Yesterday, the US-China talks ended with no material progress, just after tariffs on USD 16bn worth of products from each nation kicked in. The pound slid on the back of a strong dollar, but also on renewed concerns over a no-deal Brexit. As for today, focus is likely to fall on Powell’s speech at Jackson Hole.

US-China Talks End, Powell Takes Center Stage

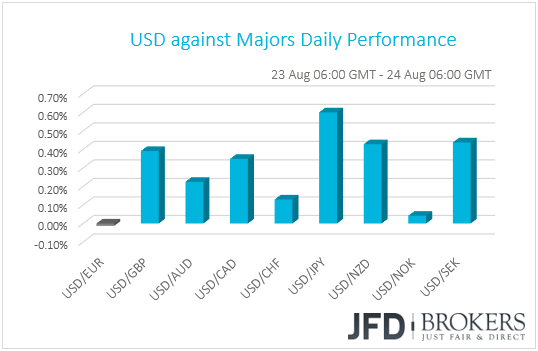

The dollar continued to recover against all but two of the other G10 currencies on Thursday. It gained the most against JPY, SEK and NZD in that order, while it traded virtually unchanged versus EUR and NOK. The Aussie, although it still ended the day lower against its US counterpart, rebounded overnight after PM Turnbull was ousted and replaced by Scot Morrison.

Yesterday, the talks between the US China ended with no breakthrough after tariffs on USD 16bn worth of products from each nation kicked in. On Tuesday, we said that this could hurt risk sentiment somewhat. Indeed, although not clearly evident in the currency market (USD strengthened but JPY lost the most ground), major European and US indices ended their sessions in the red.

However, we also noted that bearing in mind last Friday’s reports that the two nations are working on a road map that would eventually lead to a meeting between US President Trump and Chinese Leader Xi Jinping in November, such a switch may remain limited and/or short-lived. After all, there were little hopes that we may get something concrete from this round and thus there is little room for disappointment, in our view. Indeed, Asian indices rebounded overnight, with Japan’s Nikkei ending its session up around 0.80%. Even China’s Shanghai Composite index ended slightly in the green. We believe that barring any headlines suggesting a breakdown of plans for future negotiations, expectations that further talks may lead to top-level meetings could keep market sentiment relatively supported.

As for today, attention is likely to turn to the Jackson Hole Economic Symposium and Fed Chair Powell’s speech. Following the latest comments by US President Trump that he is “not thrilled” with Powell’s decision to keep raising rates and that the Fed should be more accommodating in order to help him boost the economy, market participants would be eager to hear what the Fed Chief has to say.

As for what we believe, we don’t expect him to signal any change in the Fed’s course for further gradual rate increases. We expect him to maintain an upbeat view on the US economy and keep the door wide open for two more rate hikes this year. The last thing he may want is to hurt investors’ faith over their independence. Yesterday, Dallas Fed President Robert Kaplan and Kansas City Fed President Esther George stressed the Fed’s independence, further supporting our view. Investors may also look for Powell's view on trade uncertainties, but, if he chooses to comment on the matter, we don’t expect him to say something much different than what we already know. The minutes of the latest FOMC meeting revealed that policymakers suggested that further escalation is a potentially consequential risk for economic activity and thus, we expect his remarks to be along those lines.

