This week, we have three central banks deciding on monetary policy: The RBA, the BoC and the ECB. It will be interesting to see whether the RBA will introduce the rate-cut chance within the statement, and whether the BoC will maintain its plan for more hikes over time. With regards to the ECB, investors may be eager to see whether the Bank will alter its interest-rate guidance and whether there will be any announcement on new TLTROs. The US and Canadian employment data for February will also be in focus.

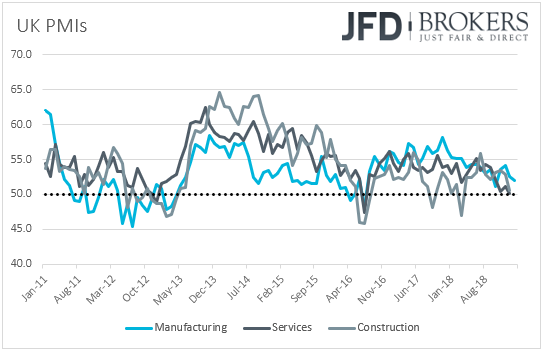

Monday appears to be a relatively light day in terms of economic releases, with the only worth mentioning being the UK construction PMI for February. Expectations are for the index to have ticked down to 50.5 from 50.6 in January. The case for a lower print is supported by the manufacturing index, released on Friday, which slid to 52.0 from 52.6. That said, we repeat for the umpteenth time that usually investors tend to focus more on the services PMI, which is released on Tuesday, as the service sector accounts for around 80% of the UK economy.

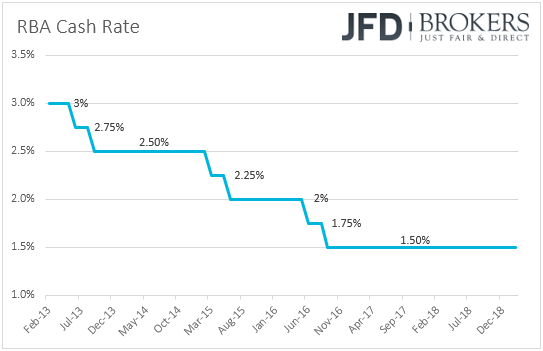

On Tuesday, during the Asian morning, the RBA decides on monetary policy. At the preivous meeting, the Bank kept interest rates unchanged, and while the statement had a somewhat dovish flavor compared to the previous one, it included no hints with regards to a potential rate cut in the months to come. That said, just the following day, Governor Lowe put that prospect well on the table, noting that interest rates could move in either direction, with the probabilities of an up and a down move evenly balanced, something that was mentioned in the meeting minutes as well. What’s more, in its quarterly Statement on Monetary Policy, the Bank slashed its GDP and inflation forecasts, also noting that financial market prices suggest that interest rates are likely to stay unchanged over the months ahead, with some expectation of a decrease by the end of this year.

Since then, then only top-tier data we got related to the labor market. The wage price index for Q4 rose +2.3% yoy, the same pace as in Q3, while the employment report for January showed that the unemployment rate held steady at 5.0% and that the economy gained more jobs than in December. Bearing in mind that the Bank has put the prospect of a rate cut on the table, already acknowledging the strength of the labor market, we don’t expect the statement to paint a much different picture than the previous one. Having said that though, it will be interesting to see whether the cut-case will be included in the statement this time, and not just in the meeting minutes.

As for Tuesday’s economic data, during the Asian day, Australia’s current account balance for Q4 and China’s Caixin services PMI for February are due to be released. Australia’s current account deficit is expected to have narrowed somewhat, while China’s Caixin index is forecast to have ticked down to 53.5 from 53.6 in January.

During the European morning, we get Switzerland’s CPI for February, which is expected to have slowed for the 4th consecutive month, to +0.5% yoy from +0.6%, which is well below the SNB’s target of 2%. With the Bank itself not seeing that target being hit even in Q3 2021, we believe that policymakers are unlikely to be tempted to alter their loose policy with such a low inflation rate. The SNB is scheduled to hold its first monetary policy meeting for 2019 on March 21st, when we expect officials to keep interest rates unchanged, reiterating that they will stay active in the foreign exchange market as necessary and that the franc remains highly valued.

From the Eurozone, we have retail sales for January and expectations are for a +1.3% mom rebound after a 1.6% slide in December. This may drive the yoy rate up to +2.0% from +0.8%. We also get the final services and composite PMIs for February from several European nations and the bloc as a whole, but as it is usually the case, the final prints are expected to confirm their preliminary estimates.

The UK services PMI for February is coming out as well. The forecast suggests that the index slipped into contractionary territory. Specifically, it is expected to have declined to 49.9 from 50.1, something that may amplify concerns on how Brexit uncertainty is weighing on the UK economy. Nevertheless, with a disorderly exit most likely to be averted, at least on March 29th, we don’t expect the PMIs to prove game changers with regards to the pound's forthcoming direction. Remember that the pound fell when the January services print disappointed but surged in the second half of February on hopes that a no-deal exit can be eventually avoided.

