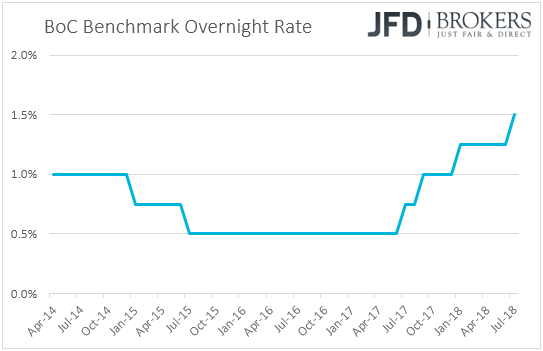

On Wednesday, the highlight is likely to be the BoC interest rate decision. At their latest policy meeting, BoC officials decided to raise interest rates to +1.50% from +1.25%, and maintained a hawkish stance, noting that they will continue to take a gradual approach on interest rates, guided by incoming data.

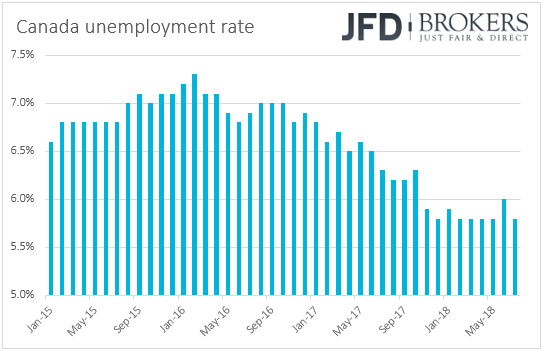

Since then, most Canadian economic data have been more than encouraging. Both headline and core inflation metrics accelerated more than anticipated in July, while the unemployment rate for the same month slid to 5.8% from 6.0% in June. As for economic growth, it accelerated to +2.9% qoq from +1.3% qoq on an annualized basis but fell just shy of the +3.0% estimate. Meanwhile, June’s monthly rate fell to 0.0% from +0.5% in May. Although the quarterly data suggests the fastest pace in one year, this may have not been enough to bolster expectations that the BoC will proceed with hiking rates at this meeting.

We agree with the consensus for no September hike. Officials just raised rates at their prior meeting and they may prefer to wait for more evidence before pushing the hiking button again, perhaps in October. What’s more, on Friday, talks between the US and Canada over NAFTA ended without a deal, which keeps uncertainty over the matter elevated. Even though chances for a deal are not wiped out entirely, we believe that Poloz and his colleagues may prefer to wait for the dust around NAFTA to settle down before acting again.

As for Wednesday’s indicators, during the Asian morning, Australia’s GDP for Q2 is due to be released. Expectations are for the quarterly rate to have declined to +0.8% from +1.0%, something that could bring the yoy rate down as well, to +2.8% from +3.1%. China’s Caixin services PMI for August is also coming out.

During the European day, we get the final services and composite PMIs for August from the European nations of which we get manufacturing data on Monday. The UK services PMI for the month is coming out as well and expectations are for the index to have risen to 53.9 from 53.5.

With regards to the trade front, the public-comment period with regards to the US tariffs on USD 200bn worth of Chinese imports concludes. Last Thursday, reports suggested that President Trump could proceed with the imposition of those tariffs as soon as the hearings are over and thus, it would be interesting to see whether this is the case.

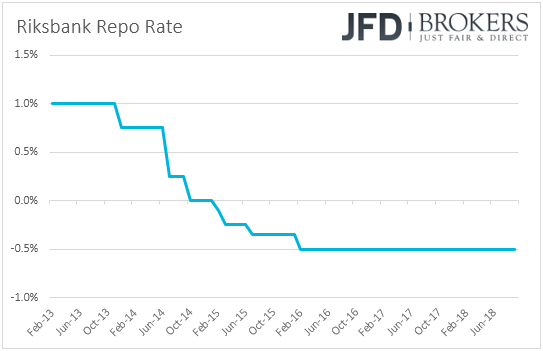

On Thursday, it is the turn of the Riksbank to decide on monetary policy. At its latest gathering, the Bank kept interest rates untouched and maintained the view that slow repo rate rises will be initiated towards the end of the year. However, apart from the usual dissenter, Deputy Governor Ohlsson, who supported raising rates at that meeting, Deputy Governor Martin Floden advocated for a raise as early as in September.

