Risk appetite got a strong boost at the opening of this week after US President Donald Trump and his Chinese counterpart Xi Jinping agreed over the weekend to put tariffs on hold and try to solve their differences within 90 days. Market participants are likely to stay on the edge of their seats in anticipation to fresh headlines with regards to the matter but also keep an eye on Brexit and Italy. However, this week appears busy in terms of economic developments as well. The RBA and the BoC hold their last policy meetings for the year, while the US jobs report is likely to attract extra attention, especially after Powell’s speech and the release of the Fed minutes last week. As for the energy market, all lights will fall to the OPEC+ gathering in Vienna.

Monday is a PMI day. During the European morning, we get the final manufacturing PMIs for November from several European nations and the Eurozone as a whole. As usual, the final prints are anticipated to confirm the preliminary estimates.

In the UK, the manufacturing PMI is forecast to have risen to 51.6 from 51.1. Under normal circumstances, the market tends to pay more attention to the services index, which is scheduled to be released on Wednesday, but given that the political scene has overshadowed economic developments in the UK, we don’t expect this set of PMIs to prove critical with regards to the pound’s forthcoming direction. The British currency is likely to stay anchored to headlines surrounding the Brexit landscape.

We get November manufacturing PMIs from the US as well. The final Markit print is forecast to match the preliminary figure, while the but the ISM index is anticipated to have declined slightly, to 57.5 from 57.7.

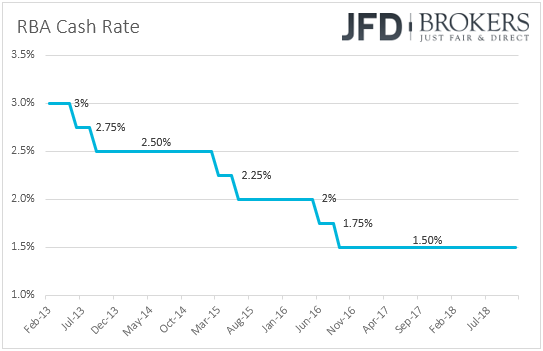

On Tuesday, during the Asian morning, the Reserve Bank of Australia decides on monetary policy, but once again, we don’t expect any fireworks. The Bank has been stubbornly keeping its benchmark cash rate unchanged at +1.50% since August 2016, and it is widely anticipated to keep it there at this meeting as well.

When they last met, Australian policymakers proceeded with some positive changes in the accompanying statement, but the Aussie strengthened only 10 pips at the time of the release, a move suggesting that the changes were not significant enough for market participants to bring forth their expectations with regards to when interest rates may start rising. Indeed, according to the Bank’s quarterly Statement on Monetary policy, released a few days after the meeting, financial market prices imply that the cash rate is expected to increase in 2020.

Since that gathering, the only top-tier releases we got related to the labor market. The unemployment rate remained unchanged at 5.0% in October, while the net change in employment showed that the economy gained much more jobs than it did in September. What’s more, the wage price index accelerated to +2.3% yoy in Q3 from +2.1% in Q2. These releases suggest that the Bank is likely to keep the latest positive tweaks in its statement, but we don’t expect any major surprises beyond that.

As for the rest of the day, during the European day, Switzerland’s CPI for November is due to be released and is expected to have slowed to +1.0% yoy from +1.1%. At its latest meeting, the Swiss National Bank kept its benchmark rate unchanged at -0.75%, reiterating that it will remain active in the FX market as necessary and repeating that the Swiss franc is highly valued. It also revised down its inflation forecasts, suggesting that the CPI rate is likely to hit the Bank’s 2% target in Q2 2021. The decision was taken at a time when the rate was at +1.2% yoy and this was conditional upon interest rates staying at current levels for the whole forecast horizon. Therefore, even if the CPI rate does not tick down as the forecast suggests and stays unchanged, or even rise somewhat, we see it unlikely for SNB policymakers to be tempted to alter their policy stance.

The UK construction PMI for November is also coming out and expectations are for a decline to 52.7 from 53.2 in October.

