The dollar strengthened yesterday after Fed Vice Chair Clarida appeared more upbeat with regards to future rate increases than he did around 10 days ago, while remarks by White House Economic Advisor Larry Kudlow boosted the broader market sentiment. Today, focus is likely to turn to Fed Chair Powell’s speech.

Clarida’s Remarks Boost USD, Focus Turns to Powell’s Speech

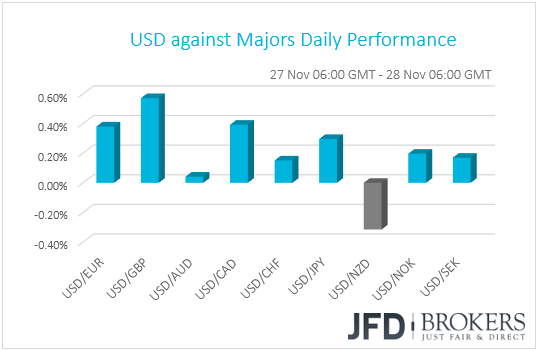

The dollar traded higher against most of the other G10 currencies on Tuesday. It gained the most against GBP, CAD and EUR, while it lost ground only versus NZD. It traded virtually unchanged against AUD. The drivers behind the greenback’s strength may have been hawkish remarks by Fed Vice Chairman Richard Clarida, as well as a risk-off mood throughout most of the day.

Kicking off with Clarida, the Fed’s Vice Chair noted that US economic fundamentals are robust, and that US GDP growth is strong. Most importantly, he said that he would back more hikes than expected if inflation surprises to the upside.

The dollar came under selling interest around 10 days ago, following comments from several FOMC policymakers, including Clarida himself, which leaned to the dovish side. Back then, Clarida said that interest rates are very close to neutral, adding that there is some evidence of slowing global economic growth and that the Committee is at a point where it needs to be data dependent. His remarks over global economic growth were echoed by Dallas Fed President Robert Kaplan as well as Philadelphia Fed President Patrick Harker, who even appeared concerned on whether a December hike would be appropriate.

Although the market remained optimistic with regards to a December rate increase after those remarks, it priced out the number of the hikes expected through 2019, to 1.4 from 2 prior to the dovish speeches. That number rebounded to 1.5 yesterday following the hawkish flavor in Clarida’s fresh comments. In our view, that number could have risen more, but investors may have remained on guard ahead of Chair Powell’s speech later today.

In early October, the Fed Chief hinted that the Fed was nowhere close to a pause when it comes to future rate increases. Back then, Powell said that he is very happy with regards to the economic expansion, adding that interest rates are still distant from their neutral level and that the Fed could raise them past that level. Since then, equity markets have tumbled to correction levels and, as we already noted, investors have turned more cautious with regards to the Fed’s future plans. It is also interesting to note that just a day ahead of Powell’s speech, US President Trump reiterated that he is not happy with the Fed’s plans to keep raising rates.

So, having all these in mind, it would be interesting to see whether Powell will maintain an upbeat stance. If he does, we expect the dollar to stay under buying interest and the number of the hikes expected by the market throughout 2019 to rise further. On the other hand, a more cautious stance by the Fed Chair may add to the idea that the Fed could decide to pause hiking soon.

USD/CAD – Technical Outlook

USD/CAD keeps on climbing higher since its reversal to the upside on the 1st of October. We can draw a short-term trendline from the low of the same day, which still has not been violated and the pair continues to trade above it in an orderly fashion. Yesterday USD/CAD had another good run in the upwards direction, but got held by the resistance at 1.3315, which kept the rate down on the 20th of November. That said, as long as the pair remains above its short-term upside line, we will continue aiming higher.

If USD/CAD continues to travel north and pierces through the 1.3315 resistance area, such a move might clear the path towards a slightly higher level, at 1.3350, which was the high of the 28th of June. A further acceleration of the rate could drive the pair to an even better resistance barrier at 1.3385, marked by the highest point of June. Certainly, let’s not exclude a possibility of seeing a bit of retracement back down from the current level. The pair could drop to test the support hurdle near the 1.3265 zone, or even the aforementioned short-term upside line.

