The pound was yesterday’s main gainer as it skyrocketed following comments from EU chief negotiator Michel Barnier that the European Union was ready to offer the UK a close relationship after Brexit. Elsewhere, market sentiment remained supported amid the ongoing NAFTA talks. As for today, focus is likely to fall on the US core PCE index for July and Canada’s GDP for Q2.

Barnier’s Comments Wake GBP-Bulls Up

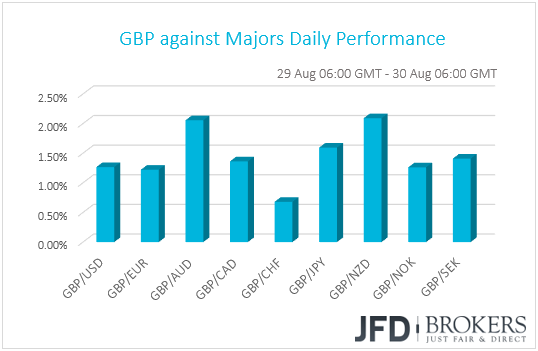

The pound made a 180-degree turn yesterday and surged against all the other G10 currencies, gaining the most against NZD, AUD and JPY.

The British currency had been on a slide recently due to increasing concerns that the UK could end up leaving the EU without a deal. However, pound bulls woke up yesterday after EU chief Brexit negotiator Michel Barnier said, “We are prepared to offer Britain a partnership such as there never has been with any other third country.” Nonetheless, he repeated that “there is no single market a la carte”, which means that the EU would still not allow the UK to cherry-pick on the single market.

Although the comments were a major relief for investors and may keep the pound supported for a while more, they are far from suggesting that a deal is imminent. With seven months to go until the official divorce date, the two sides have still a lot to work on, like the major issues of trade and the Irish border. What’s more, as we noted yesterday, officials on both sides admit that finding common ground by October is unlikely, and they will now aim to finalize the terms of the divorce by November.

Moving forward, we expect the pound to remain extremely sensitive on Brexit developments. Any headlines suggesting that the two sides are moving in the direction of securing a deal are likely to prove positive for the pound. On the other hand, developments pointing to more delays could revive fears over a disorderly exit and could bring sterling under renewed selling interest.

