Following the FOMC and RBNZ meetings last week, it is the turn of the RBA to decide on monetary policy, but once again, we don’t expect any fireworks. On Friday, the US and Canadian employment reports will be in the spotlight, while on the political front, the annual conference of the UK Conservative Party, which started yesterday and will continue until Wednesday, will be closely watched.

Monday is a PMI day. During the European morning, we get the final manufacturing prints for September from several European nations and the Eurozone as a whole. As it is usually the case, the final numbers are expected to confirm their preliminary estimates.

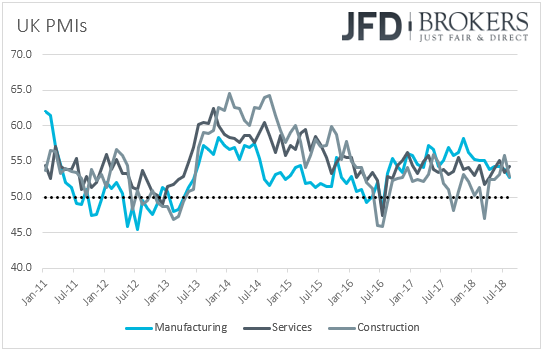

The UK manufacturing PMI for September is also coming out. In August, the PMI declined to a 2-year low of 52.8, with the IHS Markit Director Rob Dobson noting that the report is broadly consistent with zero growth in manufacturing production. Now the index is expected to have declined further, to 52.5 from 52.8, which could raise some concerns over the sector’s support to the economy in Q3. That said, as we have noted several times in the past, investors are likely to focus more on the services PMI, due out on Wednesday, in order to get a clearer picture on how the economy may have performed during the last month of the quarter, as the service sector accounts for around 80% of the UK GDP.

We get September manufacturing PMIs from the US as well. The final Markit index is expected to confirm its first estimate of 55.6, while the more-closely-watch ISM index is forecast to have declined to 60.1 from 61.3.

In Asia, Chinese markets will be closed for the whole week in celebration of the National Day holiday.

On the political front, the UK Conservative Party has begun its annual conference yesterday, which will continue until Wednesday. Following the Salzburg summit, where no progress was made on the Brexit front, with EU officials rejecting PM Theresa May’s plan, it will be interesting to see how much of opposition will the plan face within her own party. The Prime Minister will address the conference on Wednesday.

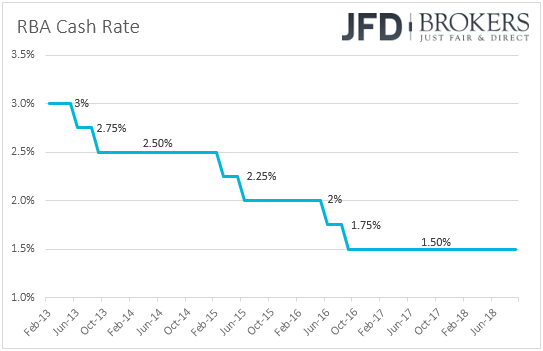

On Tuesday, during the Asian morning, the RBA decides on monetary policy, but once again, we don’t expect any fireworks. The Bank has been stubbornly keeping interest rates at +1.50% since August 2016, and according to its latest Statement on Monetary Policy, the cash rate is expected to increase around the end of next year. At its latest meeting, the Bank proceeded with some upbeat tweaks in its statement, noting that in the first half of 2018, the economy is expected to have grown at an above-trend rate, and that wage growth has picked up a little recently. That said, the statement was far from suggesting a change in the RBA’s future plans.

After that meeting, GDP data showed that the Australian economy slowed to +0.9% qoq in Q2 from an upwardly revised +1.1% qoq in Q1, but this pushed the yoy rate up to +3.4% from 3.1%. The unemployment rate remained unchanged at 5.3%, while the net change in employment showed that the economy gained more jobs than expected. The NAB business survey showed that labor costs accelerated to +1.3% in the three months to August from +0.9% in the three months to July. All these numbers suggest that the Bank is likely to maintain the upbeat tweaks it made in its latest statement, but they do not suggest that we will get anything more.

As for Tuesday’s economic data, the only release worth mentioning is the UK construction PMI for September, which is expected to have declined to 52.5 from 52.9. However, as we already noted, we believe that most of the attention will fall on the services index on Wednesday.

On Wednesday, during the European morning, we get the final services and composite PMIs from the European nations of which we get the manufacturing data on Monday. Once again, the final prints are anticipated to confirm the preliminary estimates. Eurozone’s retail sales for August are coming out as well and expectations are for a 0.2% mom rebound after a 0.2% slide in July. This would drive the yoy rate up to +1.6% from 1.1% previously.

In the UK, the services PMI is expected to have slid to 54.0 in September from 54.3. In August, the index rose to 54.3 from 53.9, with Markit’s Chief Economist Chris Williamson saying that the data suggests that the economy is on course to expand by 0.4% in Q3. Nevertheless, even a small decline in the services print, if accompanied with further softness in the manufacturing and construction indices, could raise some concerns over the performance of the UK economy during the quarter.