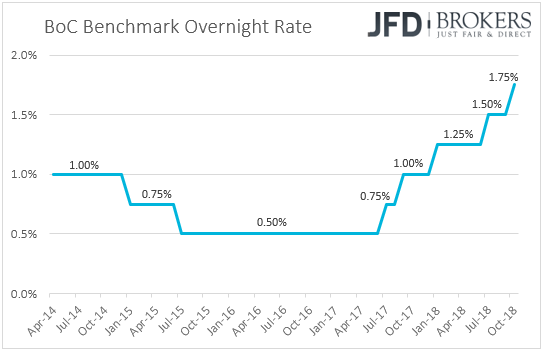

On Wednesday, the central bank torch will be passed to the Bank of Canada, which is also expected to keep interest rates untouched after raising them to +1.75% at its latest meeting. If so, given that this will be one of the “smaller” meetings that are not accompanied by updated economic projections neither a press conference, all the attention is likely to fall to the meeting statement.

At the previous gathering, apart from raising rates, officials removed from the accompanying statement the part saying that they will “take a gradual approach” with regards to future rate increases. In our view, this means that if data suggest so, interest rates can rise faster than previously anticipated.

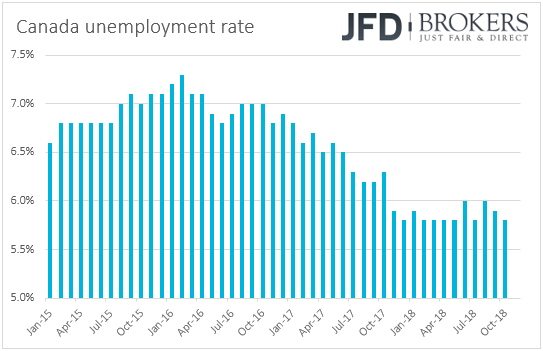

Latest data showed that the unemployment rate declined to 5.8% in October from 5.9% in September, while inflation accelerated in both headline and core terms. However, Friday’s GDP data showed that the economy shrank 0.1% in September, which may have prompted market participants to take a few January-hike bets off the table. Thus, it would be interesting to see how upbeat (or not) the statement will be, and how this will shape expectations around the Bank’s next move.

As for Wednesday’s economic indicators, during the Asian morning, Australia’s GDP for Q3 is due to be released. Expectations are for a slowdown to +0.6% qoq from +0.9% in Q2, something that could drive the yoy rate down to +3.3% from +3.4%. China’s Caixin services PMI for November is coming out as well. The forecast suggests that the index remained unchanged at 50.8 but bearing in mind that the official non-manufacturing index for the month declined to 53.4 from 53.9, we view the risks surrounding the Caixin forecast as tilted to the downside.

During the European day, we get the final service-sector and composite PMIs for November from the European nations of which we get the manufacturing prints on Monday, as well as for the Eurozone as a whole. As usual, expectations are for a confirmation of the preliminary numbers. Eurozone’s retail sales for October are also coming out and are expected to have risen +0.2% mom after stagnating in September.

We get the November services PMI from the UK as well, which is expected to have risen to 52.5 from 52.2. This is the most important among the three UK PMIs, as the services sector accounts for near 80% of the nation’s total GDP. However, as we already noted, UK’s economic data appear to have been overshadowed by developments surrounding the Brexit landscape and thus, we expect the index to attract less attention than usual.

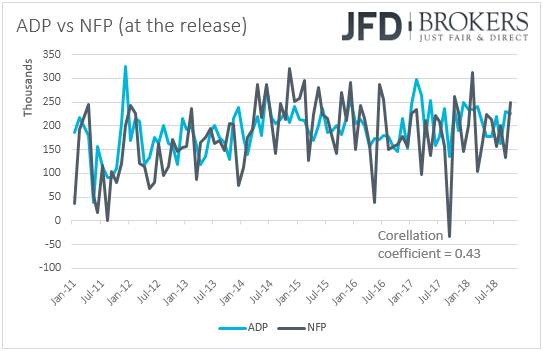

From the US, we get the ADP employment report for November. Expectations are for the private sector to have gained 196k jobs, less than the 227k in October. This could raise speculation that the NFP number, due out on Friday may also come below October’s print of 250k. Indeed, currently the NFP forecast is at 200k. However, we repeat to the umpteenth time that, even though the ADP is the only major gauge we have for the non-farm payrolls, the correlation between the two time-series at the time of the release (no revisions are taken into account) has been very low in recent years. Taking into account data from January 2011, this correlation stands at 0.43. The final Markit services and composite PMIs for November, as well as the ISM non-manufacturing index for the month are also due to be released.