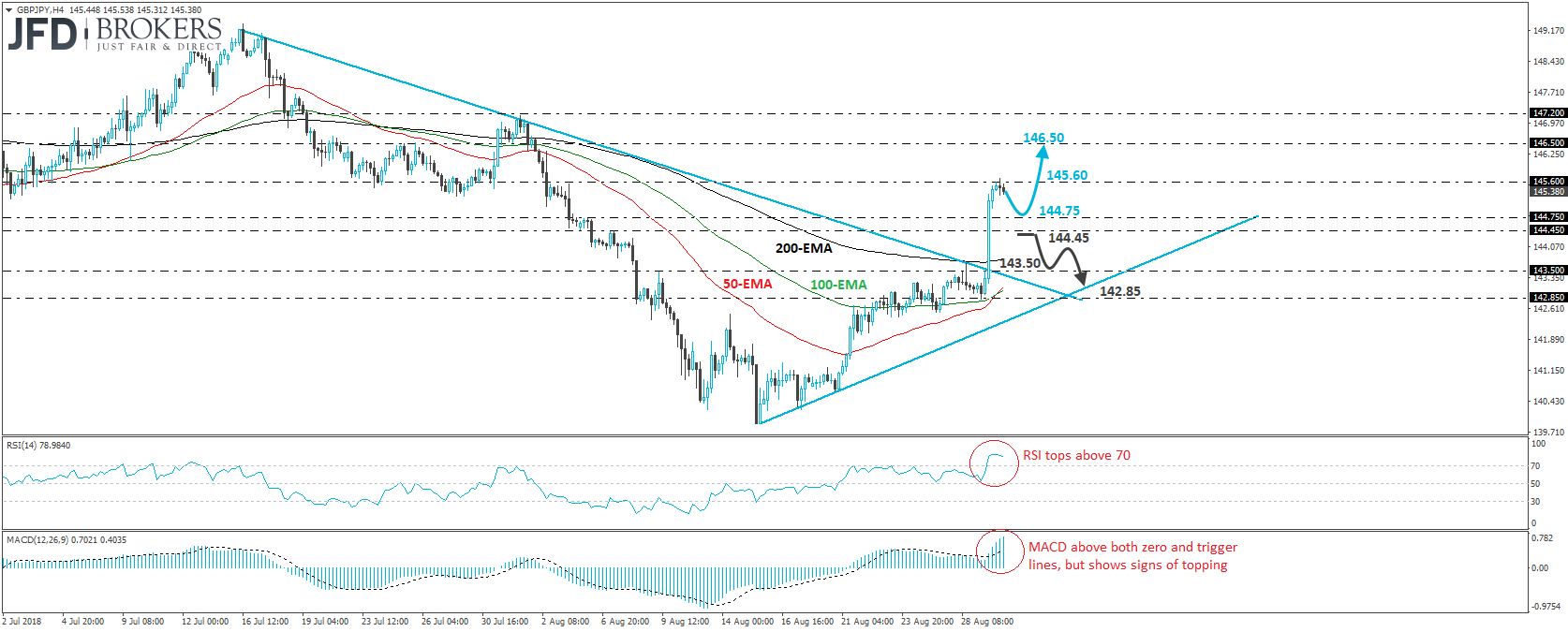

GBP/JPY – Technical Outlook

GBP/JPY surged yesterday following Barnier’s remarks, breaking above the downside resistance line drawn from the peak of the 16th of July. The rally was eventually stopped near the 145.60 resistance zone. In our view, the move above the aforementioned downside line has turned the short-term outlook to positive and suggests that the pair could continue drifting higher for a while more.

A break above 145.60 could open the way for our next resistance of 146.50, defined by the inside swing low of the 1st of August. However, given that yesterday’s rally appears overextended, we would expect a corrective setback before the next positive leg, perhaps for the rate to challenge the 144.75 hurdle as a support this time.

The case for a pullback is supported by our short-term oscillators as well. The RSI topped within its above-70 zone, while the MACD, even though above both its zero and trigger lines, shows signs that it could start topping as well.

Now, if the 144.75 hurdle does not act as a support and the rate falls below 144.45, then we may experience a deeper correction. A dip below 144.45 could open the way for the 143.50 zone, where another break could aim for the upside support line drawn from the low of the 15th of August, or the 142.85 barrier.

NAFTA Talks Continue, US Core PCE and Canada’s GDP on the Agenda

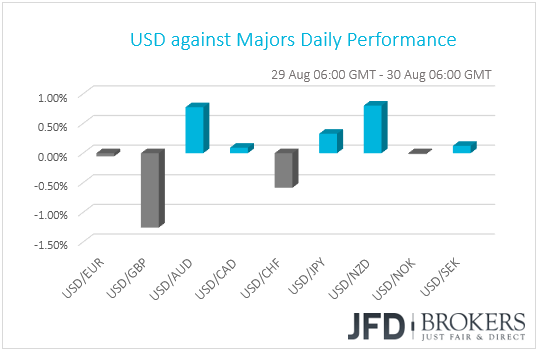

The dollar traded mixed against the other G10 currencies on Wednesday. It gained against NZD, AUD and JPY in that order, while it depreciated versus GBP and CHF. The greenback traded virtually unchanged against EUR, CAD, NOK, and SEK.

It appears that the dollar’s slide has paused for now, perhaps due to some short-covering on the latest USD-short positions. That said, although the US currency did not experience further safe-haven outflows yesterday, the broader market sentiment remained relatively supported, and this is evident by the performance in equity markets. In Europe, Euro Stoxx 50 and the German DAX ended their session in the green, although UK’s FTSE 100 closed negative, while all the US indices rose, with the S&P 500 and Nasdaq hitting record highs for the fourth consecutive day.

Back to the currencies, the Canadian dollar was on the defensive yesterday, but rebounded strongly on encouraging headlines around the NAFTA talks, to end the day virtually unchanged against its neighboring US dollar. Specifically, Canadian Foreign Minister Chrystia Freeland said that that the talks are very intense, but there is “a lot of good will” from both the US and Canada. Canada’s PM Justin Trudeau and US President Trump were also optimistic that the negotiations will bear fruit, and that Friday’s deadline will be met.

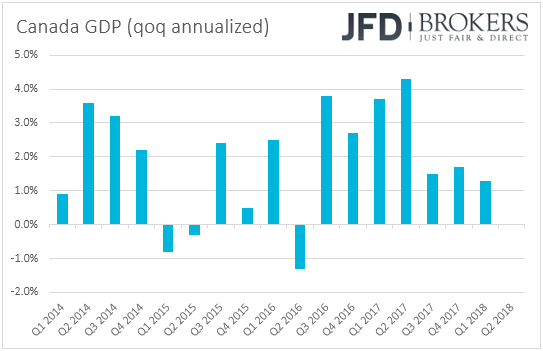

Today, besides developments around NAFTA, CAD traders are likely to also pay attention to the economic calendar, and specifically, Canada's GDP data for both June and Q2. With regards to the monthly rate for June, expectations are for a slowdown to +0.1% mom from +0.5% in May, but the qoq annualized rate for Q2 is forecast to have risen to +3.0% from +1.3% in Q1. Canada’s latest economic data have been more than encouraging, and a rise in the nation’s qoq annualized growth rate could further increase the likelihood for another BoC rate increase by the end of the year. While most participants believe that October is the most likely candidate for a hike, a better than expected GDP print could tempt some investors to place bets that the hike could be delivered even at the September gathering.