Therefore, we expect GBP-traders to keep their focus locked on developments surrounding the UK political landscape and the vote-series PM Theresa May promised to Parliament. Remember that last week, PM May told lawmakers that they will have a new deal on the table by March 12th, and if it is not approved, another vote will take place the on March 13th. The second vote will be on whether Britain should leave the EU with or without a deal. If Parliament rejects the option of a disorderly withdrawal, a third vote over extending the process will be held the following day.

In the US, we get the final Markit services and composite PMIs for February, as well as the ISM non-manufacturing index for the month. As it is the case most of the times, the final Markit prints are expected to confirm their preliminary numbers, while the ISM index is anticipated to have risen to 57.4 from 56.7. New Home sales for December are due out as well and the forecast suggests a slowdown to +2.9% mom from +16.9%.

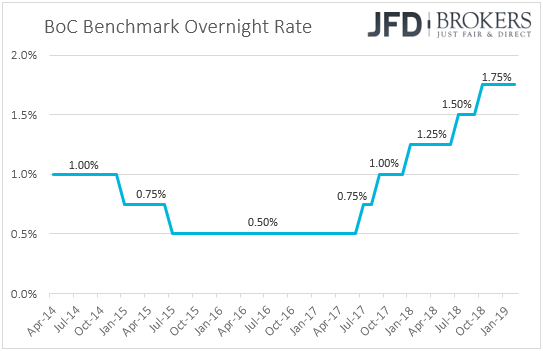

On Wednesday, the central bank torch will be passed to the Bank of Canada. When they last met, BoC policymakers left interest rates unchanged and kept the door open for further rate increases. Latest CPI data showed that inflation slowed in both headline and core terms, while economic activity contracted in both November and December, with the qoq annualized rate for the final quarter of 2018 tumbling to +0.4% from +2.0%.

Seen in isolation, these releases raise concerns over the BoC’s ability to raise borrowing costs further. However, bearing in mind that, in a recent speech, Governor Poloz noted that the Bank’s plan remains for higher rates over time, we believe that officials could keep their forward guidance unchanged at this meeting. They may prefer to wait and see whether the softness continues before they go ahead with such a move. That said, we don’t expect an upbeat narrative either. In the same speech, the Governor said that the timing of future rate increases is “highly uncertain”, which combined with the aforementioned data may prompt policymakers to strike a more cautious stance compared to the previous time, even if they stick to their guns that further rate increases are needed in the foreseeable future.

As for the rest of Wednesday’s data, Australia’s GDP for Q4 is due to be released and the forecast suggests an uptick to +0.4% qoq, after tumbling to +0.3% in Q3 from +0.9%. That said, this would still drive the yoy rate lower, to +2.6% from +2.8%, which is slightly below the RBA’s projection of 2.75% and, conditional upon a dovish meeting statement on Tuesday, may increase speculation with regards to a rate cut by year end.

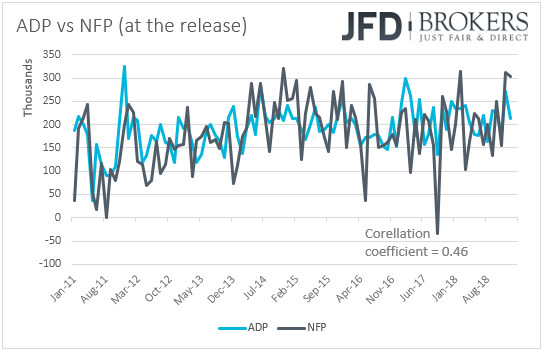

Later in the day, in the US, the ADP employment report for February is due to be released. Expectations are for the private sector to have gained 190k jobs, less than January’s 213k. This could raise bets that the NFP number, due out on Friday, may also come in below its prior stellar print of 304k. At the time of writing, the forecast for non-farm payrolls is at 185k. That said, we repeat once again that, even though the ADP is the only major gauge we have for the non-farm payrolls, the correlation between the two time-series at the time of the release (no revisions are taken into account) has been low in recent years. Taking into account data form January 2011, this correlation stands at 0.46. The US trade balance for December is also due to be released and expectations are for the nation’s trade deficit to have widened to USD 57.8bn from 49.3bn.

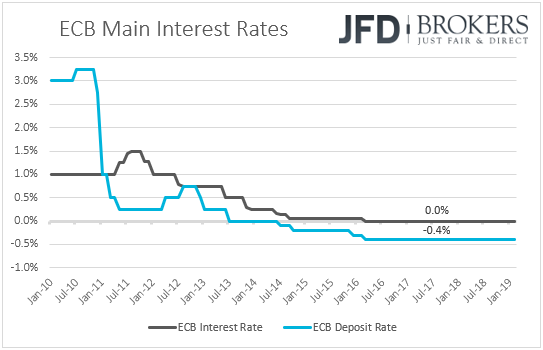

On Thursday, it’s the turn of the ECB to decide on monetary policy. At the January meeting, the Bank made no changes to interest rates and the accompanying statement, but at the press conference following the decision, ECB President Mario Draghi noted that the risks surrounding the bloc’s economic outlook have “moved to the downside”. He also said that the fact that the market places the first hike in 2020 shows that investors understood the Bank’s reaction function, something that was mentioned in the minutes as well. With regards to whether they have started looking into a new round of TLTROs (Targeted Long-Term Refinancing Operations), which are cheap loans to banks, Draghi said that several policymakers raised the issue, but no decision was taken.

