The British pound was yesterday’s G10 winner, rallying following headlines that the UK Labour party is willing to support an amendment that extends Article 50 in case no deal is reached by the end of next month. The Aussie slid overnight after the NAB decided to hike mortgage rates. As for today, the spotlight is likely to fall on the ECB decision and especially the Bank’s language with regards to the economic outlook. The Norges Bank decides on monetary policy as well.

GBP Up on Brexit-delay Reports, AUD Down on NAB Mortgage Rate Hike

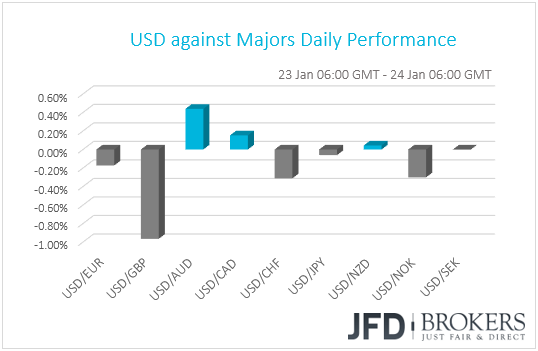

The dollar traded lower or unchanged against most of the other G10 currencies yesterday. It gained only against AUD and CAD, while it underperformed against GBP, CHF, NOK and EUR. The greenback traded virtually unchanged versus JPY, NZD and SEK.

For another day, the pound was among the winners, this time taking the front seat. The currency surged and emerged above the psychological zone of USD 1.3000, following headlines that the Labour party is “highly likely” to support a plan that delays Brexit if an accord is not found by the end of February. The proposal by lawmaker Yvette Cooper suggests a nine-month extension to the 31st of December.

We already knew that Labour’s leader Jeremy Corbyn has been calling PM May to rule out a no-deal outcome, and thus, the party’s support to Cooper’s amendment should not be a big surprise. That said, the driver behind the latest recovery in the pound has been expectations that a no-deal withdrawal can be avoided, and yesterday’s headlines encouraged investors to add to those bets.

As for our view, it hasn’t changed. We’ve been highlighting that, with the clock ticking towards the 29th of March, we see the case for May to secure a broadly-accepted deal as a hard task. On Monday, she said that she will be “more flexible” with lawmakers, but even if her flexibility leads to a plan that could pass through Parliament, she may not find the EU on the same page. Remember that EU officials have been adamant that the accord agreed with May is the only possible deal, with EU Chief Negotiator Michel Barnier reiterating that position even yesterday. Thus, given that everyone agrees a disorderly exit should be avoided, the next inline option may be extending Article 50.

As for the pound, such expectations may keep the currency supported for a while more. However, as investors continue to price out the likelihood of a no-deal outcome, with no fresh bullish catalysts from the Brexit arena, the currency may run out of upside momentum soon. After all, the UK political crisis is far from resolved.

The Australian dollar was the currency that suffered the most. It gained overnight following Australia’s better-than-expected jobs data, but was quick to reverse back down, erase the employment-related gains and trade even lower within the next couple of hours. The slide was triggered by the decision of the National Australia Bank, one of Australia’s “big four” banks, to increase mortgage rates by 12bps, citing “sustained increases” in funding costs. The move represents a tightening in financial conditions and could delay the RBA from hiking even further. According to the central bank’s latest quarterly Statement on Monetary Policy, the benchmark cash rate is expected to increase in 2020.

GBP/AUD – Technical Outlook

With a stronger British pound and a weaker Australian dollar, this is the result which you get – GBP/AUD flying sky high. The pair is trading well above its upside support line drawn from the low of the 3rd of December 2018, but also above a steeper short-term upside line taken from the low of the 15th of January. At the time of this analysis, GBP/AUD is trading near the 1.8400 hurdle, which provided decent resistance from the 18th until the 23rd of October. For now, we will continue aiming higher, but with the potential of seeing a bit of a correction back down, before another leg of buying.

If GBP/AUD travels above the 1.8400 barrier, this might clear the path towards the next potential strong resistance zone, at 1.8513, marked by the peak of the 2nd of January. But this is from where the pair might correct itself back down, as our oscillators suggest that on the 4-hour timeframe GBP/AUD is already slightly overbought. The pair could push back down, but if it fails to move below the 1.8400 obstacle, that level may act as a good area for a bounce, which could lead to another leg of buying. A push further up and a break of the 1.8513 barrier could lift the rate to a test of the 1.8565 level, marked by the high of the 16th of October last year.

