This week, the economic calendar includes the minutes from the latest RBA, Fed and ECB policy meetings. Market attention is also likely to fall on the new round of the US-China trade talks, as well as the Jackson Hole Economic Symposium.

On Monday, we have no major events or indicators scheduled on the economic agenda.

On Tuesday, during the Asian morning, we get the minutes from the latest RBA policy gathering. The RBA has kept interest rates unchanged since August 2016, and its latest meetings have proven non-events, with the Aussie staying unfazed at the announcements. At the latest gathering, the Bank made some minor changes in the accompanying statement, but that was not enough to move the Aussie. What’s more, in the quarterly Statement on Monetary Policy that was published a couple of days after the meeting, it was noted that financial market prices imply that the cash rate is expected to increase around the end of next year, compared to mid-2019 as it was pointed out in the May report. So, with the Bank proceeding with no material changes to its language, and with expectations for a rate increase so distant, we don’t expect to get any fireworks from the minutes.

On the trade front, according to last week’s reports, US and China are expected to begin a round of two-day talks, just before Thursday, when tariffs on USD 16bn worth of products targeted by each country go into effect. Although the market reacted positively on the news that the two sides are willing to return to the negotiating table, market chatter suggests that some are worried that the talks may not bear fruit, given that they involve lower-level officials and that the gap between the two nations is still big.

On Wednesday, we get the minutes of the latest FOMC monetary policy meeting. At that meeting, the Committee decided to keep interest rates unchanged as was widely anticipated, while it made a small change to the accompanying statement. Officials noted that economic activity has been rising at a “strong rate”, instead of “solid rate” as was included in the previous statement.

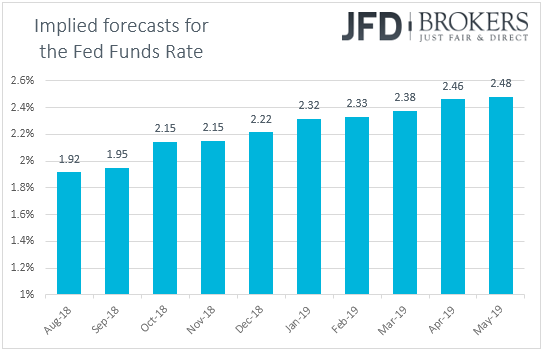

The market reaction was muted back then as the outcome was largely expected. The Committee stood pat but kept the door wide open for two more hikes by the end of the year. According to the Fed funds futures, the market implies a 96% probability for the next rate increase to occur in September, while there is a 66% chance for another one in December. We don’t expect the minutes to paint a different picture than the statement did and thus, any reaction in the greenback is likely to stay limited on this event as well.

As for the rest of Wednesday’s events, in the Asian morning, we get New Zealand’s retail sales for Q2, while during the European session, BoE Governor Mark Carney and several other MPC members will testify on the August Inflation Report before Parliament’s Treasury Committee.

Later in the day, we have the US existing home sales for July and Canada’s retail sales for June. Expectations are for the US existing home sales to have rebounded 0.8% mom after falling -0.6% in June, while Canada’s retail sales for June are expected to have slowed in both headline and core terms. Specifically, headline sales are anticipated to have slowed to +1.1% mom from +2.0%, while the core-sales rate is expected to have declined to +0.7% mom from +1.4%.

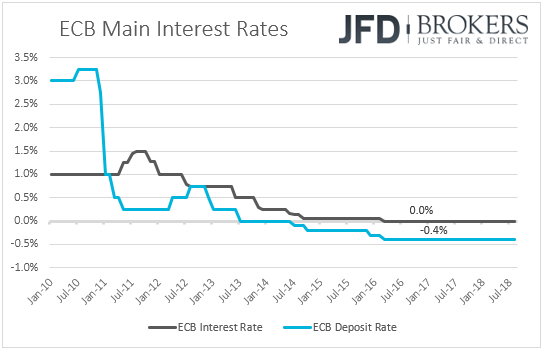

On Thursday, the ECB takes its turn in releasing the minutes of its latest policy gathering. At that meeting, President Draghi noted that expectations of the future rate path were very well aligned with the anticipation of the Governing Council, backing the market consensus for a hike in late 2019. This may have come as a disappointment to those expecting to hear that summer months are also candidates for a rate hike.