Since then, economic data continued to suggest a weak economic outlook. Headline inflation ticked up to +1.5% yoy in February, but the core CPI rate slid back to +1.0% yoy from +1.1%, which is well below the Bank’s objective of “below, but close to 2%”. According to preliminary data, the composite PMI rose to 51.4 in February from 51.0 in January, but this is the first rise after six consecutive slides, and in our view, it is far from suggesting a decent rebound in Eurozone’s economic activity.

Having all that in mind, investors may will be looking to see whether the Bank will push back its interest-rate forward guidance and whether it will introduce a new round of TLTROs. Although given the market consensus for a hike in 2020, officials could alter their forward guidance at this meeting, we believe that they may prefer to wait for a while more before they do that. After all the “at least through summer of 2019” notion is an open ended one, which, in our view, means that interest rates could start rising in September the earliest, but also well thereafter. With regards to the TLTROs, bearing in mind that the latest minutes suggested that decisions in this respect shouldn’t be taken “too hastily”, we believe that officials could also wait a bit longer before taking such a step. However, we may get some hints on whether they consider acting in the upcoming months. The meeting will be also accompanied with new staff macroeconomic projections, where we expect downward revisions in both GDP and inflation forecasts.

As for Thursday’s economic indicators, during the Asian morning, we have Australia’s trade balance and retail sales, both for January. The nation’s trade surplus is expected to have decreased, but retail sales are anticipated to have rebounded 0.3% mom after sliding 0.4% in December. Later in the day, we have Eurozone’s final GDP for Q4, which is expected to confirm the second estimate, and the US Labor Costs Index for the quarter, which is anticipated to have accelerated to +1.6% qoq from +1.2%.

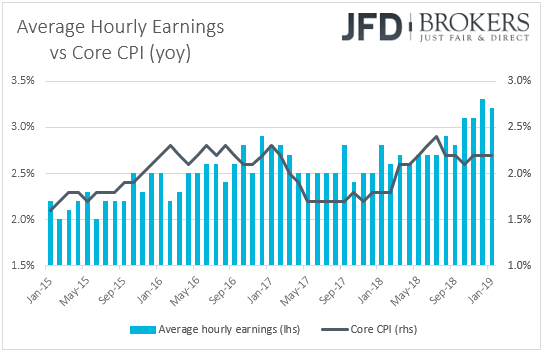

On Friday, investors are likely to lock their gaze on the US employment report for February. Expectations are for nonfarm payrolls to have risen 185k, less than January’s 304k, but still a healthy number. The unemployment rate is forecast to have declined to 3.9% from 4.0%, while average hourly earnings are anticipated to have accelerated to +0.3% mom from +0.1%. Barring any revisions to the prior monthly prints, this is likely to drive the yoy rate up to +3.3% yoy from +3.2%, as the monthly print of February 2018 that will drop out of the yearly calculation is +0.1%.

Overall, the numbers point to a strong report, consistent with further tightening in the labor market. Although Fed Vice Chair Richard Clarida noted last week that wage gains are no putting upward pressure on inflation, further acceleration in earnings may eventually lead to somewhat higher consumer prices. Following last week’s GDP data, which eased concerns of a severe slowdown, a robust employment report could cause the likelihood for a Fed rate cut in 2019 to vanish and may even push slightly up the hike percentage. According to the Fed funds futures, the market is nearly 92% confident that the Committee will refrain from pushing the hiking button this year, while there is a 7% chance for an increase. The chance for a cut has now dropped to 1%.

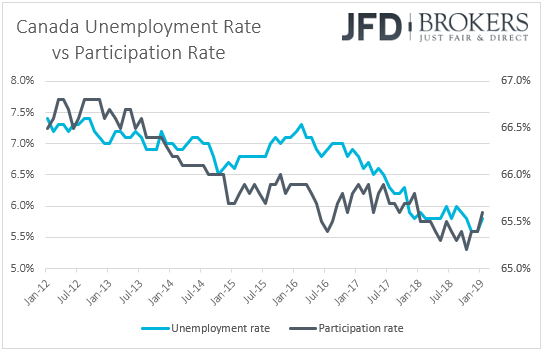

We get employment data for February from Canada as well. The unemployment rate is expected to have ticked down to 5.7% from 5.8%, but the net change in employment is expected to show a decline of 5k jobs after a 66.8k gain in January. Given that the participation rate is expected to have declined as well, we believe that the potential slide in the unemployment rate may be owed to unemployed people stop looking actively for a job, instead of more people being employed.

With regards to the rest of the data, we get Japan’s final GDP for Q4, and China’s trade balance for February. China’s CPI and PPI numbers for the month are also coming out, but during the Asian morning Saturday.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Group, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Group analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD Group prohibits the duplication or publication without explicit approval.

76% of the retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.

Copyright 2019 JFD Group Ltd.