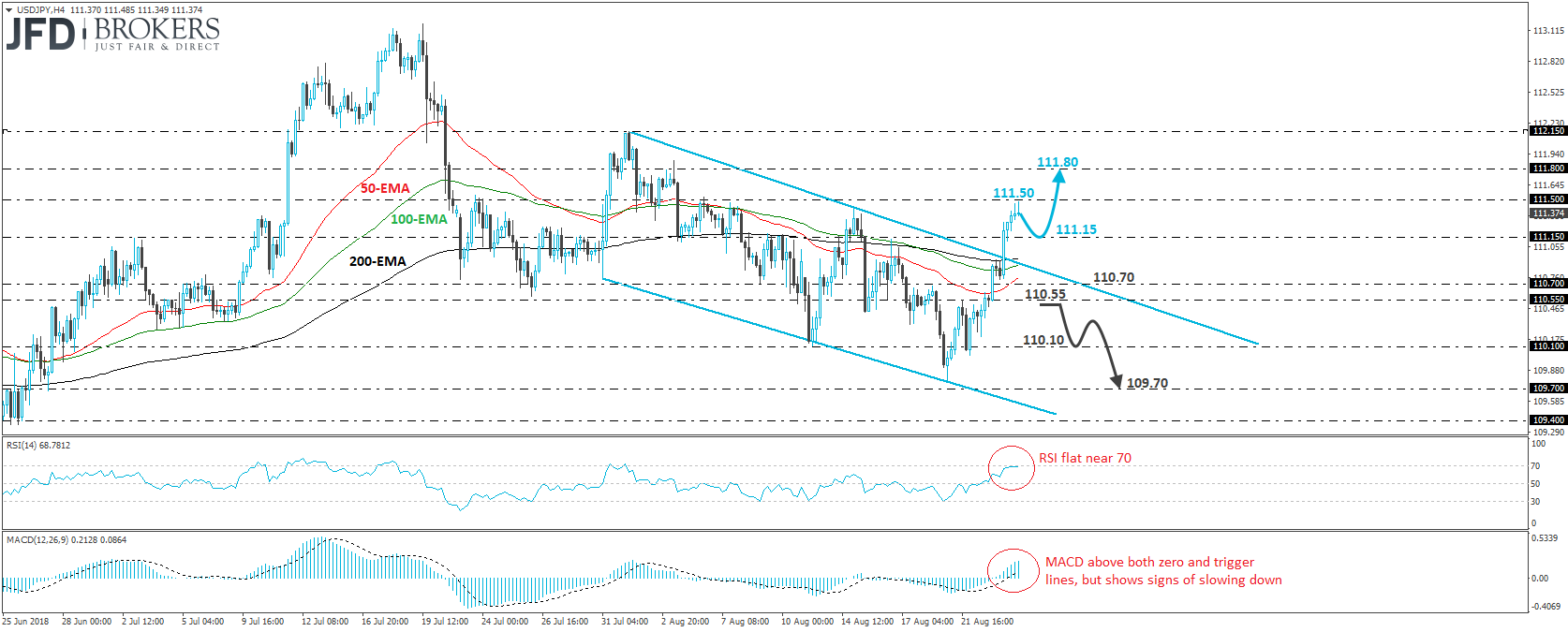

USD/JPY – Technical Outlook

USD/JPY surged yesterday, breaking above the tentative downside resistance line drawn from the peak of the 1st of August. Subsequently, the rate emerged above the 111.15 resistance (now turned into support) hurdle, to stop near our next obstacle of 111.50. In our view, the break above the aforementioned downside line has changed the short-term outlook to somewhat positive and thus, we would now expect the rate to continue drifting north.

We would expect a clear and decisive break above 111.50 to pave the way towards our next resistance of 111.80. However, given that the latest rally appears overextended, we see a decent chance for a corrective retreat to occur before the bulls decide to take charge again, perhaps for a test near the 111.15 barrier, or the prior downside resistance line.

Our short-term oscillators detect slowing upside speed, which supports our view that a corrective setback may be looming before the next positive leg. The RSI has flattened near its 70 barrier, while the MACD, although above both its zero and trigger lines, shows signs of slowing down.

On the downside, we would like to see a dip back below 110.55 before we start examining whether the bears have taken control. Such a move could confirm that the rate has returned back below the aforementioned downside resistance line and could initially aim for the 110.10 zone. Another break below 110.10 could pave the way towards 109.70.