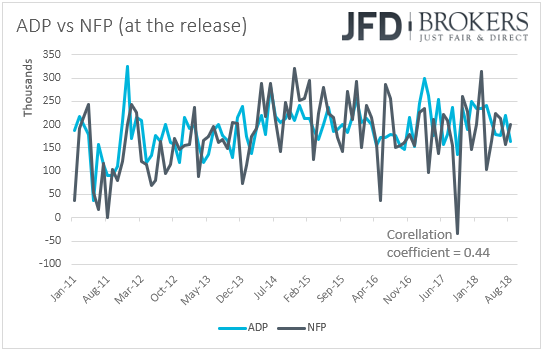

In the US, we get the ADP employment report for September. Expectations are for the private sector to have gained 185k jobs, more than the 163k in August. This could increase bets that the NFP print, due to be released on Friday, may come close to its forecast, which is also 185k. That said, we must repeat that even though the ADP is the only major gauge we have for the non-farm payrolls, the correlation between the two time-series at the time of the release (no revisions are taken into account) has been very low in recent years. Taking into account data from January 2011, the correlation stands at around 0.44. The final Markit services and composite PMIs, as well as the ISM non-manufacturing index, all for September, are also due out. The Markit prints are forecast to confirm their first estimates, while the ISM index is expected to have declined to 60.0 from 60.7.

Thursday appears to be a relative light day in terms of economic releases. During the Asian morning, we get Australia’s trade balance for August, while later in the day, the US factory orders for the same month and Canada’s Ivey PMI for September are coming out.

Finally, on Friday, the spotlight is likely to fall on the US employment report for September. Expectations are for non-farm payrolls to have increased 185k after rising 201k in August. The unemployment rate is expected to have ticked back down to its 18-year low of 3.8%, while average hourly earnings are anticipated to have slowed somewhat on a monthly basis, to +0.3% mom from +0.4%. Barring any revisions to the prior monthly prints, this could drive the yoy rate down to +2.8% from +2.9%, as the September 2017 monthly rate that will drop out of the yearly calculation was +0.5%.

Overall, the forecasts suggest that we are likely to get another report consistent with further tightening in the labor market, something that could strengthen the case for a December rate hike by the Fed. The key takeaway we got from last week’s meeting is that Fed officials remain willing to continue raising rates until the data suggests otherwise, despite removing from the statement the part describing monetary policy as accommodative.

Even if wages slow somewhat, we doubt that this would prove enough to alter market expectations with regards to the Fed’s future plans. According to the Fed funds futures, the market assigns a near 80% chance for a hike in December, while it sees another 2 for 2019 at a time when the Fed’s 2019 median dot points to 3. We believe that a more severe slowdown in earnings is needed for the market to scale back its expectations. On the other hand, an upside surprise could raise bets of accelerating inflation in the near future and thereby, prompt market participants to bring their expectations closer to the Fed’s projections.

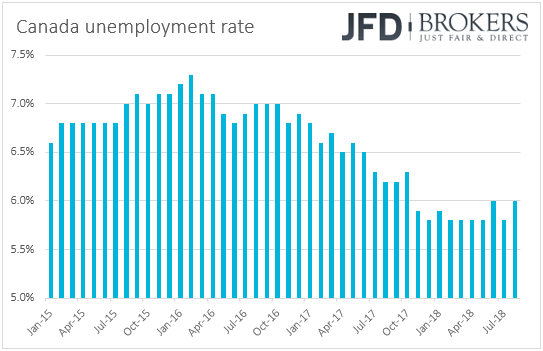

We get employment data for September from Canada as well. The forecasts suggest that the unemployment rate remained unchanged at 6.0%, while the net change in employment is anticipated to show that the economy gained 24.7k jobs after losing 51.6k the previous month.

Recent data out from Canada showed that the headline CPI rate declined to +2.8% yoy from 3.0%, but the core rate ticked up to +1.7% yoy from +1.6%. Headline retail sales rebounded less than anticipated, but core sales accelerated by more than the forecast suggested. What’s more, last Friday, monthly GDP data showed that the economy grew 0.2% mom in July after stagnating in June. All these keep the door wide open for a rate increase at the BoC’s upcoming gathering, scheduled for the 24th of October, and a decent employment report could further increase that likelihood.

As for the rest of Friday’s releases, during the Asian morning, Australia’s retail sales for August are expected to have risen 0.2% mom, after stagnating in July, while later in Europe, we get Germany’s factory orders for August and Switzerland’s CPIs for September. Germany’s factory orders are expected to have increased 0.3% mom after declining 0.9% in July, while Switzerland’s CPI rate is anticipated to have ticked down to +1.1% yoy from +1.2%.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.