Alternatively, if the above-mentioned upside line breaks and the pair moves below the 1.3185 obstacle, marked by this week’s low, this may spook the bulls from the battlefield, where more bears would be more than happy to jump in and steer the pair in the southern direction. This is where we could aim for support levels such as 1.3155, or even 1.3125, with the latest being the low of the 16th of November. If that area is not able to withstand the bear-pressure, a further slide may bring the 1.3085 support zone into play.

![]()

Equity Markets Rebound After Kudlow’s Comments

Now getting the ball rolling with the broader market sentiment, most European indices ended their session in negative territory, perhaps weighed by US President Trump’s comments after the US close on Monday that he remains willing to raise the tariff rate on USD 200bn Chinese goods to 25% from 10% and that he may proceed with tariffs on the remaining imports from China, unless he and his Chinese counterpart manage to find common ground.

However, risk sentiment took a 180-degree turn during the US session, with the S&P 500 and the Dow Jones Industrial Average closing in the green. Nasdaq ended the US session virtually unchanged. The catalyst behind the change in investors’ mood may have been comments by White House Economic Advisor Larry Kudlow, who said that the upcoming meeting between the US President and his Chinese counterpart at the G20 summit may be an opportunity for the two nations to “turn the page” on a trade war. However, Kudlow also said that the US administration has been disappointed so far with China in trade talks.

We believe that market volatility is likely to increase as the G20 summit draws closer. Headlines suggesting that the two leaders could eventually find common ground may boost further risk appetite. Equity indices may recover some more of their recently lost ground, while safe-haven assets are likely to stay on the back foot. The opposite could be true if news point to further escalation.

With regards to the outcome of the meeting between Trump and Jinping, our view remains the same as on Monday. The US President has repeatedly expressed his willingness to work towards securing a deal with China, but recent developments suggest that it would be very hard for an accord to be agreed as early as at this meeting. Last week, the Asia-Pacific Economic Cooperation (APEC) group failed to strike a communique for the first time in its history, due to differences between US and China over trade, while the Trump administration said that China took “further unreasonable actions in recent months” with regards to intellectual property. Thus, the two leaders could just agree to keep the door open for further talks.

DJIA – Technical Outlook

Overall, the Dow Jones Industrial Average is still below its downside resistance line drawn from the peak of the 3rd of October. That said, the index has rebounded on Monday from its long-term upwards-moving trendline taken form the low of the 6th of February and continues to move into areas that were last time tested in the beginning of November. At the same time, looking at our DJIA cash index on the 4-hour chart, the Average has broken a very short-term downside resistance line, drawn from the high of the 9th of November and shifted back into positive territory for the year. From the short-term perspective, the US index could continue its journey north, but because there are still a lot of uncertainty on the trade arena the move higher could just be a correction.

From the technical side, if the Dow Jones continues to push above the 24843 resistance, this might be a good opportunity for more bulls to step in temporarily and drive the index towards the next potential area of resistance at 25100, marked by the inside swing low of the 16th of November. A further acceleration of the price may lead the DJIA to the 25345 obstacle, or even the 25500 barrier, which held the index down on the 19th of November.

On the other hand, if the Dow Jones struggles to have a firm move above the 24843 level and reverses back down below the 24675 hurdle, marked by Monday’s and the 21st of November’s high, this would automatically place the US index below the aforementioned very short-term downside resistance line, as well as back into the negative territory for the year. This is when we will aim for another possible test of the 24415 support zone, which was yesterday’s low, or even for another test of the previously-mentioned long-term upside trendline.

![]()

As for the Rest of Today’s Events

In terms of economic indicators, we get the 2nd estimate of the US GDP for Q3. Expectations have now changed and suggest an upside revision to 3.6% qoq SAAR from 3.5% qoq SAAR, which was the initial estimate. New home sales for October are also coming out and are expected to have rebounded 3.7% mom after sliding 5.5% the previous month.

With regards to the energy market, the Energy Information Administration’s (EIA) weekly crude oil inventories are coming out. The forecast suggest that inventories rose 0.8mn barrels after rising 4.9mn the week before. Something like that would mark the 10th straight week of crude stock increases. Yesterday, the API report for the same week showed a 3.5mn barrels increase, which suggests that the risks surrounding the EIA forecast may be tilted to the upside.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.