Pound Retreats on Renewed Brexit Concerns

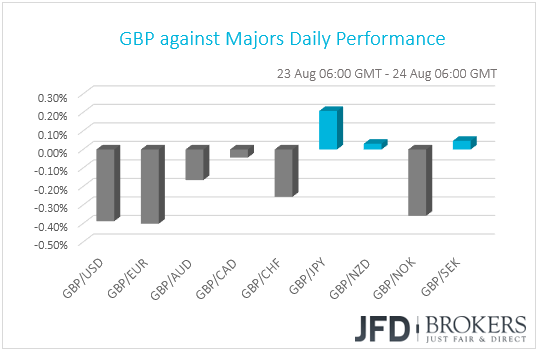

The pound traded lower or unchanged against all but one of its G10 peers on Thursday. It gained only against JPY. The pound lost the most ground against EUR, USD and NOK in that order, while it traded virtually unchanged against CAD, NZD and SEK.

Yesterday, Brexit Secretary Dominic Raab presented the first notices of the government’s plans in case of a no-deal Brexit. The plans revealed that UK credit card users could be obligated to pay a “Brexit tax”, while UK companies trading with the EU would face a massive increase in red tape and possible delays at the border.

Yesterday’s publication may have revived fears for of a no-deal outcome, and combined with a strong greenback, pushed the pound lower. In our view, with any BoE rate-hike expectations well-pushed into next year, the pound is likely to remain sensitive on political developments. Although the currency has already priced the no-deal Brexit to a decent extend, with the clock ticking towards the 29th of March, the official date of the UK’s departure from the EU, and no signs that the two sides are close to finding an accord, the pound could still come under additional selling interest.

GBP/CAD – Technical Outlook

GBP/CAD slid after hitting resistance fractionally below the 1.6840 hurdle. However, the slide was stopped by the 1.6730 zone and then, the rate rebounded somewhat. The pair continues to trade below the downtrend line taken from the peak of the 22nd of June and thus, we would consider the short-term outlook to still be negative.

We would expect the bears to take charge again soon and push the rate below 1.6730. Such a break could set the stage for downside extensions towards our next support area of 1.6635, or the 1.6590 zone, marked by the lows of the 14th and 15th of August.

However, before that, we see the case for a small corrective recovery, perhaps for another test near 1.6840, or near the downtrend line. That view derives from our short-term momentum studies. The RSI rebounded from near 50 and now stands flat near that line, while the MACD, although below its trigger line, stands positive and shows signs that it could start bottoming soon.

In order to start examining the case of a short-term trend reversal, we would like to see a clear break above the short-term downtrend line taken from the peak of the 22nd of June. Such a break is likely to initially aim for the 1.6925 resistance, the break of which could open the path towards 1.7030.

As for the Rest of Today’s Events

During the European day, we get Germany’s final GDP for Q2. As usual, the forecast is for the final print to confirm the preliminary estimate and show that Eurozone’s growth engine accelerated to +0.5% qoq from an upwardly revised +0.4% in Q1.

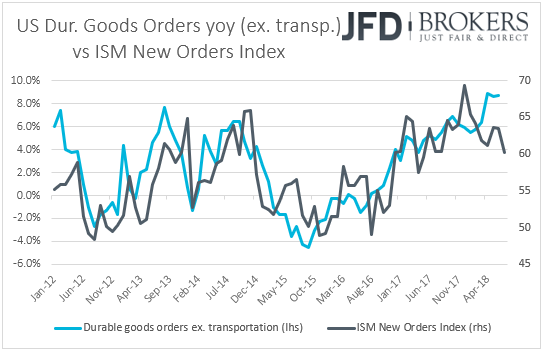

From the US, we get durable goods orders for July. Expectations are for headline orders to have risen by 0.8% mom, the same pace as in June, something that could push the yoy rate up. As for core orders, they are anticipated to accelerate on a monthly basis, to +0.3% mom from +0.2%, but this is likely to drag the yoy rate down. The case for a decline in the yearly core rate is supported by the New orders sub-index of the ISM manufacturing PMI for the month, which declined to 60.2 from 63.5 in June.

As for the speakers, besides Fed Chairman Powell, BoE’s Chief Economist Andy Haldane and BoC Governor Stephen Poloz will also speak at the event. Haldane speaks later today, while Poloz will step up to the rostrum on Saturday.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.