Alternatively, a drop below the aforementioned steep upside line and the 1.8255 hurdle could invite more bears into the game. GBP/AUD may then travel further down towards the key support area between the 1.8135 and 1.8105 levels, a break of which could show that there is even more weakness in the pair and further declines are possible. The next support level, which we will be looking at will be around 1.7945, marked near the low of the 21st of January.

![]()

ECB Decision Takes Center Stage, Norges Bank Meets as Well

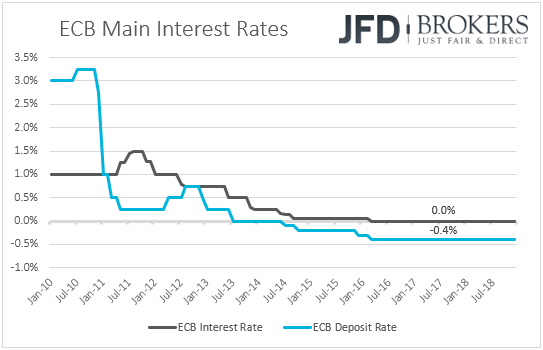

As for today, the big event is likely to be the ECB monetary policy decision. Although no change in policy is expected, focus is likely to fall on the Bank’s language with regards to the economic outlook. At the previous meeting, the Bank formally ended its asset purchasing program, while at the press conference following the decision, President Draghi noted that “The risks surrounding the euro area growth outlook can still be assessed as broadly balanced.” However, he added that the balance of risks is moving to the downside due to the persistence of uncertainties related to geopolitical factors, the threat of protectionism, vulnerabilities in emerging markets and financial market volatility.

Since then, data has kept coming in on the soft side, with Eurozone’s composite PMI for December hitting its lowest since November 2014, headline inflation slowing by more than anticipated during the month and the core CPI rate staying stubbornly at +1.0% yoy, well below the Bank’s objective of “below, but close to 2%”. This may have raised speculation that Draghi and co. may have to change their language around the economic outlook soon, noting that the risks have shifted to the downside. With the minutes of the prior meeting showing that some policymakers argued for such a change to take place then and ECB President Draghi noting last week that “there is no room for complacency”, we see a decent likelihood for this to happen at this meeting.

As for the euro’s reaction, we see the surrounding risks as asymmetrical. If indeed the Bank says that the risks of the economic outlook has shifted to the downside, the euro is likely to weaken, but not much. After all, it has been already sliding due to such expectations. The surprise would be if Draghi reiterates that the risks are still balanced. Coming on top of further softness in the bloc’s economic data and especially his own remarks of no room for complacency, something like that could catch investors off guard and the euro could rally.

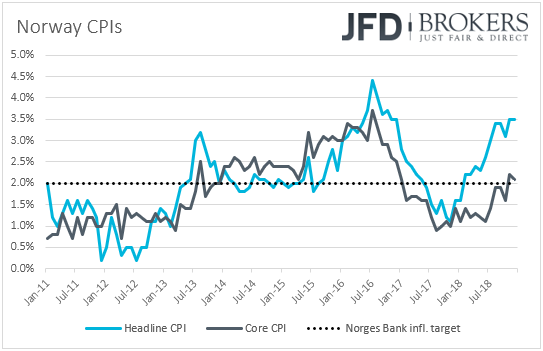

Ahead of the ECB, we have another major central bank deciding on interest rates: the Norges Bank. Expectations are for no policy action from this Bank either. Officials are expected to keep interest rates unchanged at +0.75% and thus, bearing in mind that this would be one of the “smaller” meetings that are not accompanied by updated economic projections, all the attention is likely to fall on the statement. At their previous gathering, policymakers maintained the guidance that interest rates are likely to be raised in Q1 2019, noting that this will most likely happen in March. What’s more, they said that the upturn in the economy appears to be continuing, without mentioning anywhere the slowdown in mainland GDP for Q3.

