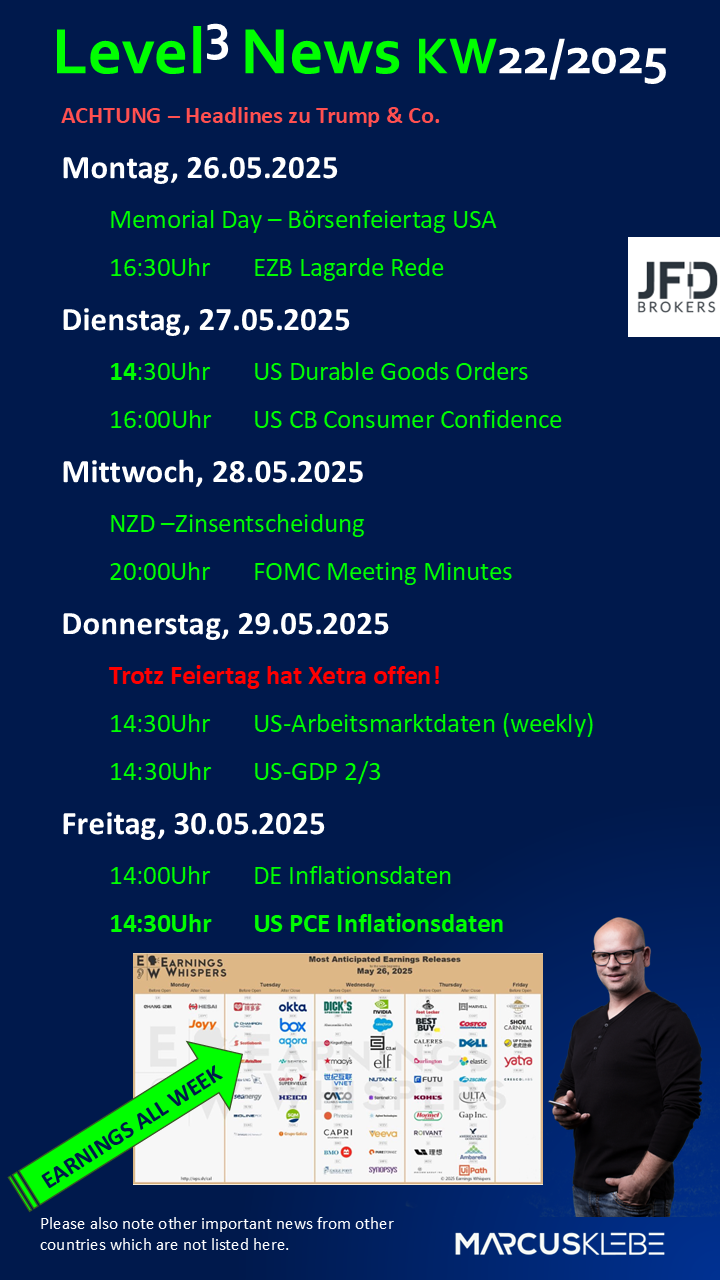

Summary (Week of May 27–31, 2025):

Next week, key macro events will include the FOMC Minutes, US PCE inflation data, and central bank meetings from RBNZ, BoK, and SARB. Also in focus: the OPEC JMMC meeting, Australian and Tokyo CPI, and Canadian GDP. In the earnings spotlight is Nvidia (NVDA), reporting on Wednesday.

Key Dates:

-

Monday: US and UK markets closed (Memorial Day & Bank Holiday)

-

Wednesday: RBNZ decision, FOMC Minutes, Australian CPI, OPEC JMMC, Nvidia earnings

-

Thursday: BoK & SARB meetings, US GDP (2nd estimate), PCE (Q1), Jobless Claims

-

Friday: US PCE (April), Canadian GDP (Q1), Tokyo CPI (May), Chicago PMI

Highlights:

-

Nvidia (Wed):

Nvidia is set to report earnings amid high expectations for AI growth. The company faces headwinds from US export restrictions to China, with CEO Huang warning of a “tremendous loss” due to chip bans. Market expectations:-

Q1 revenue: USD 43.09bln

-

EPS: USD 0.92

-

Gross margin: 71%

-

Forward guidance for Q2: USD 46.59bln revenue, USD 1.01 EPS

-

-

RBNZ (Wed):

A 25bps rate cut to 3.25% is widely expected (91% priced in). The bank continues its easing cycle due to weakening global trade, tariff-related uncertainty, and a mixed domestic economic outlook. -

FOMC Minutes (Wed):

The Fed remained on hold in May but flagged rising uncertainty around inflation and employment. The minutes will shed light on internal discussions but will not reflect recent easing of US-China trade tensions. -

Australian CPI (Wed):

April’s CPI is expected to moderate to 2.3% Y/Y (or even 1.9% per Westpac), supporting the RBA’s recent dovish shift. However, sticky prices in essentials could complicate further easing. -

BoK (Thu):

After a weak Q1 GDP print and growing political uncertainty, markets are watching for a potential start of a rate-cutting cycle. The current rate stands at 2.75%, and there are signals of a possible cut below 2.25% by year-end. -

OPEC JMMC (Wed):

OPEC+ may propose a third consecutive output hike (potentially 411k BPD) to enforce discipline on overproducing members. Final decisions will be made at the full meeting on June 1st.

Disclaimer:

The content we produce does not constitute investment advice or investment recommendation (should not be considered as such) and does not in any way constitute an invitation to acquire any financial instrument or product. The Group of Companies of JFD, its affiliates, agents, directors, officers or employees are not liable for any damages that may be caused by individual comments or statements by JFD analysts and assumes no liability with respect to the completeness and correctness of the content presented. The investor is solely responsible for the risk of his investment decisions. Accordingly, you should seek, if you consider appropriate, relevant independent professional advice on the investment considered. The analyses and comments presented do not include any consideration of your personal investment objectives, financial circumstances or needs. The content has not been prepared in accordance with the legal requirements for financial analyses and must therefore be viewed by the reader as marketing information. JFD prohibits the duplication or publication without explicit approval.

There are risks involved with trading of cash equities. Past performance is not indicative of future results. You should consider whether you can tolerate such losses before trading. Please read the full Risk Disclosure (https://www.jfdbrokers.com/en/legal/risk-disclosure).

Copyright 2024 JFD Group Ltd.