This week, the central bank torch will be passed to the RBA and the RBNZ, with both Banks widely anticipated to keep interest rates unchanged. As for the economic indicators, we get the first estimate of the UK GDP for Q2, the US CPIs for July, as well as Canada’s employment report for the same month.

Monday is a relatively quiet day with no major events or indicators scheduled on the agenda.

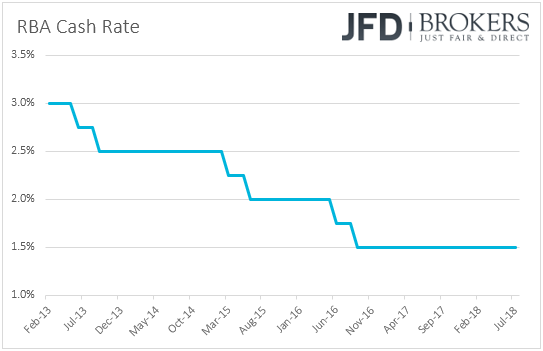

On Tuesday, during the Asian morning, the RBA concludes its policy meeting. Expectations are for the Bank to keep interest rates untouched once again. Lately, the RBA meetings have proven to be non-events and we believe that this one will not be an exemption.

Since the latest meeting, the only noteworthy data we got were the inflation prints for Q2. The headline CPI rate rose to +2.1% yoy from +1.9% in Q1, entering the RBA’s 2-3% target band, and exceeding by a tick the Bank’s own projection of 2%. That said, the trimmed mean rate remained unchanged at +1.9% yoy, below the Bank’s latest forecast for underlying inflation, which was also 2%. In our view, these figures are far from suggesting a change in RBA’s thinking around policy.

As for Tuesday’s economic indicators, US JOLTs Job Openings for June are coming out and expectations are for a slight increase to 6.74mn from 6.64mn the previous month. Canada’s Ivey PMI for July is also coming out.

On Wednesday, the calendar appears to be relatively light as well. During the Asian morning, Australia’s home loans are expected to have slowed to +0.1% mom in June from +1.1% in May. China’s trade surplus is forecast to have decreased somewhat in July, to 39.3bn from 41.5bn in June. Imports are expected to have accelerated to +16.2% yoy from +14.1%, while exports are anticipated to have slowed to +10.0% yoy from +11.3%.

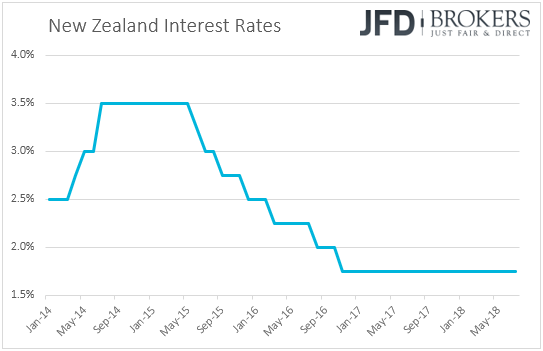

On Thursday, the RBNZ takes its turn in deciding on monetary policy, but no change in policy is expected from this Bank either. At its previous meeting, the Bank kept interest rates unchanged at +1.75%, while the accompanying statement was slightly more dovish than the previous one. Governor Adrian Orr reiterated that interest rates could move in either direction, keeping the prospect of a rate cut on the table, while he appeared more concerned with regards to the global and domestic economic outlooks.

Since then, data showed that New Zealand’s inflation accelerated to 1.5% yoy in Q2 from 1.1%, which is in line with the Banks projections in its latest quarterly Monetary Policy Statement. The unemployment rate ticked up to 4.5% from 4.4%, its lowest since Q3 2009, while the net change in employment accelerated somewhat during the quarter.

So, having all these in mind, we don’t expect any major changes in the Bank’s view around monetary policy. According to its latest quarterly Monetary Policy Report, the Bank expects interest rates to start rising in September 2019. Alongside the policy decision, we will get the new quarterly Monetary Policy Statement, which includes the Bank’s updated economic projections, as well as a press conference by Governor Adrian Orr.

As for Thursday’s economic data, during the Asian morning, we get China’s CPI and PPI, both for July. The CPI rate is expected to have remained unchanged at +1.9% yoy, while the PPI is anticipated to have slowed to 4.6% yoy from 4.7%.

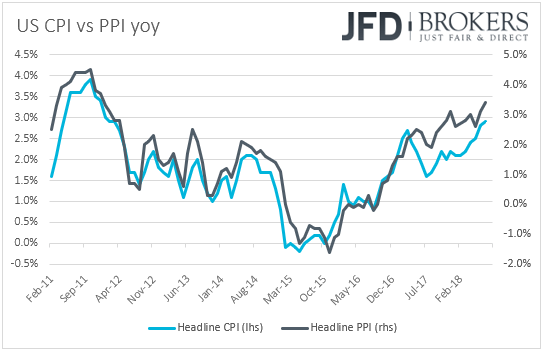

Later in the day, we get the US PPIs for July. Expectations are for both the headline and core PPI rates to have declined to +3.2% yoy and +2.6% yoy, from +3.4% and 2.8% respectively. Slowing producer prices could result slowing consumer prices and thus, these prints could raise some speculation that the CPIs, due out on Friday, may follow suit.