Last Thursday, Norway’s inflation data showed that the headline CPI rate held at +3.5% yoy, instead of ticking down to +3.4% yoy as was expected, while the core declined to +2.1% yoy from +2.2%. The core forecast was for a slide to +2.0% yoy. Thus, with both the headline and core inflation rates above the Bank’s objective of 2.0%, as well as above its own projections for December, we doubt that policymakers will be tempted to alter their view over when they expect interest rates to rise again. We expect them to repeat that the next hike is likely to occur in March, and thus, we see the case for a major reaction in NOK as somewhat unlikely.

EUR/USD – Technical Outlook

EUR/USD pushed higher yesterday, putting itself back into positive territory for the week. Now the big question is: Will it be able to maintain these gains, or will we see strong selling activity today, after the ECB’s press conference? From the technical side, the pair is still trading above its medium-term upside support line taken from the low of the 12th of November 2018. On Tuesday, it made a good push towards that line, which it tested and reversed back up. The pair found good resistance yesterday, near the 1.1395 hurdle. At the time of this analysis EUR/USD is retracing back down slightly. In our view, it would be a bit difficult to understand exactly, in which direction the pair could make a move later on, given the significance of the news coming out from the ECB. We might see increased erratic volatility, which may result in huge swings, hence why we will take a somewhat cautious approach and wait for a confirmation break.

EUR/USD could make a swing lower towards the aforementioned upside support line, which, if remains intact, may act as a good bouncing ground for the bulls to drive the pair back up again. A push above yesterday’s peak, at 1.1395, could lead to a test of the 1.1425 obstacle, which is the high of the 16th of January. If that obstacle doesn’t stand a chance in withholding the rate down, a break of it might clear the way towards the next potential resistance zone at around 1.1450, marked by the low of the 14th of January.

On the other hand, if suddenly selling activity increases, EUR/USD breaks the aforementioned upside support line and drops below the 1.1335 level, this may spook the bulls from the field. Without any hesitation, the bears could jump behind the steering wheel and drive the pair lower towards the 1.1310 obstacle, a break of which could push the rate further down, where the next potential area of resistance could be seen at 1.1270, marked by the low of the 14th of December 2018.

![]()

As for the Rest of Today’s Events

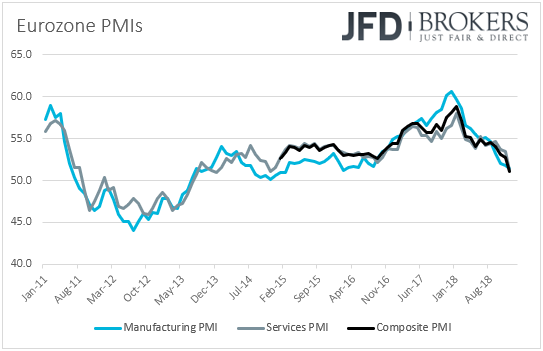

During the European session, ahead of the ECB decision, we get preliminary PMIs for January from several European nations and the Eurozone as a whole. The bloc's manufacturing index is forecast to have remained unchanged at 51.4, while the services one is expected to have risen to 51.5 from 51.2. Something like that is likely to lift the composite index to 51.4 from 51.1. That said, we don’t believe that such a rebound would ease concerns with regards to the health of the Euro area economy. Investors may need more evidence that this is the case.

We get preliminary Markit PMIs for January from the US as well. Both the manufacturing and service-sector indices are forecast to have declined to 53.5 and 54.2 from 53.8 and 54.4 respectively. That said, we have to repeat once again that the market tends to pay more attention to the ISM indices, which are scheduled to be published on the 1st and 5th of February. Initial jobless claims for the week ended on the 18th of January are also coming out.

With regards to the energy market, we have the EIA (Energy Information Administration) weekly report on crude inventories and expectations are for a 0.04mn barrels decrease after the 2.68mn slide the week before. That said, bearing in mind that the API report revealed a 6.55mn inventory build, we see the risks surrounding the EIA report as tilted to the upside. An upside surprise could bring oil prices under some more pressure.

As for tonight, during the Asian morning Friday, Japan’s Tokyo CPIs for January are scheduled to be released. No forecast is available for the headline rate at the moment, while the core rate is anticipated to have held steady at +0.9% yoy. With Japan’s inflation metrics showing no signs of a build up in price pressures, we repeat for the umpteenth time that we don’t expect any meaningful normalizing step from the BoJ anytime soon.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Group, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Group analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD Group prohibits the duplication or publication without explicit approval.

68% of the retail investor accounts lose money when trading CFDs with this provider. You should consider whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.