On Thursday, the spotlight is likely to turn to the energy market, as major OPEC and non-OPEC oil producers – known as the OPEC+ group – gather in Vienna to discuss output policy in a two-day meeting. Back in June, members have decided to return back to market 1.0mn bpd in order to deal with supply shortfalls from Venezuela as well as the effects of the US sanctions imposed to Iran. That said, since the beginning of October, oil prices have been in a falling mode due to a blend of surging US production, a risk-off environment, as well as demand concerns due to slowing global growth. The fact that the US granted waivers to eight countries, letting them to continue importing Iranian oil even after it sanctioned the nation, did not help oil prices either.

A couple of weeks ago, producers signaled their willingness to reduce production in 2019, with their analysis suggesting the need for a 1mn bpd supply reduction from October levels. A couple of days later, a report citing sources familiar with the matter noted that producers were discussing the case for a 1.4mn bpd cut.

As for our view, OPEC and its allies are more likely (than not) to proceed with cutting production, despite US President Trump’s warnings not to do so. However, the market’s reaction is likely to depend on the amount of the expected cut. Currently, the information investors have in hand is for 1-1.4mn bpd. Therefore, a deeper cut could encourage oil-bulls to jump back into the action and lift prices up, while a lower number could disappoint investors and the “black gold” may slide further. Anything within the 1-1.4mn range could just stabilize prices somewhat. The surprise would be no cuts at all. This is where oil prices could tumble, accelerating the latest downtrend.

Besides the OPEC meeting, in terms of economic indicators, we get Australia’s trade balance and retail sales, both for October. The trade balance print is expected to show that the nation’s trade surplus has increased somewhat, while retail sales are expected to have slightly accelerated, to +0.3% mom from +0.2% in September. We get October trade data from US and Canada as well. Both trade deficits are forecast to have widened slightly. US factory orders and Canada’s Ivey PMI for October are also scheduled to be released.

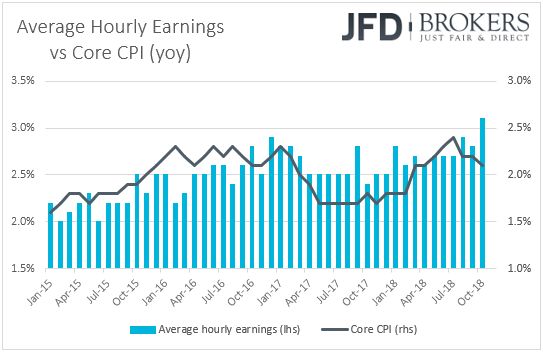

On Friday, all eyes are likely to be on the US employment report for November. Expectations are for NFPs to have risen 200k, which is less than October’s 250k, but still a decent number consistent with further tightening of the labor market. The unemployment is expected to stay at 3.7%, its lowest since 1969, while average hourly earnings are anticipated to have accelerated somewhat on a monthly basis, to +0.3% mom from +0.2%. Barring any revisions to the prior prints, this is likely to keep the yoy rate unchanged at +3.1%.

Overall, the forecasts point to a strong report, with wage growth suggesting that inflation is possible to accelerate in the months to come. Last week, Fed chair Powell’s dovish remarks prompted market participants to price out their expectations with regards to the number of interest rate hikes the Fed may deliver next year, despite staying overly optimistic that a December move remains firmly on the cards. According to the Fed fund futures, the market assigns an 85 chance for a December hike, but sees only 1.4 hikes throughout 2019. A few weeks ago, that number was around 2. The minutes of the latest FOMC meeting confirmed investors’ choice, with a few participants expressing uncertainty about the timing of future rate increases, and many arguing for placing more emphasis on the evaluation of incoming data. So, having in mind that the Fed wants to focus more on economic data, such an employment report may encourage the market to drive the number of hikes expected in 2019 slightly higher.

We get employment data for November from Canada as well. Expectations are for the unemployment rate to have held steady at 5.8%, while the net change in employment is anticipated to show that the economy has gained slightly more jobs than in October (15.0k vs 11.2k). Conditional upon a hawkish BoC on Wednesday, a decent employment report may help to revive hopes with regards to a January hike.

As for other data, we have Eurozone’s wage growth and employment change data for Q3, as well as the final GDP print for the same quarter. The preliminary UoM consumer sentiment index for December is also coming out and is expected to decline to 97.1 from 97.5.

Finally, on Saturday, China’s trade balance for November is released. The forecasts suggest that the nation’s trade surplus increased to USD 36.2bn from 34.0bn, but both exports and imports are anticipated to have slowed on a yoy basis.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

68% of the retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.