Latest inflation data showed that the headline CPI accelerated to +2.1% yoy in July from +2.0% in June, while the CPIF rate stayed unchanged at +2.2% yoy, above the midpoint of the Bank’s variation band of 1-3%. However, the core CPIF inflation metric, which excludes energy, slowed further, to +1.3% yoy. Thus, having that in mind, we see it very unlikely for Swedish policymakers to push the hiking button at this meeting. On the contrary, we see a decent likelihood for them to push further back the timing of when they expect interest rates to start rising.

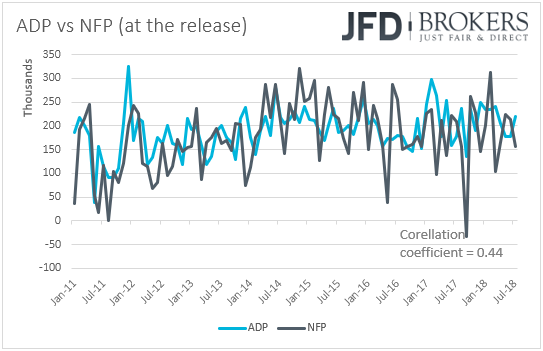

From the US, we get the ADP employment report for August. Expectations are for the private sector to have gained 189k jobs, following July’s 219k. This could increase bets that the NFP number, due to be released the following day, may come near its forecast, which is 191k. That said, we must repeat that even though the ADP is the only major gauge we have for the non-farm payrolls, the correlation between the two time-series at the time of the release (no revisions are taken into account) has been very low in recent years. Taking into account data from January 2011, the correlation stands at around 0.44.

As for the rest of the US indicators, the Unit Labor Costs index for Q2 is forecast to have declined for the second consecutive quarter. Specifically, expectations are for a 0.7% qoq slide, following a 0.9% fall in Q1. The final Markit services and composite PMIs for August are also coming out, as well as the ISM non-manufacturing index for the month.

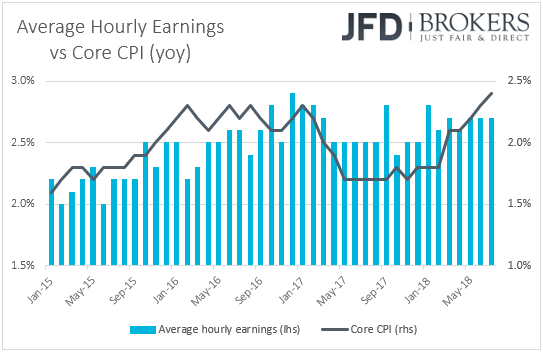

Finally, on Friday, the highlight is likely to be the US employment report for August. The forecasts suggest that non-farm payrolls have risen 191k, after July’s increase of 157k. The unemployment rate is expected to have remained unchanged at 3.9%, a tick above its 18-year low of 3.8%, while average hourly earnings are anticipated to have risen 0.3% mom, the same monthly pace as in July. Barring any revisions to the prior monthly prints, this could drive the yoy rate up to +2.8%, as the August 2017 monthly rate that will drop out of the yearly calculation was +0.2% mom.

Overall, the forecasts suggest that we are likely to get another decent report. Once again, barring any major deviation of the NFP print from its forecast, we expect the market response to be dictated by the earnings growth. Accelerating wages could raise bets of accelerating inflation in the near future and thereby strengthen further the case for two more Fed hikes this year. According to the Fed funds futures, the market is almost certain that the Committee will proceed with its next rate increase in September, while there is a 70% chance for another one in December.

We get employment data for August from Canada as well. Expectations are for the unemployment rate to have ticked back up to 5.9% from 5.8%, while the net change in employment is forecast to show that the economy added only 5k jobs but given that this is after July’s stellar print of 54.1k, it appears normal to us. Overall, we see it as a decent report, which conditional upon a hawkish BoC on Wednesday could keep expectations with regards to an October hike elevated.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.