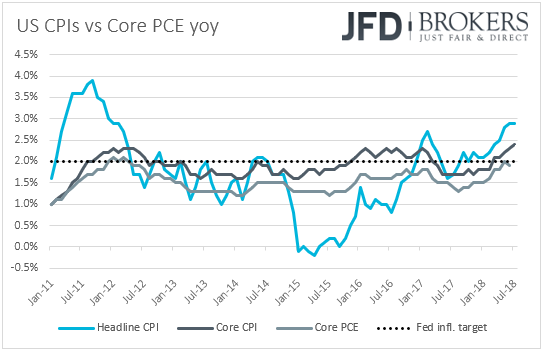

As for the US dollar, its traders are likely to focus on the PCE data for July. Expectations are for the core PCE yearly rate, the Fed’s preferred inflation measure, to have ticked back up to the Fed’s objective of 2.0%. This is supported by the core CPI rate for the month, which rose as well (to +2.4% yoy from +2.3%). A 2.0% core PCE rate could keep the Fed on track for raising rates two more times this year and could prompt policymakers to change the inflation language in the statement accompanying the upcoming policy gathering. They could note that inflation has reached their objective, instead of saying that inflation remains near the target.

USD/CAD – Technical Outlook

USD/CAD rebounded yesterday during the European session, but hit resistance near 1.2960 and then, it tumbled to stop near the 1.2900 level. Subsequently, the pair rebounded somewhat again. Bearing in mind that USD/CAD continues to trade below the prior medium-term upside support line drawn from the low of the 31st of January, as well as within the downside channel that’s been containing the price action since the 27th of June, the outlook remains negative, in our view.

We would expect the bears to take charge again soon and perhaps make another attempt to drive the battle below 1.2900. Such a break could pave the way for our next support barrier of 1.2855, defined by the low of the 6th of June. The catalyst for another leg down could be an acceleration in Canada’s GDP today, combined with more optimistic comments with regards to the negotiations over NAFTA.

That said, before the bears decide to take charge again, we see the case for the current rebound to continue for a while more, perhaps for another test near the 1.2960 resistance. That view is supported by our short-term momentum studies. The RSI rebounded from near its 30 line and is now pointing up, while the MACD, although negative, has bottomed and crossed above its trigger line.

On the upside, we would like to see a move back above the aforementioned medium-term upside support line before we abandon the bearish case , at least in the short run. Such a break may initially aim for the 1.3065 resistance, the break of which could open the path for the upper bound of the near-term channel, or the 1.3100 hurdle.

As for the Rest of Today’s Events

During the European morning, Germany’s preliminary inflation data for August are coming out. Expectations are for the German CPI rate to have remained unchanged at +2.0% yoy, which could raise speculation that Eurozone’s headline print, due out on Friday, may have held steady as well. Germany’s unemployment rate for August is also due out, and it is expected to have stayed at 5.2%.

In the US, alongside the PCE data, we get personal income and spending data for July. Personal income is expected to have slowed somewhat, to +0.3% mom from +0.4%, while spending is expected to have risen +0.4% mom, the same pace as in June. That said, the accelerations in the monthly earnings and retail sales prints for the month suggest that the risks surrounding both the income and spending forecasts may be tilted to the upside. Initial jobless claims for the week ended on the 24th of August are also coming out.

Tonight, during the Asian morning Friday, we get the usual end-of-month data dump from Japan. The nation’s unemployment rate for July is expected to have stayed unchanged at 2.4%, while the preliminary industrial production data for the month are anticipated to show that IP rebounded +0.2% mom after falling 1.8% in June. The Tokyo CPIs for August are also due to be released. Both the headline and core rates are expected to have ticked down to +0.8% yoy and +0.7% yoy, from +0.9% and +0.8% respectively.

From China, we have the official manufacturing and non-manufacturing PMIs for August. Expectations are for both PMIs to have declined to 51.0 and 53.8, from 51.2 and 54.0 respectively.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. JFD Brokers, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD Brokers analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyzes and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyzes and must therefore be viewed by the reader as marketing information. JFD Brokers prohibits the duplication or publication without explicit approval.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% of retail investor accounts lose money when trading CFDs with the Company. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Please read the full Risk Disclosure.