Finally, on Friday, during the Asian morning, we get Japan’s preliminary GDP for Q2. Expectations are for a rebound to +0.3% qoq after a 0.2% slide in Q1. This is likely to drive the yoy rate up to +1.4% from -0.6%.

During the European morning, we get inflation data for July from Norway and Sweden. Kicking off with the Norwegian figures, the headline CPI rate is anticipated to have declined to +2.4% yoy from +2.6%, but to stay slightly above the Norges Bank estimate for the month of 2.3%. The core rate expected to have remained unchanged at +1.1% yoy, just a tick below the Bank’s core projection of +1.2%. At its latest meeting, the Norges Bank decided to keep interest rates unchanged and noted that “the key policy rate will most likely be raised in September 2018”. Thus, with July inflation expected to stand near its own projections, we don’t expect the Bank to change its guidance when it meets next, on the 16th of August. We think that a notable downside surprise is needed for market participants to start worrying that the Bank may not proceed with hiking rates in September.

Passing the ball to Sweden, the CPI rate is expected to have remained unchanged at +2.1% yoy, while the CPIF rate is anticipated to have risen at 2.3% yoy. At its latest meeting, the Riksbank kept interest rates untouched and maintained the view that slow repo rate rises will be initiated towards the end of the year. However, apart from the usual dissenter, Deputy Governor Ohlsson, who supported raising the repo rate to -0.25%, we had another member with reservations. Deputy Governor Martin Floden advocated for a repo rate path with an initial increase of interest rates by 25bps in September or October. That said though, the June inflation data showed that the excluding energy CPIF decelerated. Thus, even if the headline CPIF rate rises somewhat in July, a decent acceleration in core CPIF is needed before SEK traders start raising bets that the Bank may act sooner than previously thought.

From the UK, we get the first estimate of GDP for Q2, as well as industrial and manufacturing production data for June. The first GDP estimate is expected to show that the economy expanded +0.4% in Q2 from +0.2% in Q1, in line with the BoE’s view, as well as the NIESR GDP Estimate model. Industrial production is anticipated to have rebounded to +0.4% mom in June after falling 0.4 in May. However, this is likely to drive the yoy rate a tick lower, to +0.7% from +0.8%. Manufacturing production is expected to have slowed somewhat, to +0.3% mom from +0.4%, pushing the yoy rate down to +1.0% from 1.1%. The key message we got from last week’s BoE policy meeting, when the Bank raised rates to +0.75%, is that officials are probably done hiking for this year. Thus, if the forecasts are met, we doubt that this data set will alter investors’ opinion around the BoE’s future plans. The UK trade balance for June is also coming out.

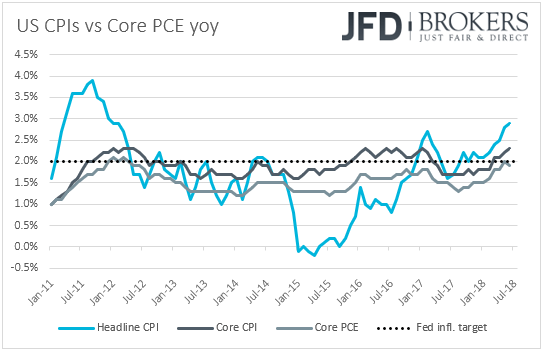

Later in the day, from the US, we get CPI data for July. Expectations are for headline inflation to have accelerated to +3.0% yoy from +2.9%, while the core rate is expected to have remained unchanged at +2.3% yoy. That said, both the US PPIs for the month, due out on Thursday, are expected to have slowed somewhat and thus we view the risks surrounding the CPIs as tilted somewhat to the downside.

However, even if the CPIs slow somewhat, as long as they remain above the Fed’s 2% objective, we don’t expect something like that to change market expectations much with regards to the Fed’s future plans. At last week’s gathering, the FOMC kept interest rates unchanged but kept the door open for two more rate hikes by the end of the year. According to the Fed funds futures, there is a 94% probability for the next rate increase to occur in September, while there is a 67% chance for another one to come in December.

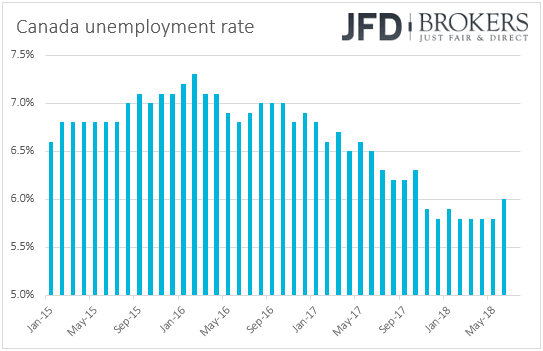

From Canada, we get the employment report for July. Expectations are for the unemployment rate to have declined to 5.9% from 6.0% in June, while the net change in employment is forecast to have declined to 17.5k from 31.8k. Following the acceleration in May’s GDP and the rise in the headline inflation rate for June, a decent employment report may increase further market participants’ confidence over the prospect of another BoC rate hike by year end.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.