Although following the June meeting, a report noted that officials are split over when they may hike rates, with some saying that July 2019 should not be ruled out, the minutes of that meeting showed that policymakers were unanimous to support the policy proposals. Thus, we see it very unlikely that these minutes will reveal any divisions among the Governing Council.

During the European morning, we get preliminary manufacturing and services PMIs for August from several European nations and the Eurozone as a whole. The bloc’s manufacturing index is anticipated to have declined to 54.6 from 55.1 in July, while the services one is expected to have risen to 55.0 from 54.2. This will push the composite index a tick higher, to 54.4 from 54.3.

In the US, the Fed’s annual Economic Policy Symposium at Jackson Hole begins. It is an economic symposium attended by central bankers, finance ministers and academics from around the globe. This year, the theme will be “Changing Market Structure and Implications for Monetary Policy”. Fed Chair Jerome Powell is scheduled to step up to the rostrum on Friday to speak on “Monetary Policy in a Changing Economy”.

As for the US indicators, we get the preliminary Markit manufacturing and services PMIs for August. The manufacturing index is anticipated to have slid to 55.1 from 55.3 the previous month, while the services PMI is expected to have ticked down to 55.9 from 56.0. New home sales for July are also due to be released.

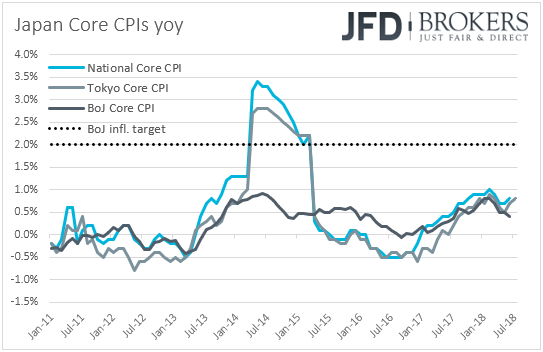

Finally, on Friday, during the Asian morning, we get Japan’s National CPIs for July. No forecast is currently available for the headline rate, while the core one is anticipated to have remained unchanged at +0.8% yoy. That said, bearing in mind that both the headline and core Tokyo CPIs for the month accelerated, to +0.9% yoy and +0.8% yoy from +0.6% and +0.7%, we see the case for the national figures to follow suit.

However, even if the National CPIs accelerate somewhat they would still stand well below the Bank’s 2% objective. Even the Bank’s own core CPI stands at +0.4% yoy. At its latest meeting, the BoJ announced some minor policy tweaks, including more flexibility in bond operations, but overall, policy was kept ultra-loose. With inflation at such low levels, we stick to our guns that it could be very hard for policymakers to proceed with a meaningful step towards normalization any time soon.

During the European day, we get Germany’s final GDP for Q2. As usual, the forecast is for the final print to confirm the preliminary estimate and show that Eurozone’s growth engine accelerated to +0.5% qoq from an upwardly revised +0.4% in Q1.

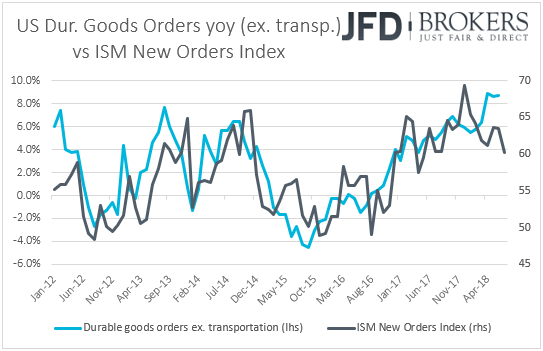

From the US, we get durable goods orders for July. Expectations are for headline orders to have risen by 0.8% mom, the same pace as in June, something that could push the yoy rate up. As for core orders, they are anticipated to accelerate on a monthly basis, to +0.3% mom from +0.2%, but this is likely to drag the yoy rate down. The case for a decline in the yearly core rate is supported by the New orders sub-index of the ISM manufacturing PMI for the month, which declined to 60.2 from 63.5 in June.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.